{kind=link}

Sterling declined as the Brexit crisis continued over the weekend. Yesterday, Boris Johnson suffered another blow after the resignation of Amber Rudd, who was the Secretary of State for Work and Pensions. In a statement, Rudd said that her position on Brexit was made untenable due to lack of progress on a new Brexit deal. There are concerns that other members of the government are considering resigning. Among those who will be watched closely are Julian Smith and Robert Buckland. Meanwhile, the French government warned that it will veto aa further Brexit delay. Later today, investors will receive the second reading of the second-quarter GDP, manufacturing production, industrial production, and the trade data.

The European economy will be in focus later today as Germany releases its trade numbers for the month of July. The German exports for July are expected to have slumped by -0.5% in the month. This will be a worse decline from the previous month’s -0.1%. Imports are expected to decline by -0.3% after increasing by 0.5% in June. As a result, the trade surplus is expected to drop to EUR 17.5 billion after rising to EUR 18.1 billion in June. In recent months, economic data from Germany has been relatively weak. The manufacturing PMI and other economic data show that the economy is contracting.

The price of crude oil rose after Saudi Arabia announced the removal of Khalid al-Falih as Minister of Energy. Khalid was replaced by King Salman’s son, Prince Abdulaziz bin Salman. This announcement broke the longtime tradition of not appointing members of the ruling family to Minister of Energy. This announcement came at a time when Saudi Arabia has struggled to raise oil prices. It also came a week after Falih was replaced as the chair of Saudi Aramco, the world’s most profitable company. Over the weekend, it was announced that JP Morgan will be the main underwriter for the company as it prepares for its IPO. Meanwhile, data from China too added to that pressure. Yesterday, data showed that exports in August declined by 1.0% after rising by 3.3% in the previous month.

The Japanese yen rose slightly against the USD after the country released its second reading of the Q2 GDP data. Numbers showed that the economy expanded at an annualized rate of 1.3%, which was in line with expectations. On a QoQ basis, the economy expanded by 0.3%, which was slightly lower than the previously-released 0.4%. Capital expenditure rose by 0.2%, which was lower than the expected 0.7%, while the external demand declined by -0.3%.

USD/JPY

The USD/JPY pair declined fromFriday’s close of 107.00 to a low of 106.75. On the 30-minute chart, the price is slightly below the 14-day and 28-day moving averages. The RSI has moved slightly lower to the current level of 46 while the momentum indicator has remained at the 100 level. Today, the pair will likely resume the previous upward trend and retest the important resistance level of 107.00.

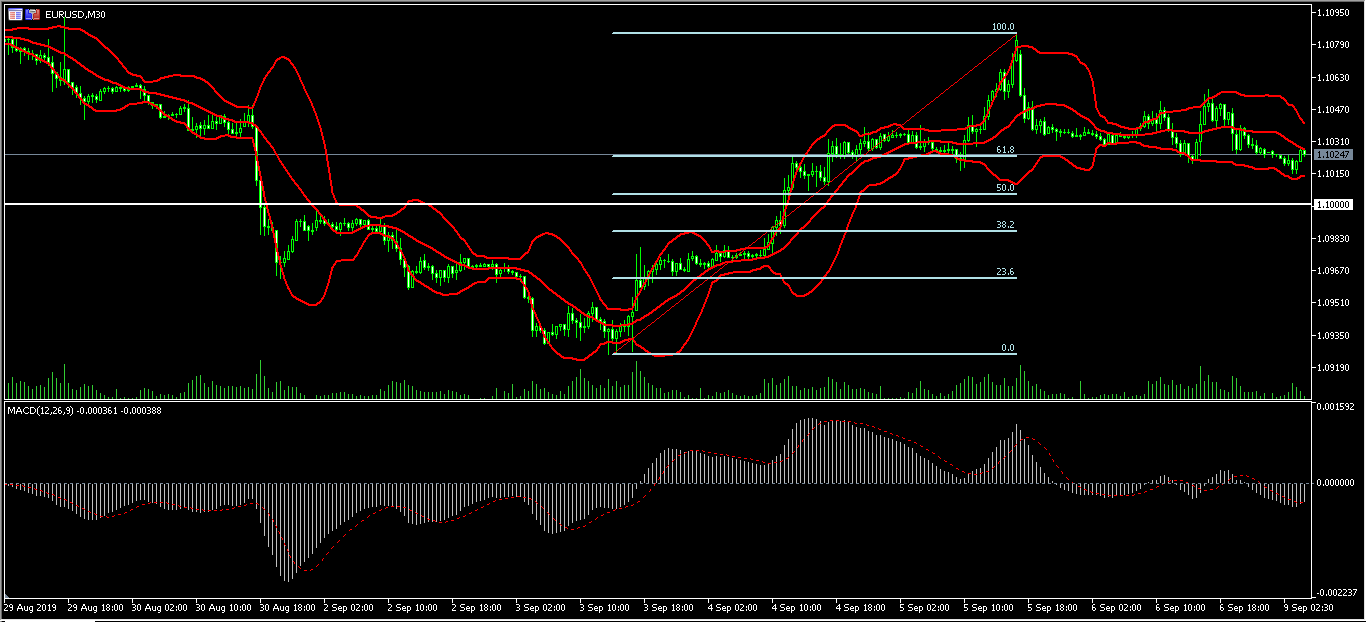

EUR/USD

The EUR/USD pair is trading at 1.1025, which is along the 61.8% Fibonacci Retracement level on the 30-minute chart below. This price is along the middle line of the Bollinger Bands while the signal line of the MACD is at the lower side. Today, the pair will likely move lower to test the important psychological level of 1.1000, which is also along the 50% Fibonacci level.

AUD/USD

The AUD/USD pair rose even after China released weak exports and imports data yesterday. The pair moved from a low of 0.6836 to a high of 0.6850. On the 30-minute chart below, this gain was a continuation of a strong trend that started last week when the pair was trading at 0.6685. The current price is slightly above the 14-day and 28-day moving averages while the RSI has been on an upward trend. The commodities channel index too has been on an upward trend. The pair will likely continue moving higher to retest the previous high of 0.6860.