{kind=link}

Summary

- Eurozone economic growth softened around the turn of the year, and although consumer fundamentals should support continued expansion, GDP growth should be slower in 2022 than in 2021.

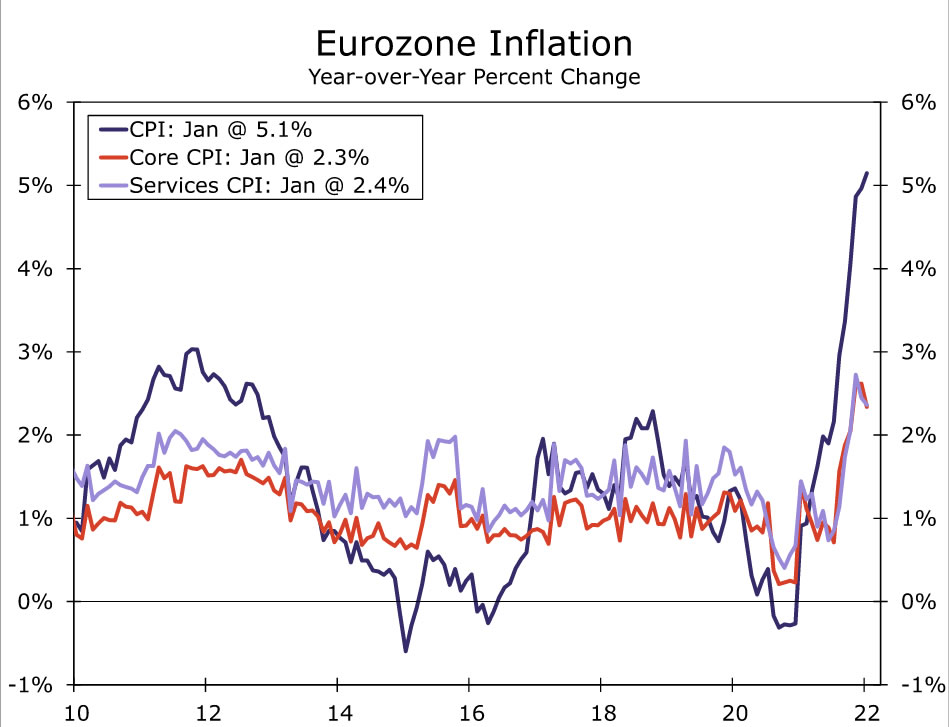

- In contrast, CPI inflation remains elevated, with January’s 5.1% year-over-year increase the largest on record. While much of the increase has been driven by energy, price pressures are becoming more broad-based, and neither headline nor core inflation have likely peaked.

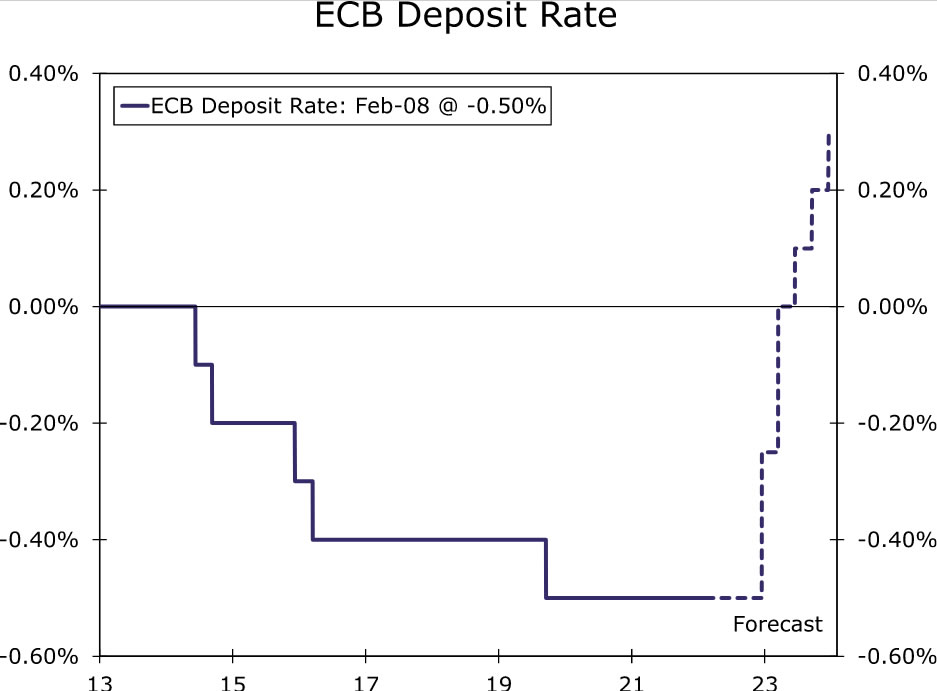

- These persistent price pressures have attracted the attention of European Central Bank (ECB) policymakers, who delivered a hawkish monetary policy announcement in early February. ECB President Lagarde said inflation risks were tilted to the upside, and did not take the opportunity to repeat that a 2022 rate hike is very unlikely.

- The ECB appears to be laying the groundwork for an eventual rate increase, which we think the central bank will build further at its March meeting by announcing a faster tapering of bond purchases. In March, we expect the ECB to signal €40B per month of bond purchases during Q2-2022, €20B per month of purchases during Q3-2022, and to say it intends to end bond purchases in September.

- Beyond March, we expect the ECB to start raising its Deposit Rate shortly after it completes its net bond purchases. Specifically, we see an initial 25 bps Deposit Rate hike in December 2022 and another 25 bps hike in March 2023. Beyond that, we see ongoing, but slower hikes, with 10 bps increases expected in June 2023, September 2023 and December 2023

Eurozone Economy Subdued Around Turn Of The Year…

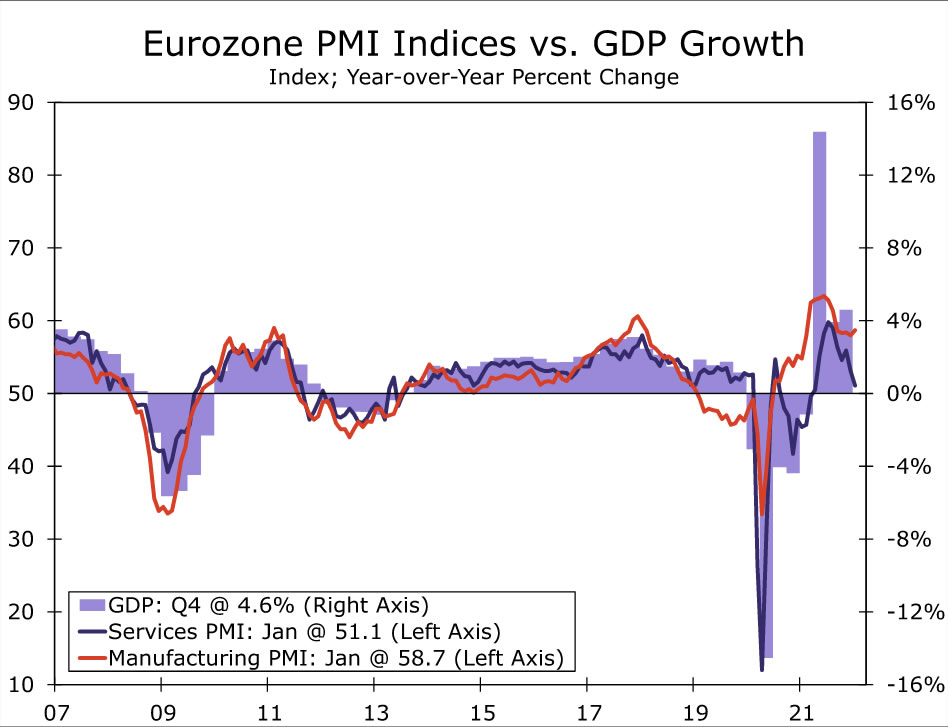

The Eurozone economy slowed noticeably in late 2021 as a resurgence of COVID cases saw some European governments reintroduce restrictions (albeit not as stringent as those earlier in the pandemic), as well as induce voluntary caution on the part of consumers. New COVID cases across the Eurozone peaked at just over 1,000,000 per day in late January, and have only receded slightly since. As one might expect, the service sector has borne the brunt of the COVID-related restrictions and caution. The Eurozone services PMI has dropped markedly for the past two months, falling to 51.1 in January. The manufacturing PMI has held up better and indeed rose to 58.7 in January, though is still down from the highs seen last summer. However, with the service sector being a much more substantial portion of the economy, overall GDP growth has also slowed significantly. Eurozone Q4 GDP rose just 0.3% quarter-over-quarter, a bit less than expected, down from growth of 2.3% in Q3 and 2.2% in Q2. With respect to Q4 GDP growth for the region’s largest economies, German GDP shrank 0.7% quarter-over-quarter, while French GDP rose 0.7% and Italian GDP rose 0.6%.

The COVID-induced slowdown will likely prove temporary, and Eurozone consumer finances remain in decent shape. In nominal terms, Eurozone household disposable income rose four out of five quarters through Q3-2021, now up 3.4% year-over-year. Meanwhile, although the household saving rate declined in Q3 to 15.0% of disposable income, it remains above pre-pandemic levels. Overall, these fundamentals suggest that a consumer-led recovery—and an overall economic recovery—can continue. That said, we acknowledge higher inflation is chipping away at consumers’ purchasing power and, accounting for the recent pickup of inflation, Eurozone real household disposable income was up only 0.8% year-over-year in Q3-2021. Therefore, while we see continued Eurozone economic growth in 2022, we think it will be slower than 2021, and forecast Eurozone GDP growth of 3.7% for this year.

…But Inflation Heating Up, Central Bank Becoming Hawkish

On the price front, the latest figures showed an unexpected quickening of inflation in January. The Eurozone January headline CPI firmed to 5.1% year-over-year, well above the consensus forecast for a 4.4% increase, and the fastest pace of increase on record. Much of the increase was driven by energy prices, which rose 28.6%, while the increase in the January core CPI (of 2.4%) and services CPI (of 2.3%) were much more moderate. Still, even the more moderate increases in these underlying inflation measures appear to have been artificially depressed by base effects stemming from a large January 2021 increase. Adjusted for seasonality, both the core and services CPI appears to be advancing faster than a 4% annualized pace over the past six months. As a result, it is likely that neither the overall nor core rate of Eurozone inflation has yet peaked, and it’s possible core inflation could peak close to or around 3% during the current cycle.

It was certainly these persistent price pressures that attracted the focus of European Central Bank (ECB) policymakers at their early February monetary policy announcement. The ECB did not adjust its monetary policy stance at that meeting, keeping its Deposit Rate at -0.50% and maintaining its existing plans to gradually wind down its asset purchases. However, compared to prior announcements, ECB President Lagarde’s post-meeting press conference was distinctly more hawkish in tone. Lagarde said that while energy prices were still the main reason for elevated inflation and price increases having become more widespread, risks to the inflation outlook were tilted to the upside. She said that policymakers expressed unanimous concern about that inflation outlook, and that updated economic forecasts due in March would provide an opportunity to thoroughly discuss the outlook. Lagarde said one can’t prejudge the March forecasts and ECB decision, but also that the central bank would decide about the future pace of bond buying at that meeting. Importantly, ECB President Lagarde did not take the opportunity repeat the comment from the December press conference that a rate hike in 2022 is “very unlikely”.

Along with recent more hawkish comments from other ECB policymakers, to us the ECB announcement is clearly laying the groundwork for an eventual rate increase from the central bank. We expect the central bank’s signaling come into clearer focus at the March 10 monetary policy announcement, at which time we expect the ECB to:

- Say it will conduct asset purchases at a monthly pace of €40B per month during Q2-2022, slowing to €20B per month during Q3-2022.

- Signal that it intends to end its asset purchases in September 2022, and repeat that it expects net asset purchases to end shortly before it starts raising the key ECB interest rates. In other words, we expect the ECB would repeat that interest rates will start increasing shortly after asset purchases end, though we would not expect the central bank to provide more precise guidance than that on the timing of an initial rate increase at this time.

Beyond March, consistent with the contours outlined above, we expect the European Central Bank will take the opportunity to start moving its Deposit Rate away from negative territory by late 2022. Specifically, we now forecast an initial 25 bps Deposit Rate increase to -0.25% at the December 2022 announcement, with another 25 bps hike to 0.00% to follow at the March 2023 announcement. Beyond March next year, we expect the Eurozone economic environment will be one of moderate growth and slowing core CPI inflation, but perhaps still above 2% at that time. Accordingly, we expect the ECB will continue raising interest rates beyond March 2023, though at a reduced pace. Specifically, we also forecast 10 bps Deposit rate increases at each of the June 2023, September 2023 and December 2023 meetings, which would see the Deposit rate end next year at +0.30%. Finally, although we believe the ECB will adjust its interest rate stance more rapidly than we previously forecast, it will lag behind the pace of rate hikes from the Federal Reserve, and also fall slightly short of the pace of ECB rate hikes currently priced in by market participants. Accordingly, we still view this more timely path for ECB interest rate increases as consistent with moderate weakness in the EUR/USD exchange rate over the medium-term.