{kind=link}

Markets defensive as US-China trade looms

With China reluctant to agree to a broader trade deal instead looking to narrow the scope as suggested by weekend headlines, the direction of US-China trade talks set to resume on Thursday remains highly challenging for participants ahead and has arguably led to some defensive positioning across the board. Markets fell away late in the NY session to a wider risk-off move that saw a broad USD bid within FX G10 and EM pairs, bond yields edge higher and S&P 500 Futures slide to 2,936 from an intra-day high of 2,960. USDJPY popped to as high as 107.4 but is now back down to 107.2. USDCNH trades at 7.1338 and looks to test 7.136 intra-day resistance.

Chinese Vice-Premier Liu He remains adamant that reforms to state subsidies and industrial policy won’t be included in any agreement at the upcoming resumption of US-Sino talks. State subsidies and industrial policy reform have been major sticking points in the past to delivering meaningful progress with Trump and The Administration, who are looking to push through a more complete deal. Despite Kudlow taking retaliation tail risks in delisting Chinese companies off the table last night, we expect headline sensitivity to remain high, especially in the equities and USDJPY space, as markets look to feed off any positive or negative soundbites that hit the wires.

A deeper analysis of how upcoming talks could play out and potential reactions is captured in our “US-China Playbook, Where To From Here?” piece posted earlier in the week.

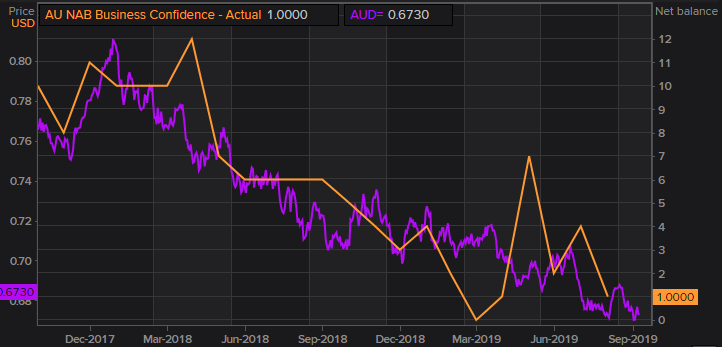

Will RBA rate cuts flow through to survey numbers?

Up ahead, Sep. NAB Business Conditions and Confidence Surveys – above 0 (positive sentiment) and below 0 (negative sentiment) – are due for release at 11.30am AEST. Both disappointed this time last month when they printed at 1. The readings showed a decline on the prior month and maintained the falling trend that had been observed since a peak in the middle of 2018. Markets, this time around, will be looking for some sort of improvement in line with RBA commentary that suggests the Aussie domestic economy has reached “a gentle turning point” having recently “been through a soft patch”. With another month of transmission of the RBA’s dual rate cuts and income tax offsets flowing through to Aussie businesses and consumers – an improvement in sentiment is likely on the cards. In terms of price action, the print is secondary to US-China trade matters though having said that AUDUSD could catch a bid on a positive reading above the prior month.

CNH catches Caixin Services PMI

Elsewhere, Markit’s Sep. China Caixin Services PMI number is out at 12.45pm AEST with the prior month’s reading having come in at 52.1. The Services PMI number follows a cyclical pattern and has never printed outside of 54.5 and 50.6 in the prior three years. Most likely the read will fall on deaf ears.