{kind=link}

Sterling rises broadly today after better than expected GDP data, even though upside momentum is weak so far. Dollar is paring some of the post-CPI gains as over sentiment, while weak, seems to be stabilizing. As for the week, Yen is the worst performing one, followed by Euro and Dollar. Aussie is the strongest one, followed by Kiwi and the Pound. There are still rooms to swap some places, depending on how US stock and bond markets end.

In Europe, at the time of writing, FTSE is down -0.67. DAX is down -0.27%. CAC is down -1.10%. Germany 10-year yield is down -0.025 at 0.260. Earlier in Asia, Hong Kong HSI dropped -0.07%. China Shanghai SSE dropped -0.66%. Singapore Strait Times rose 0.03%. Japan was on holiday.

NIESR forecasts 1.0% growth in UK GDP in Q1

NIESR forecast growth of 1.0% in UK GDP in Q1. It said that economic impact of Omicron was “far smaller than” previous two waves. The -0.2% fall in December GDP was also better than consensus forecasts, suggesting the “possibility of a positive reading in January.

“The economic impact of Omicron was far smaller than that of either of the two previous major waves of Covid-19: a mere 0.2 per cent fall in December was even stronger than consensus forecasts, but in line with NIESR’s January GDP tracker, suggesting the possibility of a positive reading in January. Unsurprisingly, retail and hospitality contributed the most to December’s fall, with the healthcare sector providing the largest positive contribution.” – Rory Macqueen Principal Economist, NIESR

UK GDP contracted -0.2% mom in Dec, up 1.0% qoq in Q4

UK GDP contracted -0.2% mom in December, better than expectation of -0.5% mom. Services output dropped -0.5% mom. Production rose 0.3% mom while construction rose 2.0% mom. Services and construction were both above pre-coronavirus levels, by 0.5% and 0.3% respectively, but production remained -2.6% below.

Q4 GDP grew 1.0% qoq, slightly below expectation of 1.0% qoq. The level of GDP in Q4 remained below -0.4% below its pre-coronavirus level in Q4 2019. Nevertheless, monthly GDP was already at its pre-coronavirus level in February 2020.

Also published, manufacturing production rose 0.2% mom, 1.3% yoy in December versus expectation of 0.2% mom, 1.7% yoy. Industrial production rose 0.3% mom, 0.4% yoy, versus expectation of 0.1% mom, 0.6% yoy. Goods trade surplus came in at GBP -12.4B, versus expectation of GBP -13.0B.

DIHK downgrades Germany growth forecasts to 3.0% in 2022

Germany’s Chambers of Industry and Commerce (DIHK) lowed 2022 growth forecasts from 3.6% to 3.0%. That is, the economy will probably not reach the pre-crisis level until middle of the year.

“The economy is holding its breath. There is still a cautiously optimistic mood in the companies. However, many do not know how things will continue due to great uncertainty,” said DIHK Managing Director Martin Wansleben.

“In addition to the Corona crisis and delivery bottlenecks, the biggest stress factors are above all the sharp rise in energy and raw material prices and the shortage of skilled workers. In addition, there are further expected cost increases due to the transformation in climate protection. It is still an open question, especially for companies that are in international competition how such a compensation should work. Many fear a deterioration of their position on the world markets.”

RBA Lowe: We have scope to wait and see

RBA Governor Philip Lowe told a parliamentary committee that it is “too early” to conclude that inflation is “sustainably in the target range”. He added, “in underlying terms, inflation has just reached the midpoint of the target band for the first time in over seven years”.

The board is “prepared to be patient” and “we have scope to wait and see how the data develop and how some of the uncertainties are resolved. Countries with higher inflation rates have less scope here.”

RBNZ survey: Another rate hike expected in Q1, 4-5 hikes in a year

In the latest Survey of Expectations of RBNZ, OCR expectations continued to rise in the short, medium and long term. OCR is expected to rise from current 0.75% to 1.05% by the end of Q1. Mean estimate for OCR for one year ahead was 2.11%, indicating four to five 25bps hikes. Mean two-year ahead OCR expectations were at 2.47%

One-year inflation expectations rose from 3.70% to 4.4%, highest since November 1900. Two-year ahead inflation expectations rose from 2.96% to 3.27%, highest since 1991. Five-year inflation expectations also rose slightly from 2.17% to 2.30%, highest since 20-17.

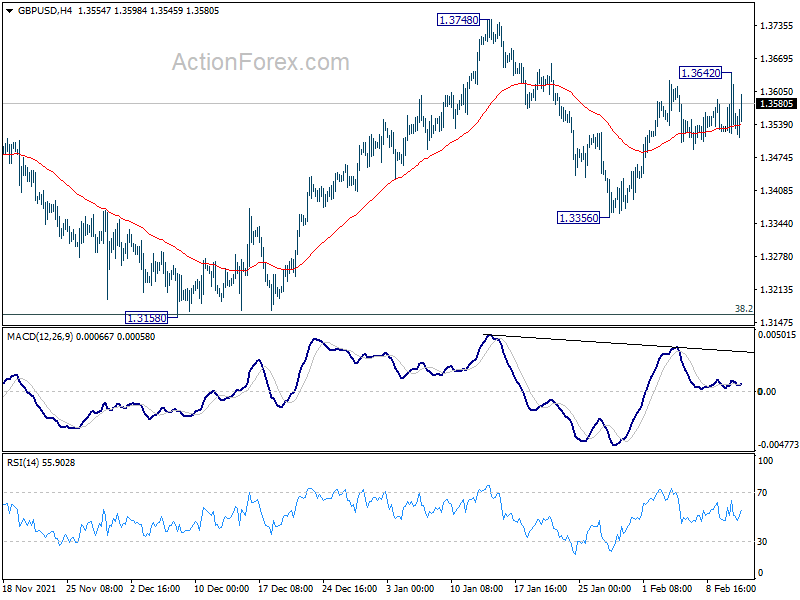

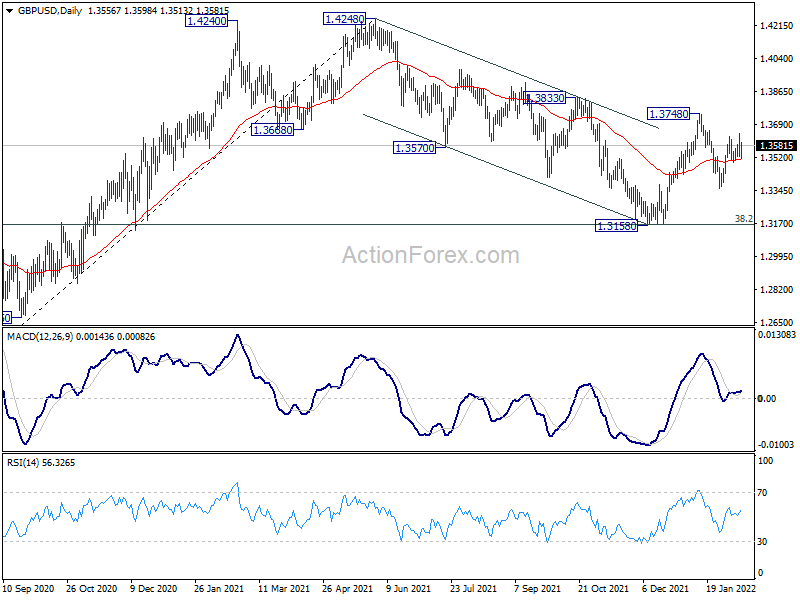

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3508; (P) 1.3576; (R1) 1.3628; More…

GBP/USD is still bounded in range and intraday bias remains neutral. On the upside, break of 1.3642 will resume the rebound to 1.3748 resistance. Firm break there will revive the bullish case that correction from 1.4248 has completed with three waves down to 1.3158. Further rally should then be seen to retest 1.4248 high. On the downside, however, break of 1.3356 will bring retest of 1.3158 low.

In the bigger picture, as long as 38.2% retracement of 1.1409 to 1.4248 at 1.3164 holds, up trend from 1.1409 (2020 low) is still in progress. On resumption, next target will be 38.2% retracement of 2.1161 to 1.1409 at 1.5134. Nevertheless sustained break of 1.3164 will argue that whole rise from 1.1409 has completed and bring deeper fall to 61.8% retracement at 1.2493

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Jan | 52.1 | 53.7 | 53.8 | |

| 02:00 | NZD | RBNZ Inflation Expectations Q1 | 3.27% | 2.96% | ||

| 07:00 | EUR | Germany CPI M/M Jan F | 0.40% | 0.40% | 0.40% | |

| 07:00 | EUR | Germany CPI Y/Y Jan F | 4.90% | 4.90% | 4.90% | |

| 07:00 | GBP | GDP M/M Dec | -0.20% | -0.50% | 0.90% | |

| 07:00 | GBP | GDP Q/Q Q4 P | 1.00% | 1.10% | 1.10% | |

| 07:00 | GBP | Index of Services 3M/3M Dec | 1.20% | 1.20% | 1.30% | |

| 07:00 | GBP | Manufacturing Production M/M Dec | 0.20% | 0.20% | 1.10% | 0.70% |

| 07:00 | GBP | Manufacturing Production Y/Y Dec | 1.30% | 1.70% | 0.40% | -0.10% |

| 07:00 | GBP | Industrial Production M/M Dec | 0.30% | 0.10% | 1.00% | 0.70% |

| 07:00 | GBP | Industrial Production Y/Y Dec | 0.40% | 0.60% | 0.10% | -0.20% |

| 07:00 | GBP | Goods Trade Balance (GBP) Dec | -12.4B | -13.0B | -11.3B | -12.701B |

| 07:30 | CHF | CPI M/M Jan | 0.20% | 0.10% | -0.10% | |

| 07:30 | CHF | CPI Y/Y Jan | 1.60% | 1.60% | 1.50% | |

| 15:00 | USD | Michigan Consumer Sentiment Index Feb P | 67.6 | 67.2 |