{kind=link}

Dollar and Canadian Dollar remain the strongest major currencies for the week, but both are losing momentum. Markets are rather unmoved by the highly anticipated FOMC minutes released overnight. DOW closed down -0.01% t 21478.17 after struggling in tight range for all the session. S&P 500 closed up 0.15% at 2432.54. NSADAQ is the more vulnerable one even though it closed up 0.67% at 6150.86. 10 year yield edged higher to 2.357 but failed to extend recent gain and closed down -0.012 at 2.334. In other markets, gold is trying to stabilize 1225 after diving to as low as 1216.5 earlier this week. WTI crude oil suffered steep selloff yesterday, from 47.3 to 44.51 and is now at around 45.3. The selloff in oil price accompanied the pull back in Canadian Dollar.

Fed policy makers divided over timing of balance sheet reduction

The FOMC minutes for the June meeting unveiled that members were divided over the timing of balance sheet reduction while there was also discussion over the recent inflation weakness. At the meeting, the Fed raised its policy rate, by 25 bps, to a target range of 1-1.25%. The minutes reflected the division among members regarding the timing of balance sheet reduction as well as how it would affect the path of interest rate hike. While "several preferred to announce a start to the process within a couple of months", "some others emphasized that deferring the decision until later in the year would permit additional time to assess the outlook for economic activity and inflation".

Concerning the interaction with the monetary policy, the minutes revealed that "several participants indicated that the reduction in policy accommodation arising from the commencement of balance sheet normalization was one basis for believing that, if economic conditions evolved broadly as anticipated, the target range for the federal funds rate would follow a less steep path than it otherwise would". Yet, "some other participants suggested that they did not see the balance sheet normalization program as a factor likely to figure heavily in decisions about the target range for the federal funds rate". Some members holding the latter view "judged that the degree of additional policy firming that would result from the balance sheet normalization program was modest".

More on FOMC minutes:

Also:

- FOMC Minutes: Fed Likely To Announce Start Of QT In September

- FOMC Debated Inflation Weakness in June, Divided on Timing of Balance Sheet Normalization

IMF Lagarde: Financial vulnerabilities present an immediate concern

IMF Managing Director Christine Lagarde warned in a blog post that "financial vulnerabilities present an immediate concern." And, "after a long period of favorable financial conditions, including low-interest rates and easier access to credit, corporate leverage in many emerging economies is too high." In Europe, she noted that "bank balance sheets still need repair following the crisis." In China, "a faster-than-projected expansion – if it continues to be fueled by rapid credit and increased spending – would potentially lead to unsustainable public and private debt in the future".

Australia trade surplus widened

From Australia, trade surplus widened to AUD 2.47b in May, up from AUD 0.09b and beat expectation of AUD 1.11b. That was driven by the 9% growth in exports over the month while imports rose 1%. However, it should be noted that coal exports jumped 62% over the month, for supply was disrupted back in April after Queensland was hit by cyclone in late March. Aussie remains the weakest major currency for the week as markets were dissatisfied that RBA didn’t turn hawkish, following other major central banks.

ECB accounts and US data to highlight the day

More market moving events are scheduled for today. ECB meeting accounts will be a major focus as markets will look into how policy makers are ready for tapering asset purchases. Germany will release factory orders while Swiss will release CPI. US ADP employment, jobless claims and ISM services will be featured in US session. After the release, markets will get a sense of how tomorrow’s non-farm payroll report would be like. US will also release trade balance. From Canada, trade balance and building permits will be featured

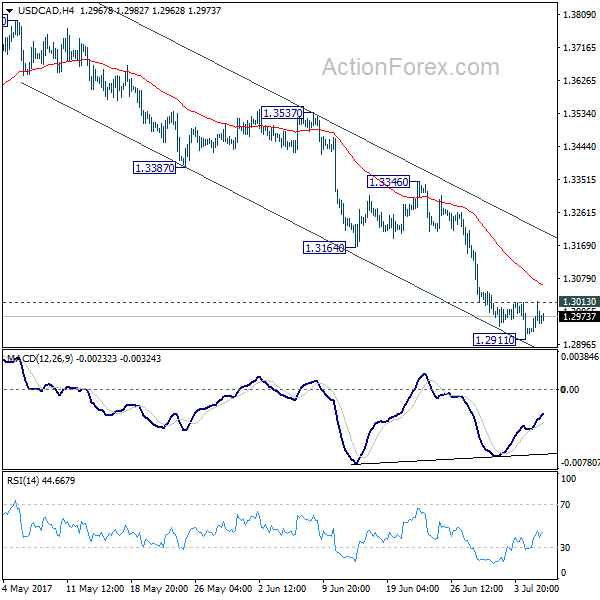

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2892; (P) 1.2953; (R1) 1.2994; More….

A temporary top is in place at 1.2911 after touching 1.3013 minor resistance. Intraday bias in USD/CAD is turned neutral first. Considering bullish convergence condition in 4 hour MACD, break of 1.3013 will indicate short term bottoming. In such case, stronger rebound would be seen back to 1.3164/3346 resistance zone first, before staging another fall. Overall, we’d expect decline from 1.3793 to extend later and sustained trading below 1.2968 cluster support, 61.8% retracement of 1.2460 to 1.3793 at 1.2969 will pave the way to retesting 1.2460 low.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The second leg should have finished at 1.3793. Break of 1.2460 will extend such correction to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we’d look for strong support from there to contain downside and bring rebound. However, firm break there will target 100% projection of 1.4689 to 1.2460 from 1.3793 at 1.1564.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) May | 2.47B | 1.11B | 0.56B | 0.09B |

| 06:00 | EUR | German Factory Orders M/M May | 1.80% | -2.10% | ||

| 07:15 | CHF | CPI M/M Jun | 0.00% | 0.20% | ||

| 07:15 | CHF | CPI Y/Y Jun | 0.30% | 0.50% | ||

| 08:10 | EUR | Eurozone Retail PMI Jun | 52 | |||

| 11:30 | USD | Challenger Job Cuts Y/Y Jun | 9.70% | |||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:15 | USD | ADP Employment Change Jun | 180K | 253K | ||

| 12:30 | CAD | Building Permits M/M May | -0.20% | |||

| 12:30 | CAD | International Merchandise Trade (CAD) May | -0.4B | |||

| 12:30 | USD | Trade Balance May | -46.3B | -47.6B | ||

| 12:30 | USD | Initial Jobless Claims (JUL 01) | 243K | 244K | ||

| 14:00 | USD | ISM Services/Non-Manufacturing Composite Jun | 56.5 | 56.9 | ||

| 15:00 | USD | Crude Oil Inventories | 0.1M |