{kind=link}

Summary

- The Bank of England (BoE) delivered a February monetary policy announcement that was towards the hawkish end of market expectations. The BoE raised its policy rate 25 bps to 0.50%, though several policymakers dissented in favor of a larger 50 bps increase. The central bank also said it will stop reinvesting maturing proceeds from its government and corporate bond holdings.

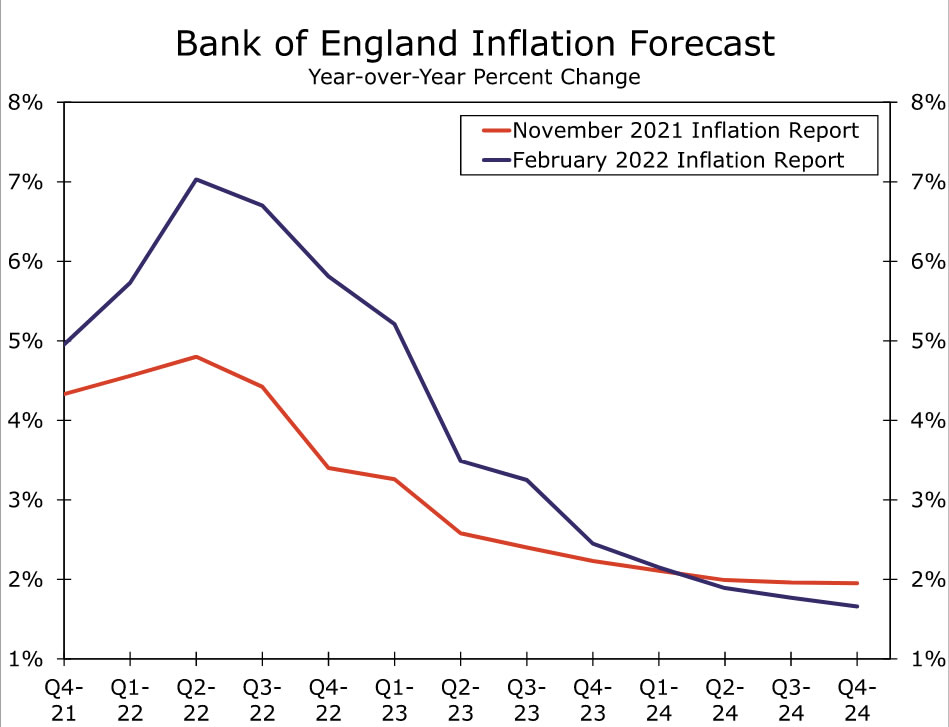

- The BoE raised its inflation forecasts, and now sees inflation peaking at 7.25% in April 2022. Despite an outlook for slower growth, in part as household incomes are squeezed by higher energy prices, the central bank said further modest tightening will be appropriate in the months ahead.

- Given the hawkish announcement, we have adjusted our outlook for Bank of England monetary policy. We expect another 25 bps policy rate increase to 0.75% in May, and also a 25 bps increase to 1.00% in August. However, as higher energy prices weigh on growth and inflation passes its peak, we do expect the pace of Bank of England tightening to slow. We do not envisage any move at the November meeting, while for 2023 we see 25 bps rate increases in February and August of next year, which would see the policy rate end 2023 at 1.50%.

Bank of England Hikes Rates and Signals Further Tightening to Come

The Bank of England (BoE) delivered a February monetary policy announcement that was at the hawkish end of spectrum in terms of market expectations. The BoE increased its policy rate by 25 bps to 0.50%, which was widely expected. However, policymakers were close to delivering an even larger 50 bps rate increase given a 5-4 vote, with the four dissenters voting in favor of a larger rate increase. In addition, having reached the 0.50% policy rate threshold and considering the economic circumstances, the BoE also said it would stop reinvesting maturing proceeds from government bonds and corporate bonds, and in addition signaled some sales of corporate bonds, allowing its balance sheet to reduce in size.

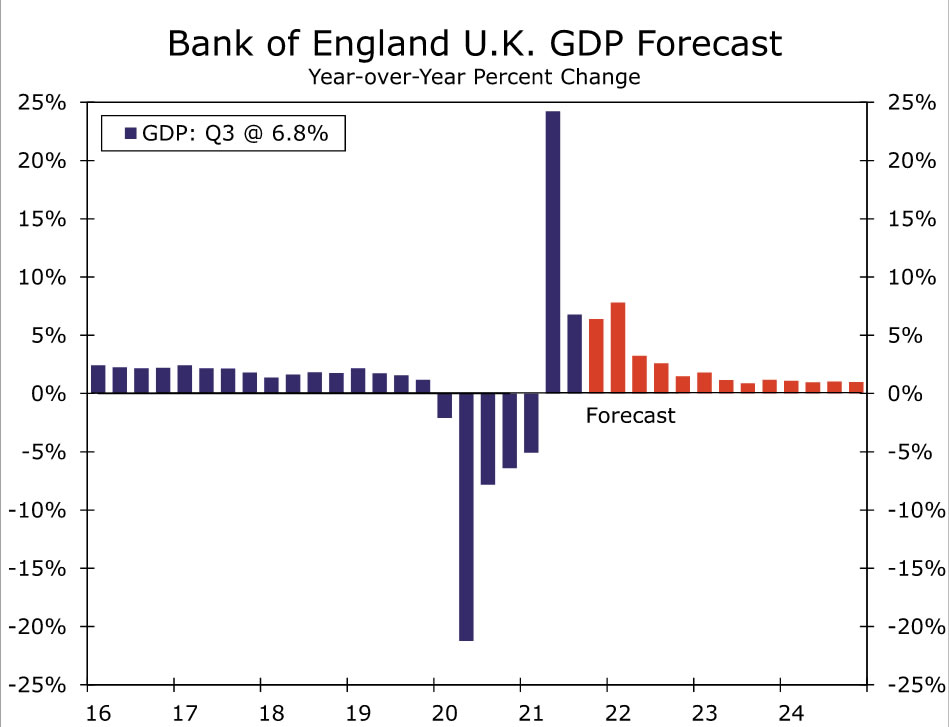

The central bank’s statement and accompanying economic projections contained some other hawkish elements as well. The BoE lifted its CPI inflation forecasts, saying it expects inflation to peak at 7.25% in April 2022. The Bank of England sees inflation slowing to 2.15% in two years and to 1.6% in three years. The revisions to the GDP growth outlook were in the other direction, with the forecast for 2022 GDP growth lowered to 3.75%.

The BoE acknowledged that energy and other price increases would squeeze real household incomes and economic growth, but also said the “MPC’s remit is clear that the inflation target applies at all times, reflecting the primacy of price stability in the UK monetary policy framework” and added that the “MPC judges that, if the economy develops broadly in line with the February Report central projections, some further modest tightening in monetary policy is likely to be appropriate in the coming months.” As a result, despite the prospect of slower growth, especially elevated inflation prompted the Bank of England to move at today’s meeting, and some further near-term rate hikes appear likely.

Indeed, comments from Governor Bailey tended to suggest that central bank monetary tightening would be front-loaded to some extent. Speaking after the formal policy announcement, Bailey said the BoE had not raised rates because the economy is “roaring away,” there is much uncertainty on the outlook, and that it is a mistake to assume interest rates are on an inevitable long march up.

Expect Earlier, And More, Bank of England Rate Hikes

We had been on the dovish end of the spectrum regarding our Bank of England outlook heading into today’s meeting—hence today’s announcement necessitates a change in our view. With the central bank signaling modest further tightening in the near-term, we expect another 25 bps policy rate increase to 0.75% in May, and also a 25 bps increase to 1.00% in August. However, as higher energy prices weigh on growth and inflation passes its peak, we do expect the pace of Bank of England tightening to slow. We do not envisage any move at the November meeting, while for 2023 we see 25 bps rate increases in February and August of next year, which would see the policy rate end 2023 at 1.50%. For the next 12 months in particular, our forecasted pace of rate hikes is more conservative than what is currently priced in by market participants, and as a result we still anticipate moderate weakness in the pound versus the U.S. dollar in the months and quarters ahead.