{kind=link}

Australia hasn’t had the best start to 2020 as the bushfires that have been ravaging the country since October have only just started to subside, with the full economic impact yet to be seen. The December data – when the fires intensified – could reveal the extent to which the economy was hit by the devastating blazes. The first key report is Thursday’s employment numbers, due at 12:30 GMT. With the Reserve Bank of Australia already on an easing bias, the data will be closely watched by policymakers as the February 4 rate decision looms.

Mounting cost of bushfires could weigh on economy

Calls on the RBA to cut interest rates have been rising as the cost of the bushfires to businesses and communities mount. Looking at the available stats and rate cut expectations, however, the decision is far from straight forward and incoming data over the next 10 days will be crucial in making up policymakers’ minds.

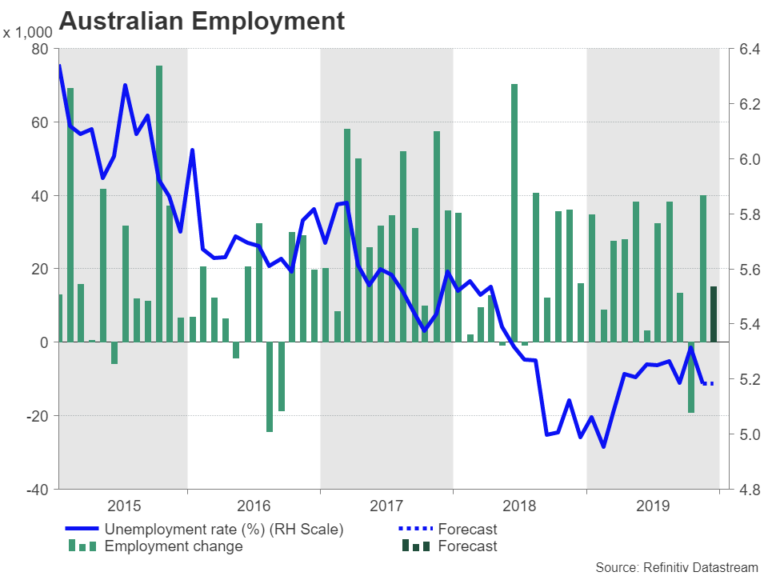

Based on November alone, the Australian economy appeared to be picking up some speed, with improvements seen in consumption, the labour market and the housing sector. However, the economic climate likely darkened towards the year-end as the country battled to bring the fires under control. There is already some evidence of this from the AIG services index, which tumbled 5 points in December, posting its first contraction in five months.

Jobs miss would fuel rate cut speculation

The risk to the upcoming releases is therefore to the downside and the first test will be Thursday’s jobs figures. Analysts are forecasting employment to have risen by 15k in December, easing from the prior month’s impressive gain of 39.9k. The jobless rate is forecast to have stayed unchanged at 5.2%.

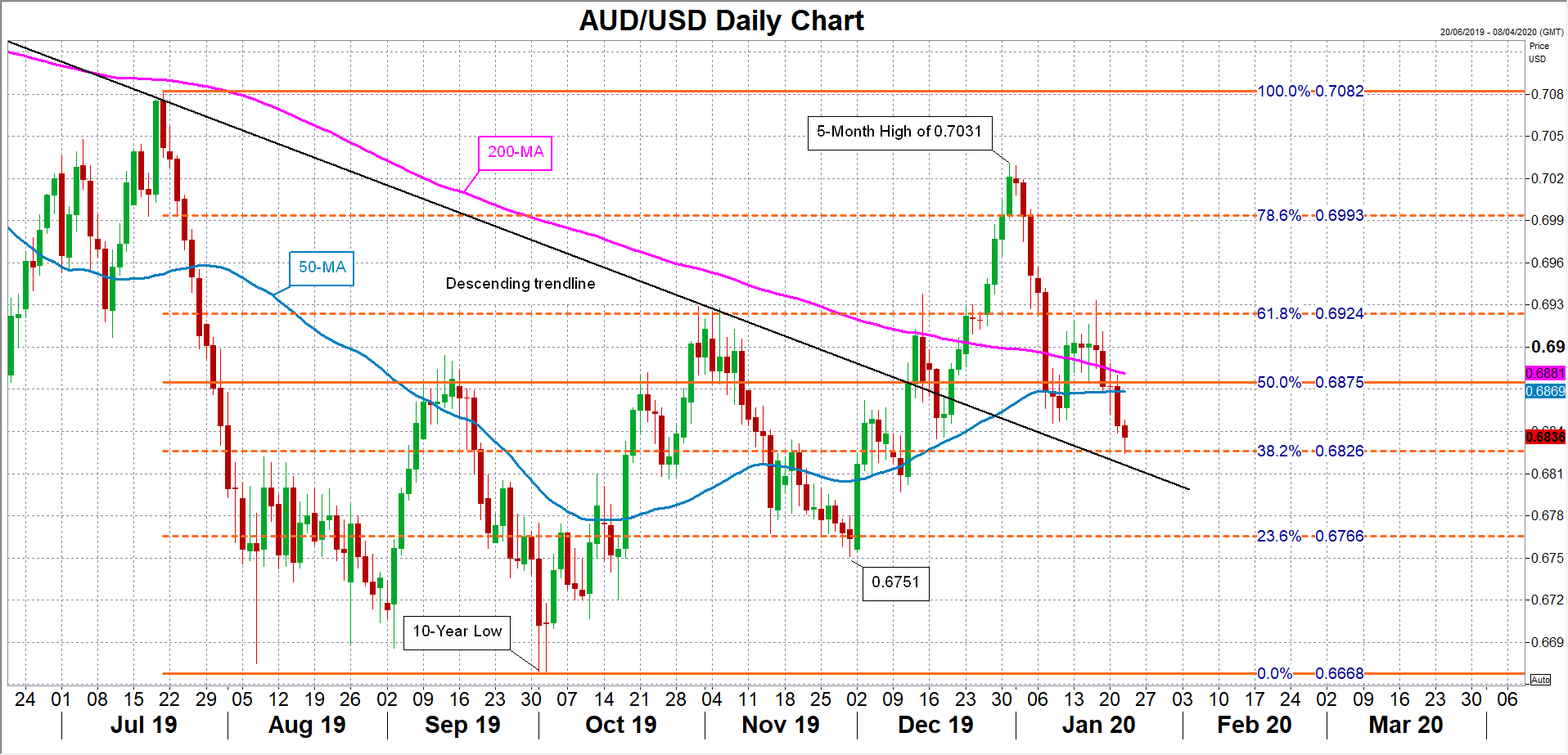

Investors are currently pricing about a 46% probability that the RBA will lower rates in February so the scope for markets to adjust their expectations should the data badly miss the estimates is quite large. A big repricing is likely to trigger a sharp sell-off in the Australian dollar, which took a tumble in early January. After a brief bounce, it appears to be back on the slide again, heading towards its descending trendline. Soaring rate cut odds could push the aussie back below the critical support of the trendline, turning the focus to the November swing-low of $0.6751.

Can easing trade tensions keep RBA on hold?

However, although the RBA has so far proven to be dovish leaning, slashing the cash rate pre-emptively three times in 2019, the bar for additional cuts may be higher than many analysts assume, especially now that trade tensions and other global risks have abated substantially. If the jobs numbers do not deviate much from the projections, the aussie is likely to see only a knee-jerk reaction and hold within its recent range as investors will prefer to wait for the IHS Markit PMIs on Friday and the Q4 inflation figures next week to form a clearer picture on how the economy ended 2019.

Another development investors and policymakers will be keeping an eye on is the outbreak of the coronavirus in China. The virus crisis is the last thing Australia’s struggling tourism industry needs, which has already been badly hurt by the deadly bushfires. Every year, millions of Chinese tourists travel abroad for the Lunar New Year holiday, with Australia being a favourite destination. A further blow to the Australian economy from the outbreak could prompt the RBA to act swiftly now rather than to save its limited firepower for a rainier day.