{kind=link}

Personal income and spending numbers will be the highlight of the data flurry out of the United States on Wednesday (15:00 GMT), before investors turn their attention to the minutes of the Federal Reserve’s November policy meeting at 19:00 GMT. Rising virus restrictions across the US have dented the short-term outlook and a soft set of numbers would further pile pressure on the Fed to do more. The minutes might offer some clues as to whether monetary easing is forthcoming in December. Should expectations of Fed stimulus receive a boost, the dollar is likely to extend its downward drift.

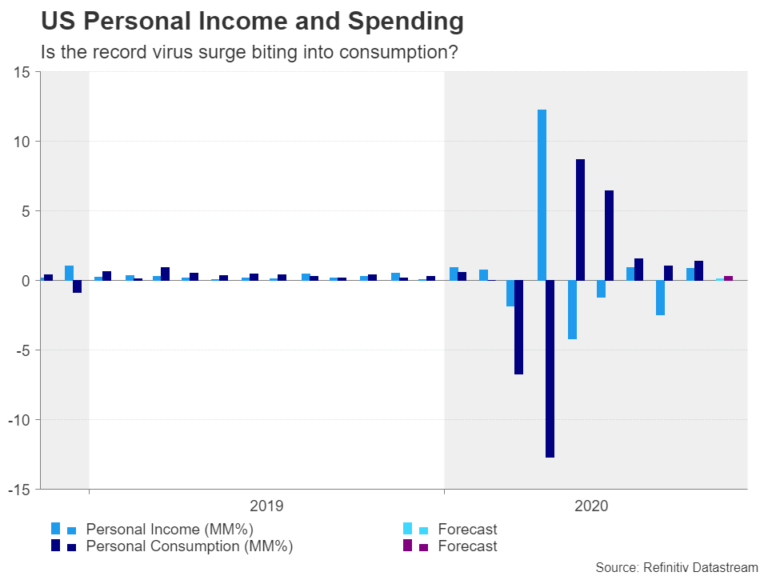

Are US consumers swimming against the tide?

Daily cases of COVID-19 are rising at a record pace again in America and whilst mask mandates, curfews and business curbs are on the up in many states, there is no prospect of broader lockdowns being imposed across the country like in Europe. However, soaring death and hospitalization rates are probably enough to discourage people from taking unnecessary trips to their local shopping mall. The rapid worsening of the virus spread is expected to have weighed on consumer sentiment in October, with personal consumption forecast to have grown by 0.3% month-on-month, slowing considerably from 1.4% in September.

Another drag on consumption is likely to have been the weaker growth in incomes. With Trump’s $300-a-week temporary extension of the $600-a-week federal unemployment benefit having expired in September, personal incomes possibly took a significant hit in October. Subdued wage growth over the period also does not bode well for how much more money people had in their pockets and expectations are for personal income to have increased by just 0.1% m/m in October.

Not all doom and gloom

Looking at the other data, the core PCE price index – the Fed’s preferred inflation gauge – is forecast to have ticked lower to 1.4% year-on-year. If confirmed, this would underscore the muted trend in price pressures, though more recent surveys point to a notable pick-up in input costs for businesses. There could be some relief from durable goods orders due at 13:30 GMT as they are projected to have increased for the sixth straight month, by 0.9% m/m, while the second estimate of third quarter GDP growth could be revised slightly higher.

A Mnuchin upset to Fed’s plans

Any negative surprises in the above data, particularly in personal spending, would heighten expectations that the Fed will ramp up its asset purchases in December. However, the gloomier picture might not be reflected in the minutes of the November 4-5 policy meeting when the recovery was seemingly on a firmer footing. In fact, the economic outlook has taken several dramatic turns lately, as apart from the darkening cloud looming over the winter months, the Fed has been stripped of some of its virus fighting weapons by Treasury Secretary Steven Mnuchin.

The discussion on whether to extend all of the emergency lending facilities before the year-end when they are set to expire likely dominated the November meeting. But with programs such as the Main Street Lending Facility as well as the facilities for buying corporate and municipal debt not being eligible for renewal after Mnuchin pulled the plug on them, policymakers will need to revisit their discussion in December to come up with alternative measures to shore up confidence in the markets.

Hence, the focus for investors from the now ‘outdated’ minutes will be to try and get a sense of how many FOMC members were open to boosting the monthly size of asset purchases as early as December.

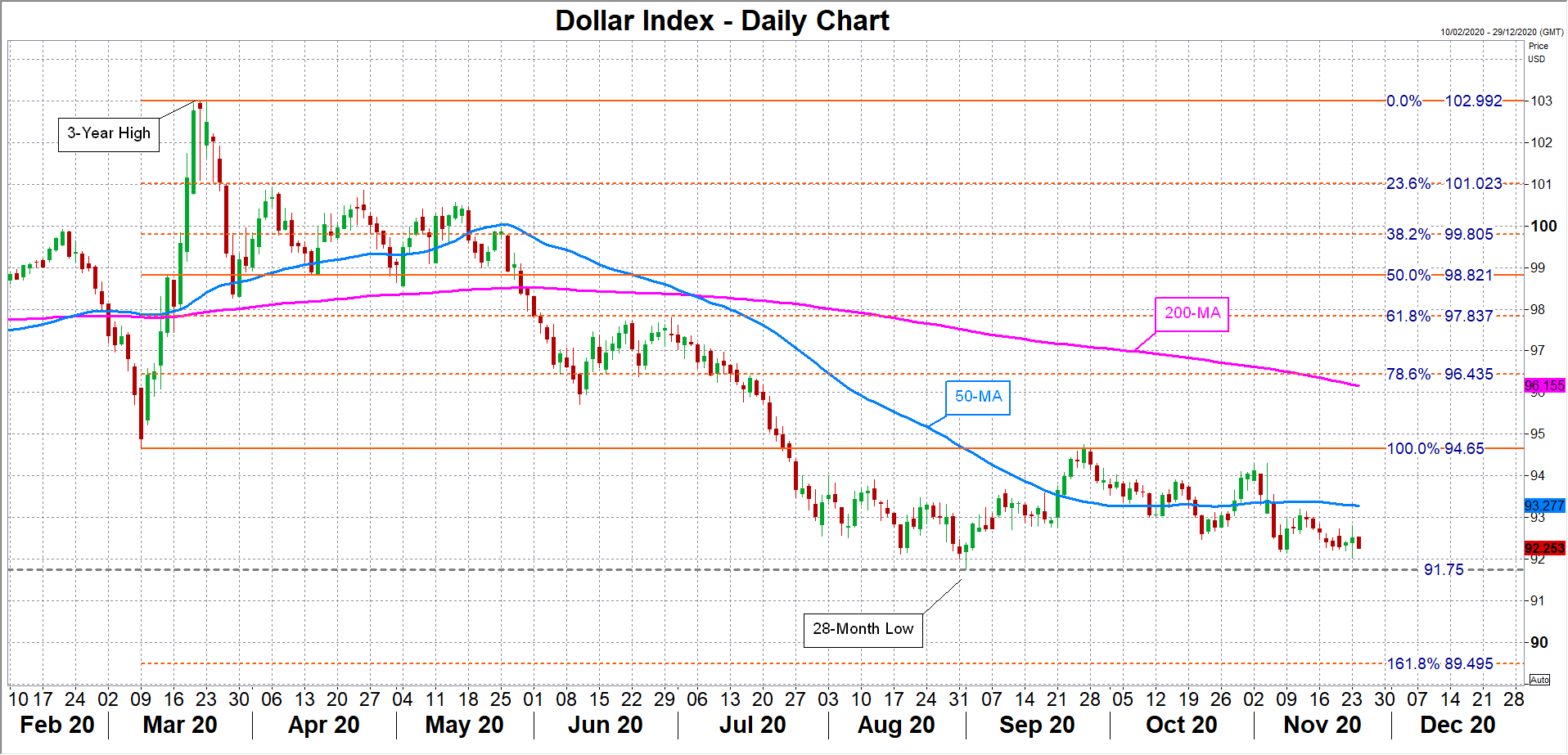

Dollar on the slide

Having brushed a 2½-month trough this week against a basket of currencies, the US dollar is at risk of sliding to fresh multi-month lows if Wednesday’s numbers add to the economic worries and the Fed is somewhat more dovish than anticipated in its minutes. The dollar index could easily slip below the 91.75 support, which was the September low, in such a scenario. Breaching the 91.75 barrier would open the way for the 161.8% Fibonacci extensions of the March upleg at 89.50.

If, however, the upcoming data do not raise any alarm about the recovery and the minutes give little away about December policy action, the dollar index could make its way back towards its 50-day moving average (MA), currently at 93.28. A successful climb above the 50-day MA would turn attention to the September top of 94.74.

In the absence of fresh direction from this week’s releases, traders should keep a close watch on Fed speakers in the run up to the December 15-16 meeting. Two further unemployment benefits will lapse at the end of December unless Congress strikes a last-minute stimulus deal and so policymakers might not necessarily be reassured from any signs of strength in the latest indicators.