{kind=link}

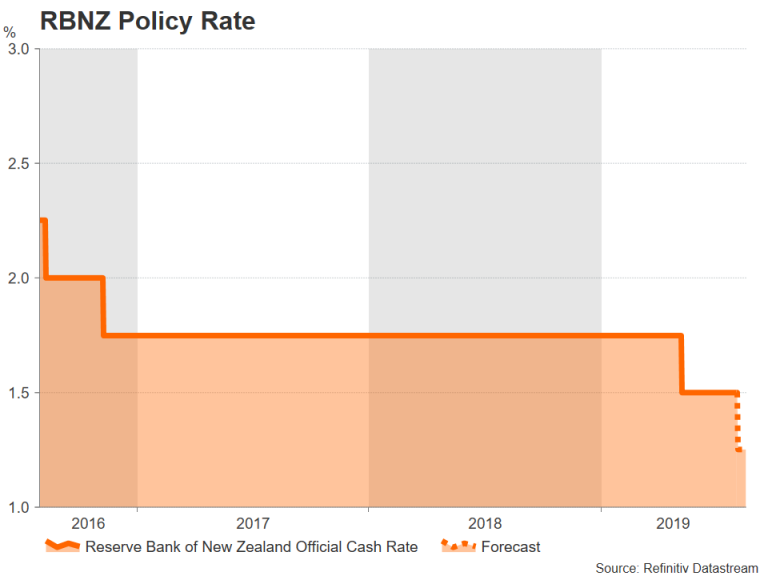

The Reserve Bank of New Zealand was the first of the major central banks to embark on an easing cycle when it lowered rates in May. It’s been on hold since then but that could be about to change next Wednesday (0200 GMT) as the RBZN is expected to deliver a second rate cut. Ahead of the policy meeting, however, quarterly employment numbers will be watched on Tuesday (Monday, 2245 GMT).

Low business confidence a big concern

New Zealand’s economy grew by a solid 0.6% quarter-on-quarter rate in the first three months of the year. However, business confidence remains low, even after the May rate cut, and sentiment in the construction sector, which drove growth in Q1, appears to be plunging again. The closely watched NZ Business Outlook index by ANZ Bank fell to -44.3% in July – the lowest in a year – led by a sharp drop in construction intentions.

Jobless rate to remain steady

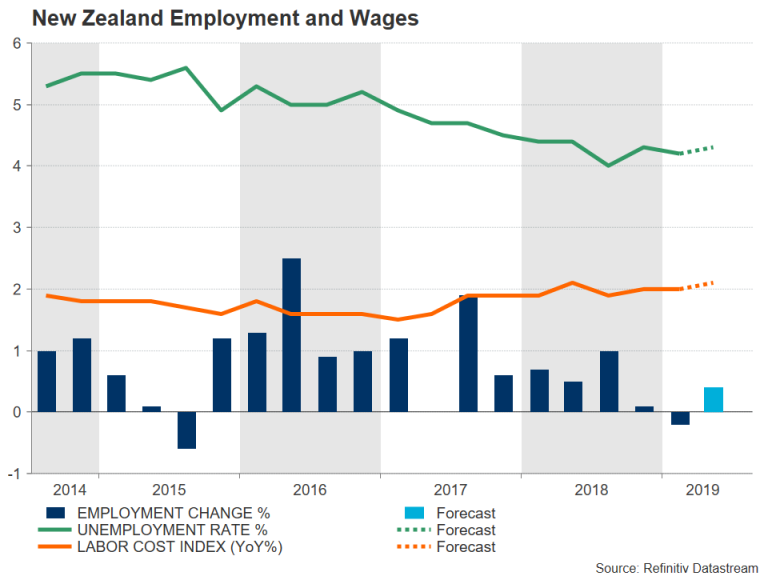

The continued weakness in business confidence does not bode well for future growth and investors will be monitoring Tuesday’s employment report for more clues on where the economy is headed. New Zealand’s unemployment rate fell slightly to 4.2% in the first quarter and is forecast to have edged up to 4.3% in Q2. Jobs growth is expected to have rebounded by 0.4% over the quarter, while the labour cost index is projected to have increased slightly to 2.1% year-on-year from 2.0% in Q1.

However, this is unlikely to be inflationary enough to significantly push up the consumer price index, which stood at 1.7% y/y in Q2. The RBNZ has a target band of 1-3% and would prefer to have the CPI index running closer to the middle of its target. Since April 2019, the RBNZ has also been mandated to supporting maximum sustainable employment, so even if inflation was to pick up, policymakers will in addition want to see a tightening of the labour market before considering reversing course with their current policy direction.

RBNZ to cut for second time this year

The RBNZ is widely expected to cut its overnight cash rate by 0.25% to a new record low of 1.25% on Wednesday amid a worsening of the global economic outlook and displeasure in the business community about the new government’s economic policies. The spike in US-China trade tension this week only serves as a reminder that the trade war is here to stay. The RBNZ is therefore expected to maintain that downside risks to the economy have increased and signal that further rate reductions might be needed in the future.

Rate cut already fully priced in

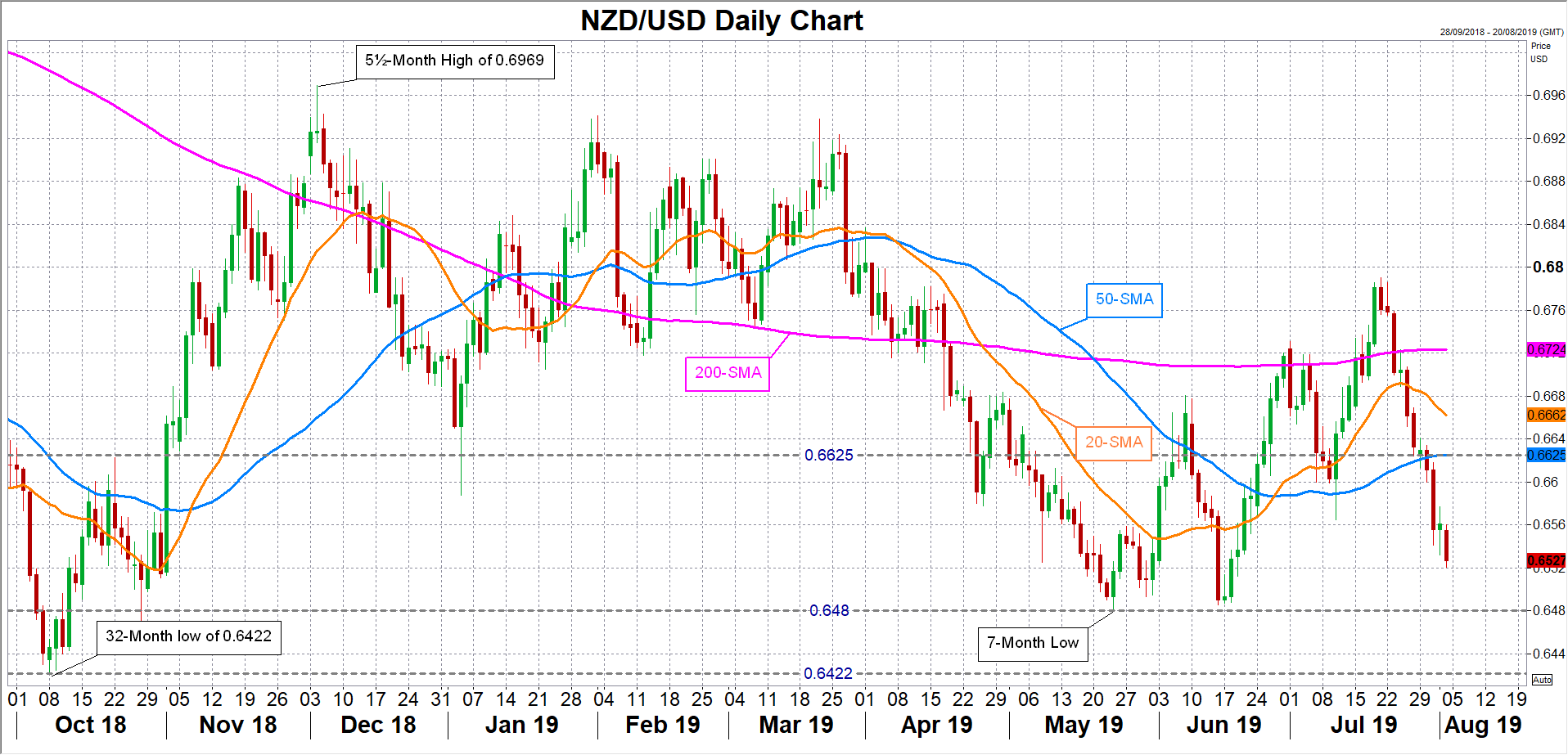

Investors have fully priced in a rate cut on Wednesday so there may not be much reaction in the currency markets to the RBNZ decision if the Bank’s statement is more or less in line with analysts’ expectations. The New Zealand dollar has slid to six-week lows as investors have become more confident that the RBNZ will need to slash rates by possibly another 50 basis points after the August meeting.

If the RBNZ provides a clear signal of more easing, the kiwi could extend its decline towards the 7-month low of $0.6480 brushed in May. Breaching this support would clear the way for the October 2018 low of $0.6422. If, though, the RBNZ appears hesitant about the need for further policy easing, the kiwi might manage a rebound towards the 50-day moving average around $0.6625.