{kind=link}

Tail risk of no deal Brexit has diminished further

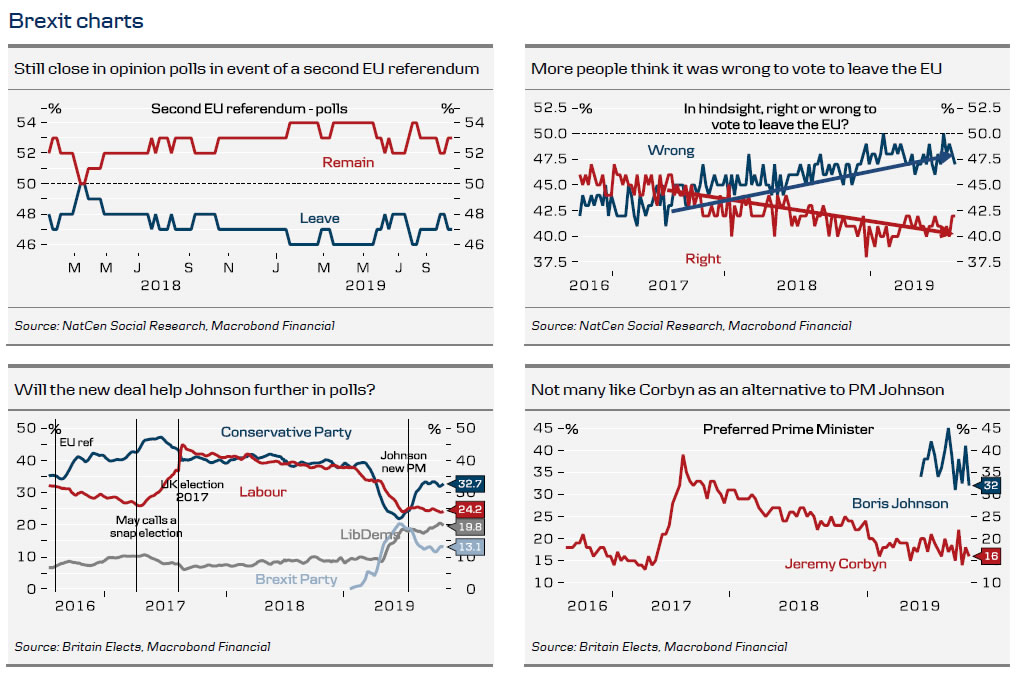

After the UK and EU27 reached a new Brexit deal today, the next uncertainty is whether Prime Minister Boris Johnson can get it over the finish line when the deal is put to a ‘meaningful vote’ on Saturday. We doubt it , although never say never. The DUP has rejected supporting the deal, so it will be very very difficult for Johnson to get a majority in the House of Commons (which would have been difficult even assuming the DUP was on board). We still doubt the pro-Brexit Labour MPs will vote in favour of a deal, which is harder than that put forward by Theresa May. Some of the moderate Conservatives, who Boris Johnson expelled from the party last month, have also hinted they will reject the deal. Our base case remains another extension followed by a snap election.

In our view, it is natural to ask why Johnson has reached an agreement with the EU knowing it will be difficult to get it through Parliament. We believe there are two reasons. First, it some MPs may get cold feet when the actual voting takes place. One way of addressing this is asking EU leaders to state they will reject another extension, i.e. stating it is ‘this deal or no deal’. Second, Prime Minister Johnson and his team probably think with his new Brexit deal he will stand stronger against Jeremy Corbyn in a potential election campaign , as the Brexit deal is cleaner than that of Theresa May. In the event he won the election, he could pass the Brexit deal without the need of the DUP.

Despite Prime Minister Johnson’s deal being unlikely to pass Parliament on Saturday, we believe the tail risk of a no-deal Brexit even after a potential election has diminished further. This also partly explains the positive risk rally we have seen on the renewed Brexit optimism. While we previously feared a Johnson victory in a snap election would lead us to a no-deal Brexit, this is no longer the case. In our opinion, it is difficult to see a path to a no-deal Brexit now.

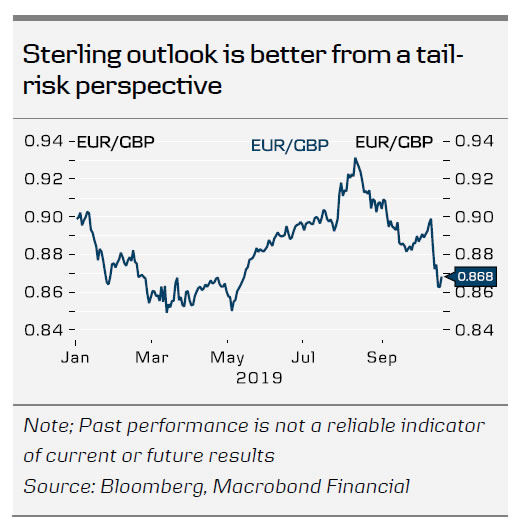

EUR/GBP: outlook better from a tail-risk perspective

We stick to our view that the optimism will not pass the test of the UK’s Parliament. As such, markets appear rather optimistic across GBP/USD, EUR/USD, USD/JPY, AUD, SEK, yields and so on. In our view, if a deal does go through, a large part of that move is already priced. Will all of this need to be unwound in the event of an extension when a deal is not done in October, as we believe it will not? In our opinion, the answer is some but maybe not all.

As of today, an extension with a deal on the table would help the Conservatives in the (likely) upcoming election. If Johnson won an absolute majority, then pricing would probably be fine as is, because he would then be able to push the deal through without the DUP (or others) blocking it. Hence, if anything has changed in terms of politics, it might not be that we get a deal in October but rather that we can get one later and the Conservatives are better positioned in an election with a deal on the table. In other words, the sterling outlook is better from a tail-risk perspective. In the bigger picture, we expect to be trading 0.85-0.90, depending on the mood of the day. Marginally, we would say the risk here is that we end up going higher in EUR/GBP.