{kind=link}

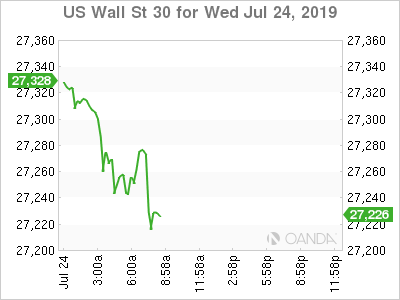

Today could be the day the bears take control. After what was a very hot start to earnings season, investors got a cold bucket of ice poured over themselves as the DOJ opened a probe on techs biggest stars and industrial earnings from Boeing and Caterpillar disappointed immensely. The US stock market is still the best game in town and while a pullback could occur, traders will return as the prospects of the Fed’s easing cycle will provide longer term support for risky assets.

Boeing saw sales collapse 35% and the 737 Max crisis appears, which is now in its fifth month appears to be going nowhere anytime soon. While shares initially tanked, investors bought the dip as many analysts did not include the $5.6 billion accounting charge in their estimates.

Caterpillar is starting to show signs of weakness and after a couple quarters of raising guidance, they adjusted their earnings growth to the lower end of their forecast. A slowdown in the Permian Basin is also starting to effect Caterpillar and that could be a sign we could see the velocity of US crude production slow down.

The Dow fell 0.4% following the poor industrial earnings reports.

The US Justice Department sent their eyes on big tech and this will be a story that may weigh on Facebook, Apple, Amazon and Alphabet throughout earnings season. Are the tech giants too big for government to kill? They might not get killed but they will need to spend time and money on an onslaught of investigations and be vulnerable if government makes an example of one them.

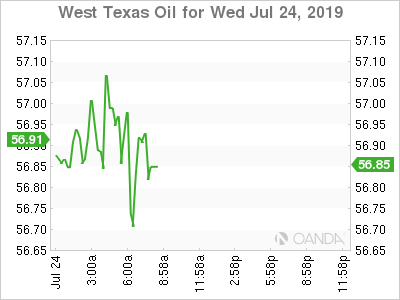

Oil

Energy traders are scratching their head to as why oil is not higher, after the API report showed a massive 11 million barrel draw, Iran maintained their hard stance that they will not negotiate with the Trump administration, the dollar is softer and trade optimism should help ease some global demand concerns. It appears oil markets are getting fatigue from the falling US stockpile story. If today’s EIA report confirms another draw, that will mark the six straight weeks of falling stockpiles. The demand story is still weighing on crude and today’s terrible PMI data from Europe is probably keeping the energy rally under control.

Demand will likely get some solid footing on promises of stimulus from the ECB this week and the Fed’s commitment to an easing cycle at the end of the month.

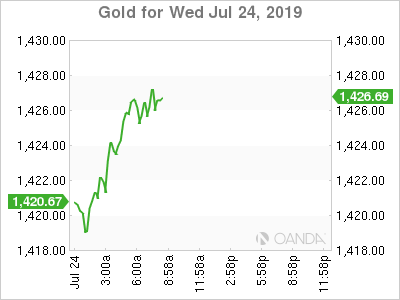

Gold

Gold continues to wait for the FOMC event. A rate cut is priced in, but the Fed’s commitment to doing whatever it can to prevent deflation will allow them to signal more cuts and that will benefit the yellow metal tremendously.