{kind=link}

ASX to fall at open

ASX Dec Futures alongside the broader equity complex has performed poorly overnight. The Australian benchmark nears 6,587 downside support and could look to test it if negative momentum carries through. Overall, we expect to see ASX Cash open 22pts lower led by weakness in oil sensitive stocks given Brent’s overnight sell-off, as well as, banking stocks subdued by the challenging industry conditions seen in ANZ’s (ANZ.AX) soft result yesterday. ANZ flagged tighter margins driven by low interest rates.

US-China doubtful

A couple of US-China headlines hit the wires overnight driving markets moderately risk-off with month-end rebalancing needs also in the mix. Building on the cancellation of the APEC Chile Summit where Trump and Xi were supposedly set to sign-off on phase 1, a Bloomberg report questioned the possibility of a long-term trade deal with Trump. This saw yields turn lower while USDCNH reacted negatively, jumping +25pips in the hour of the announcement away from 7.028 October lows. It wasn’t however all negative with Trump confident that a “new location will be announced soon”. Risk-on/risk-off proxy USDJPY was the weakest performer in G10 space shaving -60pips to test 108.

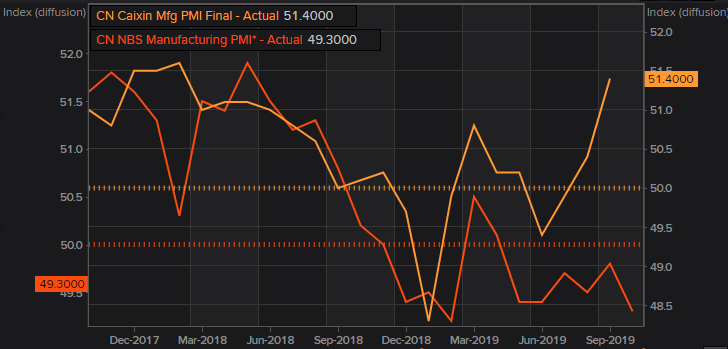

Caixin PMI up ahead

Keeping with the China theme, we catch Caixin Mfg PMIs at 12.45pm AEDT today. Forecasted at 51.0, Caixin tends to come in stronger than the official read, which missed expectations yesterday printing 49.3 vs 49.9 consensus. A weak print here from Markit’s Mfg PMI is likely to draw a negative risk reaction as markets flag the manufacturing malaise in China.

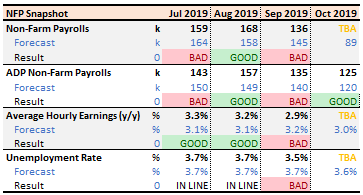

Key figures up ahead

As a reminder, markets catch Oct. US Non-farm Payrolls, Average Hourly Earnings and Unemployment at 11.30pm AEDT tonight. Not long after, we also get Oct. ISM Manufacturing PMI at 1.00am AEDT. We expect risk sentiment to react to the event and volatility to heighten leading into it. For a more in-depth view, catch what our London team thinks about the event here.