{kind=link}

U.S. Highlights

- CPI report – the only key data release this week – confirmed that inflation remained tame in September. Both headline and core inflation registered a muted 0.1% increase on the month, leaving the readings flat on a year-over-year basis.

- Meanwhile, the JOLTs survey showed that worker demand had softened over summer. The number of job openings fell in August on a year-on-year basis – a third drop in as many months.

- Unless a breakthrough in the U.S.- China trade impasse is reached later today, benign inflation and further signs of the domestic economy cooling off should lead to an even broader agreement for further monetary easing among the FOMC members when they meet later this month.

Canadian Highlights

- Oil prices rose as an Iranian oil tanker was hit by missiles on Friday.

- The Canadian labour market posted a stellar performance in September, adding 53.7k jobs. Wage growth picked up as the unemployment fell to near-historic lows.

- The housing market continued to recover, contributing to an acceleration in mortgage credit growth.

- Given the evolution of the data, the Bank of Canada appears likely to remain on the sidelines when it meets at the end of this month.

U.S. – Fed Leaves the Door Open for Another Cut

This was another busy week for markets. Lingering concerns about the health of the global economy continued to weigh on sentiment after a couple of dour speeches from the leaders of the IMF and World Bank early in the week. However, the mood improved as the week progressed, with equities gaining and bonds selling off. Risk-on sentiment was buoyed by trade talk hopes ahead of the much-anticipated meeting between President Trump and Chinese Vice Premier Liu later today. Investors also welcomed signs of progress in the Brexit talks between the UK and Ireland.

The new leaders of the IMF and World Bank warned about the deteriorating global economic backdrop ahead of their annual meetings next week. The new head of the IMF, Kristalina Georgieva, said that the global economy is now in a “synchronized slowdown”, and that the IMF expects slower growth than last year in 90% of the world. The new head of the World Bank, David Malpass, in turn highlighted the long list of looming risks, such as “Brexit, Europe’s recession, and trade uncertainty,” which may lead to a further downgrade to their global growth estimate.

Chair Powell expressed similar concerns in his speech this week, acknowledging that the U.S. economy has slowed. He also reaffirmed that while the 50 basis point reduction in the fed funds rate so far is providing support, the FOMC committee will continue to assess incoming data signals on a meeting-by-meeting basis. The next meeting will take place at the end of October, and markets are expecting another quarter-point rate cut. Powell’s speech this week did not dispel those expectations, with the chairman reiterating that “policy is not on a preset course”.

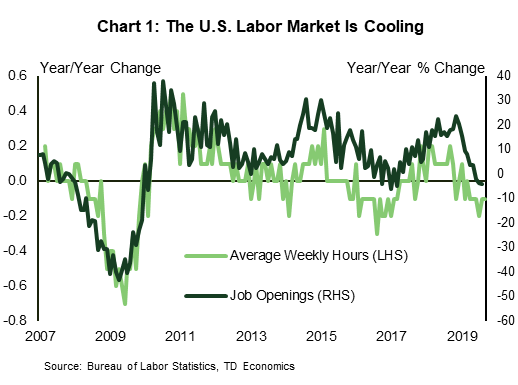

While data was sparse, with CPI being the only main release, the FOMC meeting minutes, were noteworthy. The September minutes revealed that most participants were in favor of a 25 basis point cut last month to cushion the domestic economy from external headwinds. It appears that the argument for further monetary accommodation has only strengthened since then. The ISM Manufacturing index has moved deeper into contractionary territory, service sector activity has moderated, and wage and job growth have slowed. Echoing those trends, the JOLTs survey this week showed that worker demand had softened over the summer. The number of job openings in August declined 4% from a year ago, falling for the third consecutive month and mirroring the decline in average weekly hours (Chart 1).

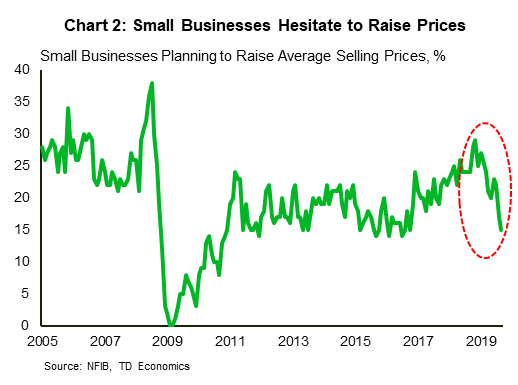

Separately, the NFIB small business confidence index showed that businesses may be stuck between a rock-and-a-hard place, as they face rising costs (especially for labor), but are unable (or unwilling) to increase selling prices (Chart 2). Indeed, despite new tariffs coming into effect in September on many consumer goods, inflation remained tame. Both headline and core inflation registered a muted 0.1% increase on the month, leaving the readings flat on a year-over-year basis at 1.7% and 2.4%, respectively. Unless a breakthrough in the trade impasse is reached later today, benign inflation and further signs of the domestic economy cooling off should lead to even more agreement at the FOMC table for the need of at least another rate cut this year.

Canada – Labour Market Still In High Gear

Canadian financial markets saw some volatility this week amid news on the U.S.-China trade talks. With hope for a deal rising on Friday, the TSX settled at a level close to where it was on Monday, up by a middling 0.5% at the time of writing. Oil prices saw a jump on Friday as an Iranian oil tanker came under attack. At the time of writing, WTI prices were up by around 3% on the week.

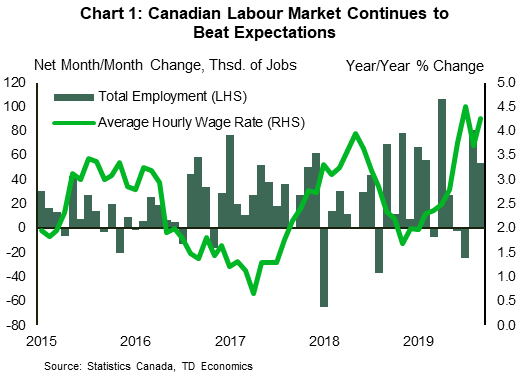

On the data front, employment figures grabbed the headlines with a blockbuster increase in hiring. Canada created 53.7k jobs in September, beating consensus estimates by nearly 50k (Chart 1). Even smoothing through the volatility, Canada is adding 40.4k jobs a month over the last six months, a stellar performance. The one blemish was that private sector hiring was down 21k on the month, offset by increases in self-employment (+42.1k) and the public sector (+32.6k). We caution into reading too much into these splits on a monthly level given their inherent volatility. With the surge in hiring, the unemployment rate dropped to 5.5%, just above the modern historical low of 5.4%. Moreover, wages appear to be responding to the tighter labour market (Chart 1).

The Canadian housing market has benefitted from the gains in jobs and wages. Homebuilding numbers were solid in September, with Ontario and B.C. seeing housing starts rise from August. The gain in B.C. was particularly encouraging, coming off the back of a significant decline in August.

The recovery in the housing market is also attributable to rapid population growth and lower mortgage rates. Population growth in Canada has been on a tear again this year, with the third quarter seeing the fastest increase in nearly 30 years. Mortgage rates too have been trending down, attracting more investment.

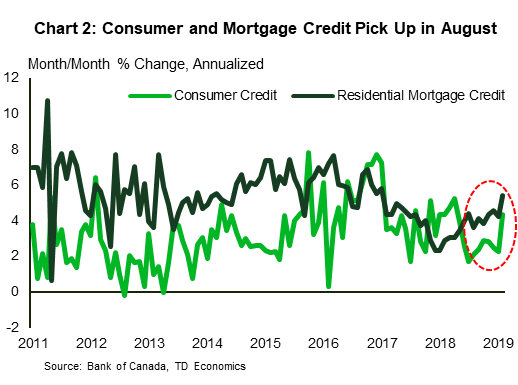

Indeed, lower mortgage rates has meant an acceleration in mortgage credit. Data released over this past weekend showed a strong pick-up in mortgage credit in August (Chart 2). But the buck didn’t stop there; consumer credit also surged, nearly doubling the growth rate observed in the first seven months of 2019. On the whole, household credit growth posted the strongest increase in two years and could signal an increase in household vulnerabilities.

The Bank of Canada will be watching these developments in credit growth closely as it remains a key area of concern. Aside from this development, however, this week’s data may be leaving the Bank feeling pretty good about its decision to remain on the sidelines. The labour market is still in high gear, and wages are rising, although consumption could still see tepid growth in the months ahead, held down by challenged household balance sheets and sated demand for motor vehicles (see our recent report). Even with the Bank of Canada on hold, Canadians are seeing lower global interest rates filter through to domestic credit markets, supporting the housing market recovery. If data continues to evolve in this fashion, the Bank of Canada may find it cozy to remain on the sidelines.

U.S: Upcoming Key Economic Releases

U.S. Retail Sales – September

Release Date: October 16, 2019

Previous: 0.4%, ex auto: 0.0%, control group: 0.3%

TD Forecast: 0.4%, ex auto: 0.3%, control group: 0.4%

Consensus: 0.3%, ex auto: 0.2%, control group: 0.3%

We expect another firm 0.4% increase in retail sales for September on the back of an also solid gain in sales for the key control group (+0.4% m/m), as consumer fundamentals remain sound (a still-healthy labor market, solid real wages and firm confidence levels). A steady rise in core sales coupled with another solid gain in auto purchases should more than offset a decline in sales at gasoline stations, which reflects a new drop in gasoline prices in September.

Canada: Upcoming Key Economic Releases

Canadian Consumer Price Index -September

Release Date: October 16, 2019

Previous: 0.1% m/m, 1.9% y/y

TD Forecast: -0.3% m/m, 2.0% y/y, Index: 136.4

Consensus: -0.3% m/m, 2.0% y/y, Index: 136.4

TD looks for headline CPI to decline by 0.3% m/m in September, which would push inflation back to 2.0% y/y from 1.9% in August. This improvement is driven by base effects after last September saw a sharp (17%) pullback in airfares that shaved 0.3pp from the index and contributed to a 0.4% decline on the month. In that regard, 2019 is evolving in a similar fashion; airfares have risen by a cumulative 17% since July, and seasonal factors tend to be most punitive in September, with prices falling in 9 of the last 10 years. While this puts us at risk of a similar pullback, the continued grounding of Boeing aircraft should limit the move. Looking beyond airfares, gasoline and prices will also exert a headwind to the monthly print owing to further weakness in the price at the pump and agricultural goods. This should translate into a more modest decline in the ex. food & energy index while the Bank’s preferred measures should hold at 2.0% on average, reflecting muted base-effects for CPI trim and median.

Canadian Manufacturing Sales -August

Release Date: October 17, 2019

Previous: -1.3%

TD Forecast: 1.0%

Consensus: NA

Manufacturing sales are poised to rebound with a 1.0% advance in August. This follows a 1.3% contraction the previous month, which reflected a sharp drop in primary metals alongside auto production shutdowns. The latter extended into early August, which will limit the recovery in motor vehicle shipments, although we expect a more substantial rebound in metals which have seen volatile swings since the US lifted steel/aluminum tariffs in May. Primary metals shaved 0.6pp from last month’s report, and their rebound along with a broad pickup in US activity are the main drivers behind our upbeat forecast. However, we will see a slight drag from lower petroleum prices while stronger homebuilding activity south of the border should have limited impact on demand for forestry products. This is due to a structural decline in Canadian sawmills over the last year, with shipments of wood products down 24% y/y through July. Real manufacturing sales should post a smaller increase owing to higher factory prices.