{kind=link}

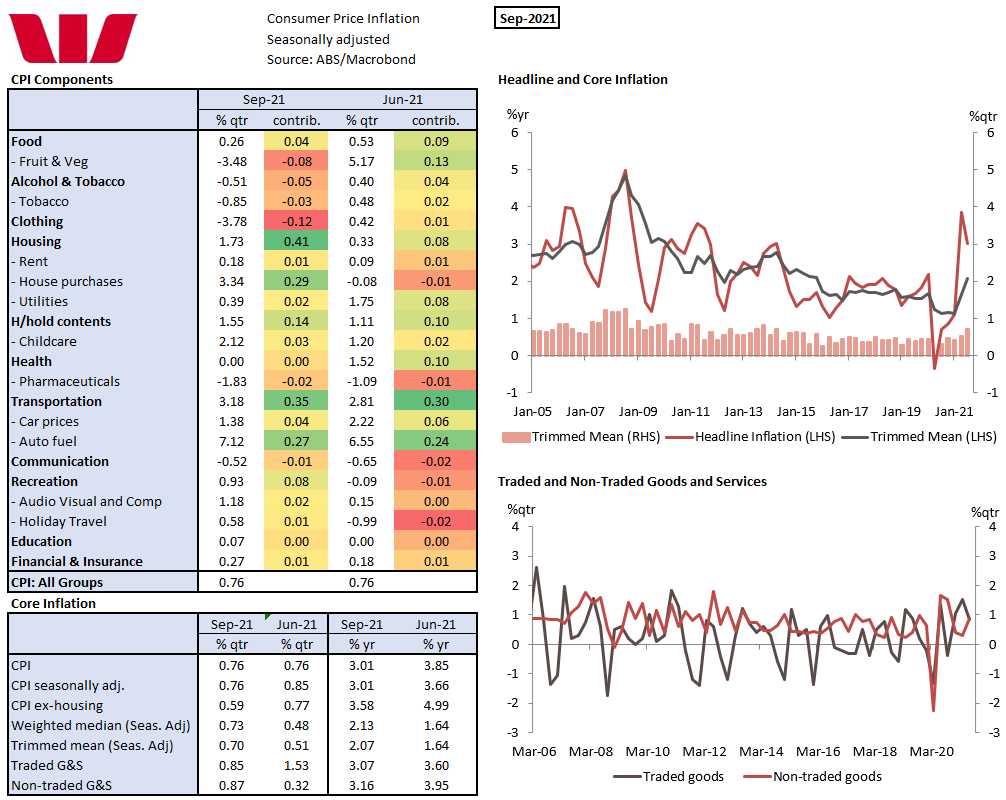

Headline CPI 0.8%qtr/3.0%yr; trimmed mean 0.70%qtr/2.1%yr, weighted median 0.73%qtr/2.1%yr.

Inflation came as expected with the September quarter CPI lifting 0.8% vs. Westpac and market forecast of 0.8%. At two decimal places it was 0.76% so a soft 0.8%.

The annual pace eased back from 3.8%, the fastest pace in 12 years, to 3.0%. As we noted in the June CPI update, the acceleration to almost 4%yr was due to base effects of the negative prints in 2020 due to government grants and subsidies. As such, this was expected to be a transitory blip in inflation.

The big surprise was the 0.7% rise in the trimmed mean taking the annual pace to 2.1%yr. This is the first time the trimmed mean inflation has been greater than 2.0%yr since September 2015. At two decimal places the trimmed mean rose 0.70%; for note the weighted median gained 0.73% for 2.1%yr.

The ABS reports that most significant price rises were for new dwelling purchase by owner-occupiers 3.3% (greater than Westpac’s forecast for 1.8%) and auto fuel 7.1% (Westpac forecast 5.9%).

In our preview we argued there was a high degree of uncertainty about dwelling prices as the current level of dwelling prices in the CPI are 4.7% below where they could be without the application of the HomeBuilder (and state government) grants. Our forecast for a 1.8% rise in dwelling prices incorporated a 1.5% rise in the underlying price paid by consumers with a smaller share of sales being supported by grants. In the end the ABS reported that the underlying prices paid rose 3.0% so most of the gain was fundamental with only a small proportion due the unwinding of the grants. This means the wedge between the prices paid and prices reported in the CPI is still a significant 3.7%.

On the low side of expectations for the quarter was alcohol & tobacco (-1.5% vs 0.9%), clothing & footwear (-3.8% vs 0.2%) and car prices (1.4% vs 2.4%).

The ABS reports that strong demand and supply disruptions have put upward pressure on prices for durable goods such as furniture and motor vehicles since the start of the COVID-19 pandemic. On the high side of expectations, as well as the already note dwelling prices (3.3% vs 1.8%) and auto fuel (7.1% vs 5.9%) there was audio visual & computing (1.2% vs 0.3%) and household contents & services (1.6% vs 0.7%). We will break down the granular data in our deeper dive to see if there are any signs this may be more than just a transitory bounce in prices post the re-opening of the economy.

The September quarter CPI was still under the push/pull influence of changing government support, subsidies and grants even if it has significantly fade. Now we are starting to see signs of prices adjust as the economy reopens just as there are global supply chain disruptions and local labour shortages. We are currently looking for core inflation to peak at just under 3% in late 2022 before easing back though 2023 and thus will be looking for signs in the September quarter CPI that we have to adjust our thinking.