{kind=link}

It will be the turn of the Reserve Bank of Australia and the Reserve Bank of New Zealand to next announce their latest policy decisions following a busy week for central banks. New Zealand will also see the release of the quarterly employment report and jobs figures are due out of Canada too. The highlight for the United Kingdom and Japan will be GDP growth numbers for the second quarter, and in China, the monthly trade and inflation releases will be watched for more clues on the health of the world’s biggest exporting nation. As for the Eurozone and the US, it will be a relatively quiet week.

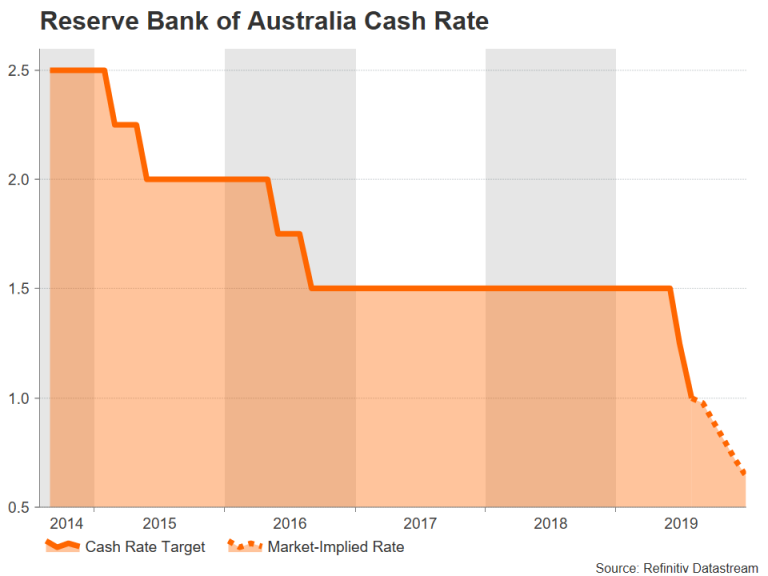

RBA to hold rates in August

The Reserve Bank of Australia meets next week to set monetary policy and will make its announcement on Tuesday. After cutting rates by 0.25% in each of the past two meetings, the RBA is expected to stay on hold in August as it monitors how the two cuts are supporting the economy as well as what kind of a boost the recently announced tax cuts are having. But with markets anticipating one more cut before the year end, it will be important to see whether the RBA will commit itself to further cuts and that could depend on what the bank’s latest economic projections will show when the Monetary Policy Statement is published on Friday.

The Australian dollar is struggling to find a floor in its downswing against the US dollar even after this week’s better-than-expected numbers on inflation, manufacturing and retail sales. There may not be much support for the aussie either from next week’s data on June trade (Tuesday) and housing finance (Friday).

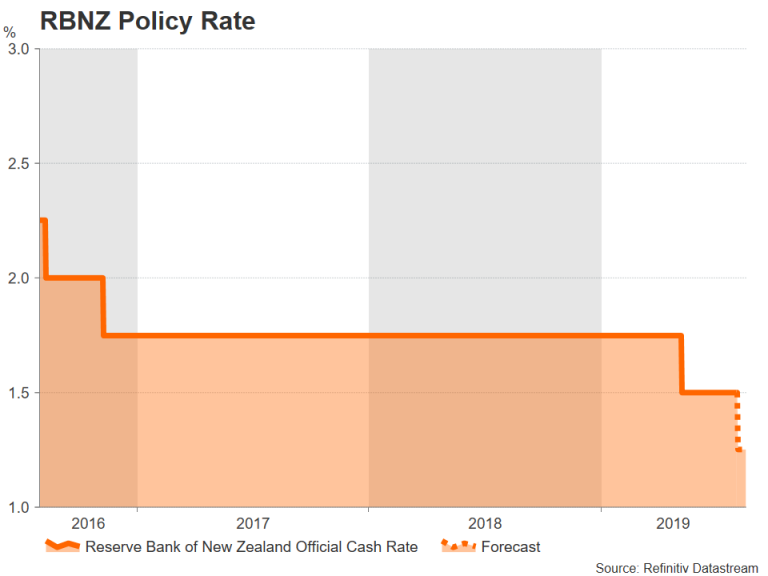

RBNZ expected to deliver second cut

Unlike its Aussie counterpart, the Reserve Bank of New Zealand will not be standing pat in August and is widely expected to slash its cash rate for the second time since May. But similar to the RBA, the focus will be on how many more rate reductions the central bank will signal in its announcement statement and quarterly Monetary Policy Statement.

Business confidence fell to the lowest in a year in July according to a closely watched survey by ANZ Bank, fuelling expectations that the RBNZ will move to provide more stimulus to a slowing economy. Investors will also get the chance to gauge the country’s labour market a day before the RBNZ decision. If Tuesday’s employment report for the second quarter fails to impress, traders will likely raise their bets of further easing by the RBNZ in the coming months. This would be negative for the New Zealand dollar, which has slumped to six-week lows on the back of rising trade tensions and a firmer US dollar.

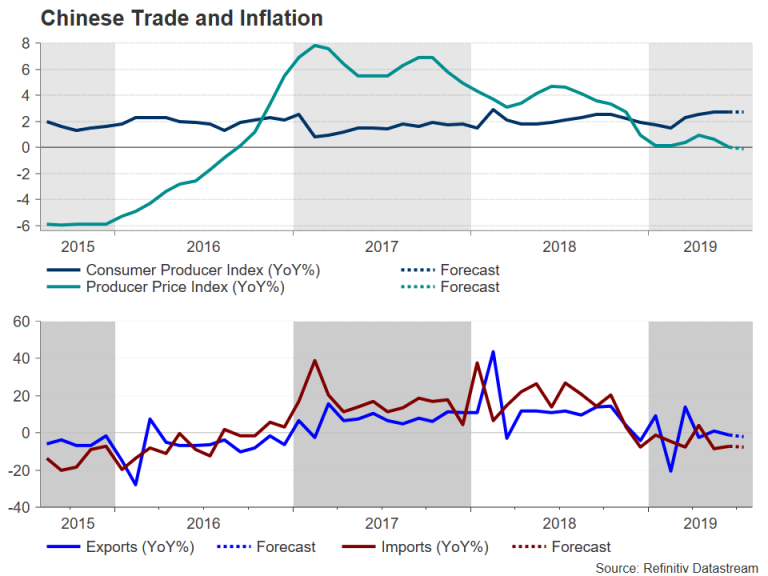

China trade data to underline Trump strain on economy

Trade numbers out of China will attract attention on Thursday amid a fresh escalation in the long-running trade conflict with the US after President Trump this week decided to slap 10% tariffs on the remaining $300 billion worth of Chinese imports, breaking the truce agreed at the G20 summit. Exports from China are forecast to have fallen on an annual basis for a second straight month in July, by 2.2%, worsening from the prior 1.3% drop. Imports are also expected to have decreased at a sharper rate, by 7.6%.

Inflation indicators will follow on Friday, with producer prices anticipated to have declined by 0.1% year-on-year in June and for the consumer price index to have risen by 2.7% y/y, unchanged from the prior month’s rate.

If confirmed, the data would reinforce concerns about the sustained damage to Chinese manufacturers from Trump’s trade war as well as about the slowing domestic demand picture, which has repercussions for nations that are major exporters to China.

Japanese Q2 GDP growth eyed

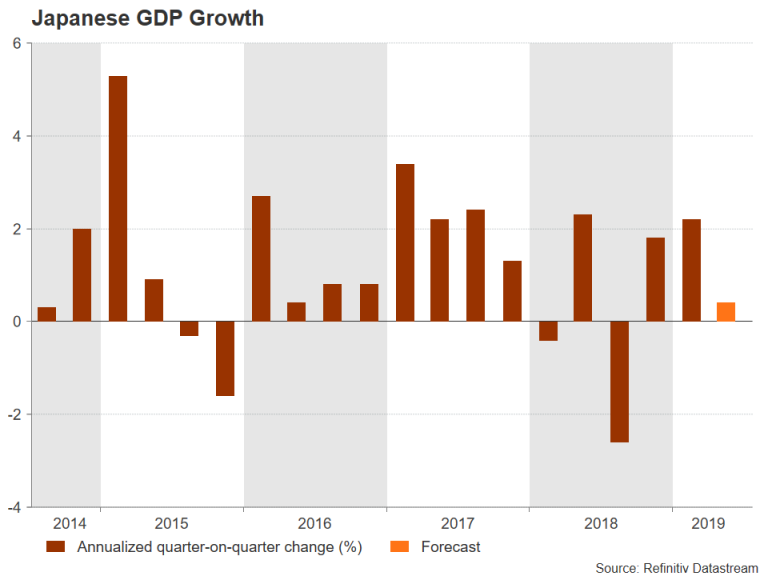

Improving household consumption in Japan has so far been able to support growth as exports have taken a big knock from the global trade frictions and the ensuing slowdown. Household spending numbers for June will therefore be watched closely on Tuesday as any deterioration on that front would be a major warning sign for the Bank of Japan. Wage figures will also be released on Tuesday and further weakness in both nominal and real earnings growth could signal that the positive growth in consumption may not be sustainable.

The Bank of Japan’s Summary of Opinions of its July policy meeting will be published on Wednesday and could reveal whether policymakers came close to approving additional stimulus measures. The bank left monetary policy unchanged this week but indicated it was ready to act if price momentum towards its 2% inflation target is lost.

The focal point, however, will be on Friday’s GDP estimate for the second quarter. Growth in Japan is forecast to have slowed from an annualized 2.2% rate in Q1 to 0.4% in the second quarter. A disappointing GDP print, combined with a Summary that suggests BoJ board members see a stronger case for an immediate policy action than what is currently perceived by the markets, could alleviate some of the intense safe-haven demand the yen is facing again following the latest spike in trade tensions.

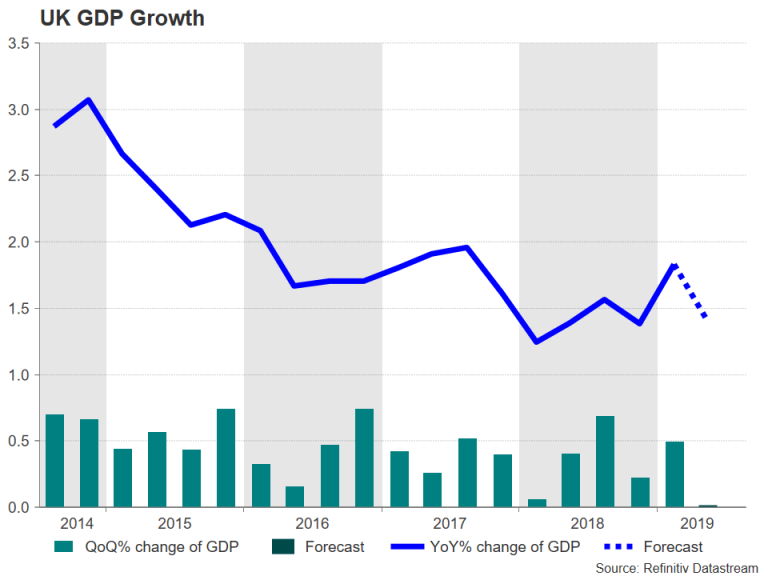

UK growth to slow in Q2

As the pound’s freefall continues, a barrage of data due out of the UK next week could halt or deepen the currency’s downtrend. The focus at the start of the week will be on the Markit/CIPS services PMI. The July reading is out on Monday and investors will be hoping to see signs of stronger growth in the UK’s largest economic sector after several months of a patchy performance.

The bulk of the data, though, will be released on Friday, which will include trade, industrial and manufacturing output figures, as well as both monthly and quarterly GDP estimates. Growth in the British economy is forecast to have ground to a halt in the three months to June, slowing from the prior 0.5% rate. There’s a greater risk, however, of the data missing the forecasts than beating them given the heightened Brexit and political uncertainty during the period so a small contraction in Q2 wouldn’t be totally surprising.

But even in the unlikely event that next week’s releases were to allay concerns of a downturn, any boost to the pound would probably be short-lived, having just crashed below the $1.21 level. Unless either the UK or the EU budge on their preconditions to hold fresh Brexit talks, there’s little that can presently help the battered pound.

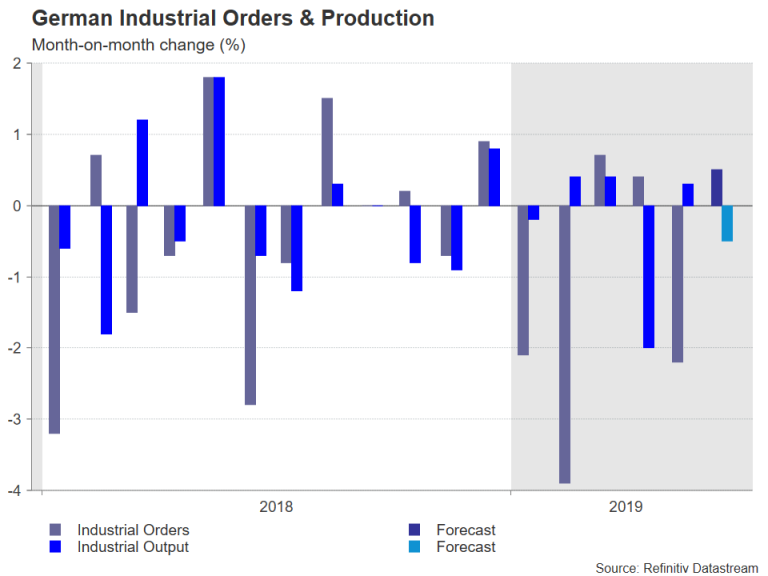

German industrial data unlikely to be euro’s saviour

Across the channel, it’s going to be a fairly muted week, with only German industrial numbers having the potential to be market moving. German industrial orders for June are due on Tuesday and will be followed by industrial production figures for the same month on Wednesday, while on Friday, analysts will be watching whether May’s 1.1% bounce in exports continued in June.

An encouraging set of stats from Germany might help stabilize the beleaguered euro, which lost more than 2% of its value against the dollar in July.

Canadian jobs and US ISM non-manufacturing PMI to be North American highlights

The US calendar will also be somewhat short of excitement in the next seven days, with the main risk for the dollar likely to be Monday’s non-manufacturing PMI. Aside from the all-important ISM survey, the greenback may also see some reaction to Tuesday’s JOLTS job openings for June and Friday’s producer prices for July.

North of the border, however, it will be a bigger week for the loonie as Canada publishes the July employment report. Recent data out of Canada continues to be mostly positive, enabling the Canadian dollar to put up a strong defence against the US currency’s comeback. But the last jobs report was unexpectedly poor, and traders will be looking for a rebound in jobs growth in July to maintain their bullish bets against the loonie.