{kind=link}

- With the spread of the corona virus, uncertainty is increasing for the Chinese economy and thus the global economy and financial markets. The brewing Chinese recovery is likely to take a hit in the short term and GDP could be reduced by up to one percentage point in H1.

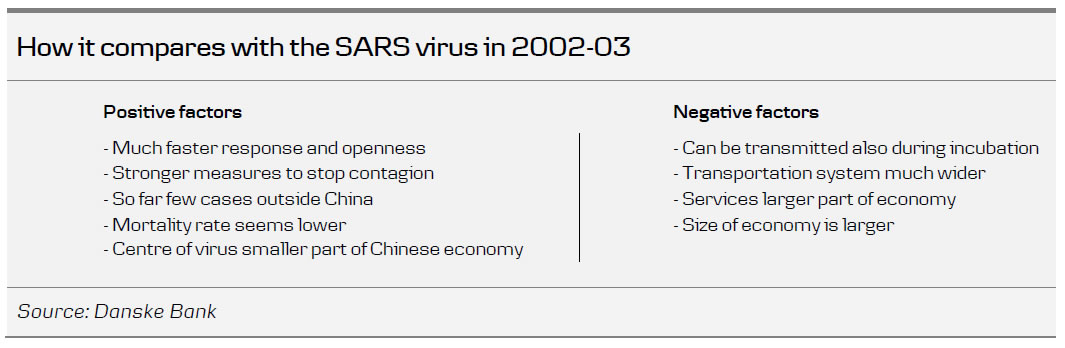

- The virus is at an early stage and it is difficult to judge how much it can spread before it gets under control. On the positive side, the government response has been faster and more drastic measures have been taken to contain the virus compared to the SARS epidemic in 2002-03.

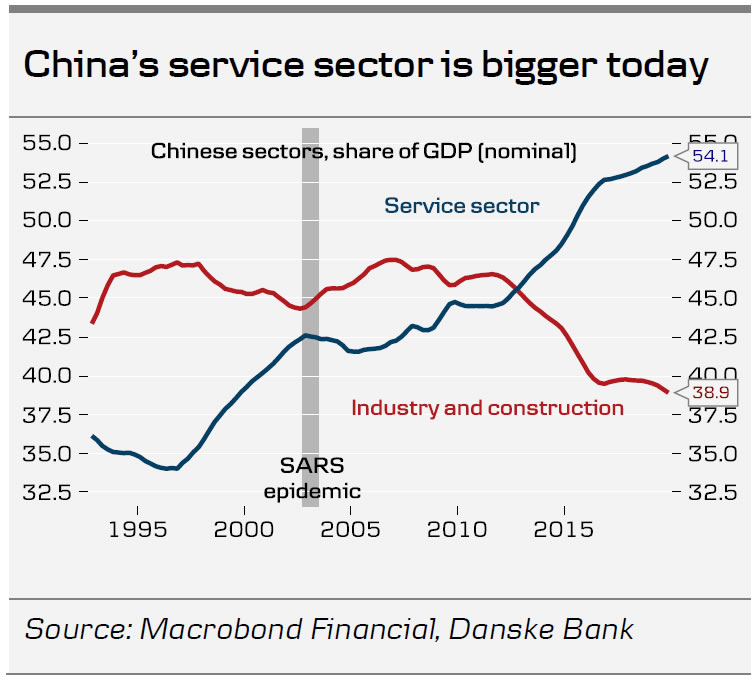

- On the other hand, the virus seems more contagious than SARS and China’s transport system is significantly wider today. The Chinese New Year holiday that started last week poses a heightened risk of contagion. The economic impact is likely to be bigger this time as the service economy is a much higher share (54%) of the economy today compared with the 2002-03 SARS outbreak (42%).

- The Chinese economy is also a much bigger driver of global growth. A mitigating factor is that mainly the service sector should be hit, where the import content is small. However, retail sales could also suffer, which could hurt imports and inflation could see another push higher from reduced production in Hubel.

- The SARS epidemic lasted 3-4 months but it is hard to say if this is any guide. While the government response is faster, the new virus seems to be spreading faster. It is too early to judge when it will get under control.

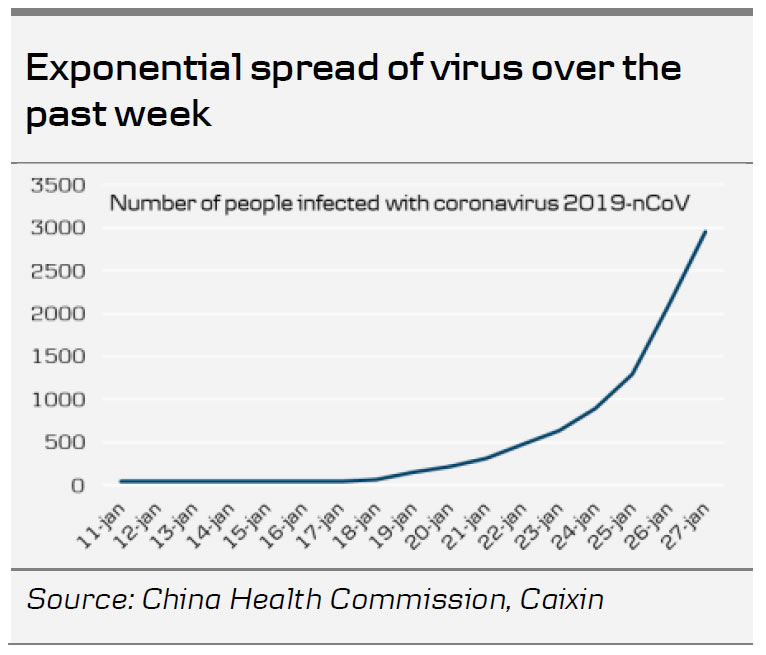

How fast is the virus spreading?

As of Monday morning 27 January the number of infected people has increased to 2,796 up from around 200 cases one week ago. 80 people have now died up from three a week ago. The virus has spread to all but one of China’s 31 provinces. The virus has also been registered in 11 other countries, which have reported a total of 40 cases with Thailand being hit the most with eight cases, while five cases have been registered in the US.

At a press conference on Sunday China’s top health official said the virus’s transmission ability is getting stronger and that it also spreads during incubation time. It means a person can transmit the virus before any symptoms have shown up. It makes screening at airports etc. less effective. It also came out on Sunday that as much as 5 million people had already left Wuhan, the centre of the virus, before the lockdown started on Thursday last week. Wuhan is a major transportation hub with 700,000 passengers normally passing through three stations. Some concerning stories circulate from Wuhan about people with symptoms that stay home out of fear of getting more sick at the crowded hospitals.

How does it compare with the SARS virus in 2003?

The SARS virus continued to spread for 3-4 months in the beginning of 2003 before it got under control. Around 8,000 people were registered and 770 people died. Hence, it seems the mortality rate was higher than with the current virus. SARS was first registered in November 2002 in the Guangdong province but China did not report it to WHO until 10 February 2003, when 305 cases were reported and five people had died. The virus spread to many Asian countries and Canada was also hit with 44 people dying from the virus. The virus peaked around May and WHO declared the outbreak contained in early July.

Compared to 2003 the authorities have responded much quicker and taken more drastic measures to stop the spread. China has expanded the number of cities in lockdown now covering a population of 56 million people. Cultural sites such as the Forbidden City and parts of the Great Wall have been closed and movie theatres have also shut in many cities. China is building two new hospitals in Wuhan city, which are set to be ready within weeks. A leading group has been set up under the Standing Committee of the Politburo (the leadership of China) with the responsibility of leading the fight against the virus. Premier Li Keqiang will be heading the efforts to fight the virus, which means decision power will be strong compared to if decisions had to be taken at a lower level.

However, while the response is quicker the risk of contagion is higher today due to the much wider transportation network with a huge amount of trains, flights and cars compared to 2003. Around 50 trains per day were leaving from Wuhan to the big cities in China until the city was put in lockdown. The virus is also spreading at a critical point in time as people left last week for the Chinese New Year celebration on Friday last week. It is a time of year when typically 3-400 million people travel to reunite with their family. Finally, the virus is more contagious this time as it can also be transmitted during incubation time.

How will it affect the economy this time?

During the SARS outbreak retail sales took a hit but overall growth was not affected much. However, the economic impact is likely to be bigger this time.

- The service sector is likely to take the main hit and is much bigger today (54% of GDP) than in 2003 (42% of GDP). People will stay home from movie theatres, concerts, restaurants and reduce travelling. China’s middle class is much bigger today and typically spends more on entertainment than low-income groups.

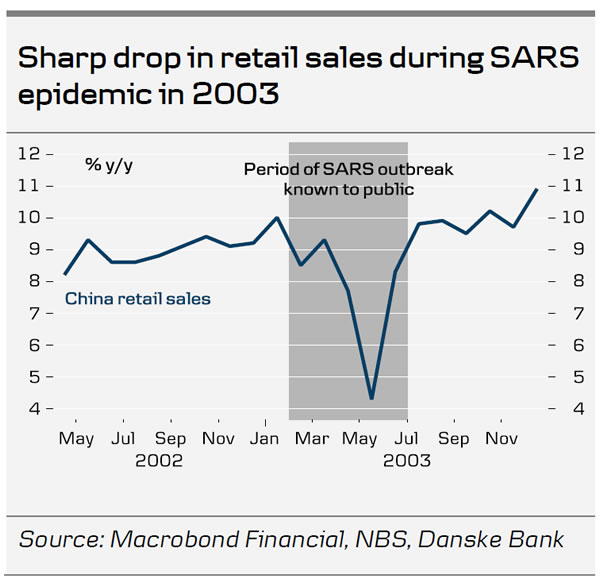

- Retail sales took a hit in 2003 with annual growth falling from 10% to 4.5% at the peak of the crisis. People stayed home from markets and shopping streets to avoid contagion. A similar effect is likely today, although it is likely to be mitigated by a much wider degree of online sales.

- The consumer sector has already been hit from higher food prices due to the African swine fever that has pushed up inflation and eroded purchasing power. The lockdown of pretty much all of the Hubei province will likely add to the upward inflation pressure.

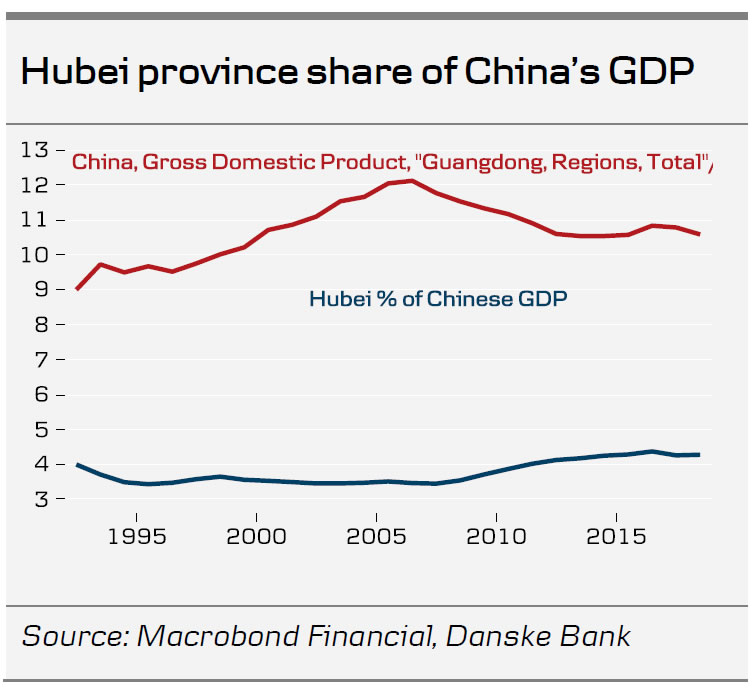

- The Hubei province is likely to see a significant drop in GDP due to the lockdown. Hubei is 4% of China’s overall economy, so a 20% drop in GDP could subtract 0.8 percentage points from China’s GDP, all else equal.

- The New Year holiday is set to be extended for another week in several areas, which will lead to a direct reduction in output in the short term.

- Finally, the virus hits at a time when the economy is already fragile due to lingering effects from the trade war. The rising uncertainty could once again put investments on the backburner until it is clear how serious the effects from the virus will be.

On the positive side, the Hubei province is a smaller part of the Chinese economy than during SARS when Guangdong was the centre of the virus. Guangdong is China’s biggest province with more than 100 million people and 11% of China’s GDP.

The Chinese government will likely aim to mitigate the negative impact through some stimulus. However, it is more difficult to counter the drag on GDP, as it is partly due to a supply shock that hits production in one province. The likely temporary nature of the shock also makes it difficult to calibrate how much to ease and for how long. However, we do expect some kind of response at least to underpin sentiment and monetary stimulus as well as possible tax cuts could be on the table.

At this stage it is very hard to judge to overall impact on the economy, but based on the above factors a hit of around one percentage point could be on the table. It is likely to be a temporary effect and to be compensated by higher growth when the virus has come under control. This was the case with SARS, where retail sales growth for a while was higher than before the virus, as pent-up demand had built up.

How much will it affect the global economy?

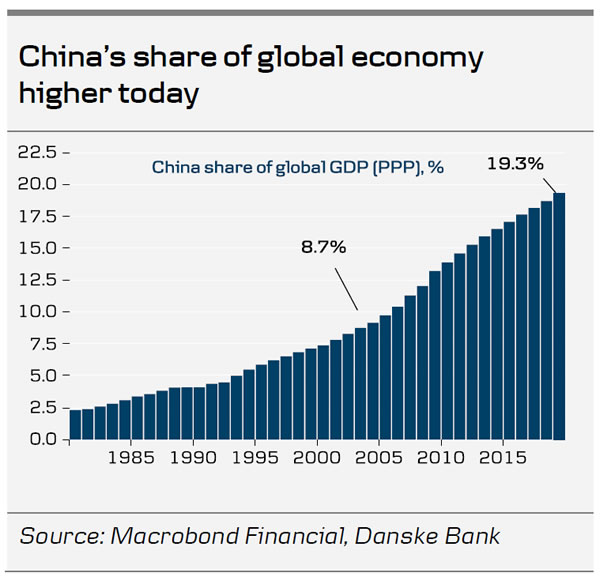

China’s economy is much bigger today than when SARS hit in 2003. The share of the global economy was around 9% in 2003 in PPP-adjusted terms and is 19% today. China is driving around one-third of global growth compared with around 20% in 2003.

A mitigating factor for the global economy is that the service sector is likely to take the biggest hit and the import content here is much smaller than in the manufacturing sector. The hit to the retail sector will also be felt among foreign companies but many of them produce goods for the Chinese market in China.

Nevertheless, there is likely to be some spill-over, not least due to the higher uncertainty, which hits at a time when sentiment is already low. Hence, there is a clear risk that the expected recovery in growth and PMIs could be somewhat delayed or at least be more muted. As in China, the effect should be temporary, though.

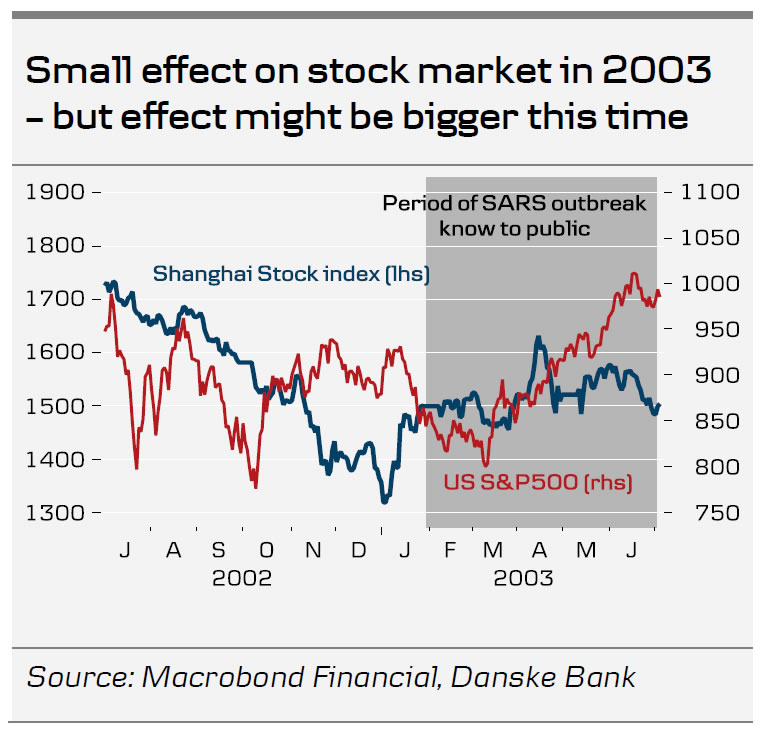

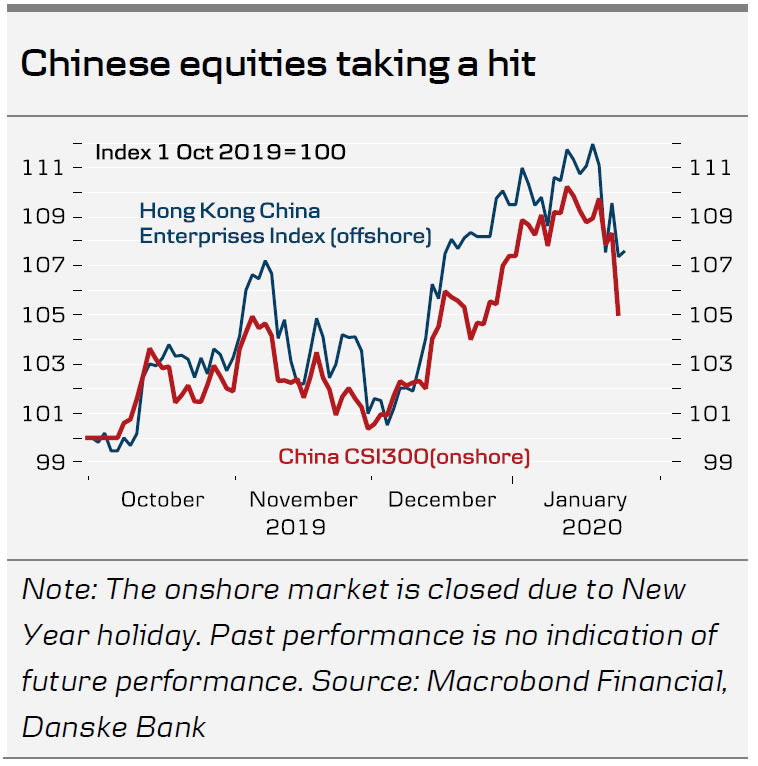

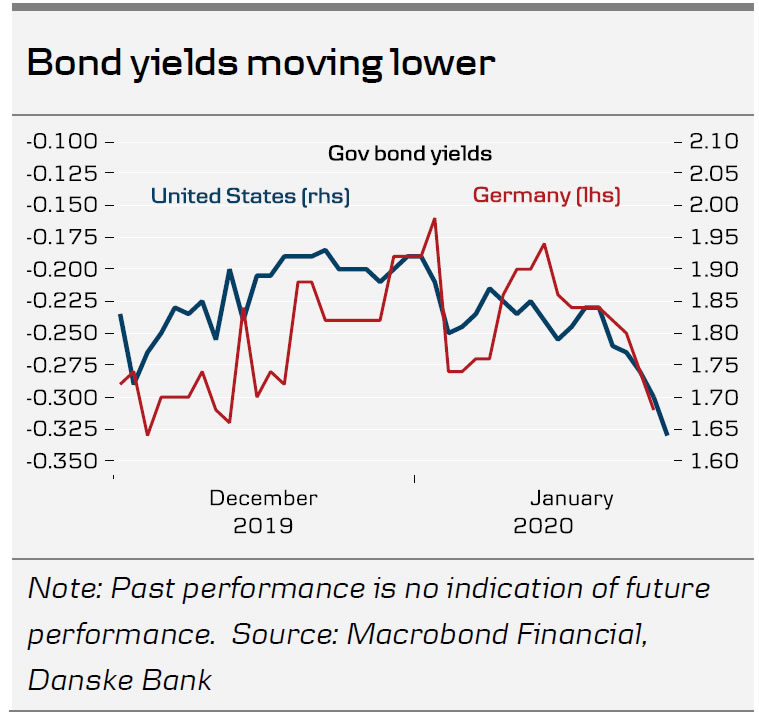

Global financial markets have also started to react with especially the Chinese markets taking a hit. Global bond yields and commodity prices have also moved lower. Given the strong rally in global equity markets in the beginning of the year, there is a risk that early profit taking triggers a correction due to the increasing uncertainty.

Conclusion: rising uncertainty as we enter unchartered waters

We are in unchartered waters as a virus of this kind has not taken place in the more modern economy that China is today with much wider transport networks and being more integrated with the global economy. A hit to the Chinese economy is inevitable at this stage but we have to wait and see how the virus develops to evaluate how big the hit will be and how long it will last.