{kind=link}

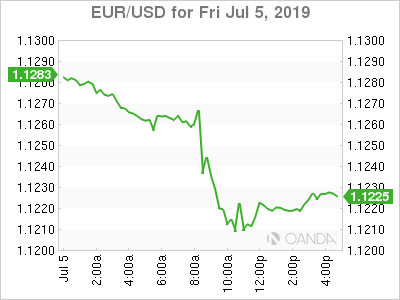

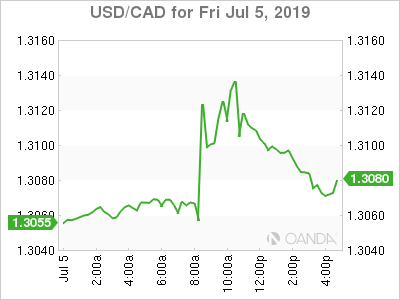

How big will the punch bowl be this time around? Financial markets are convinced the Fed is set to commence on an easing cycle this summer, but if we see Fed Fund futures price in only two rate cuts this year, US stocks will struggle to make fresh highs and the highly anticipated dollar reversal may not come to fruition. Friday’s blockbuster US non-farm payroll report tentatively derailed stock and equity bullish plans. The needle was moved from a slight lean towards 3 rate cuts to two cuts. The dollar’s broad gains accompanied a surge with US Treasury yields and a pullback in stocks.

The focus will now shift to incremental updates on the trade front and a plethora of Fed speak and the Minutes to last month’s decision. US inflation data will be released but other indications do not point for a significant surprise rise. The release of China’s trade figures will show how resilient their economy was during the tensest moments in the trade war. With the PBOC waiting to stimulate their economy, we could see dismal data support earlier action. Regarding trade, we will need to see meaningful updates or scheduled trips to DC or Beijing to support optimism that both sides are closing the gap. A wrath of Fed speak will see investors search for clues if the Fed waiver on its signal for a July rate cut.

- Powell testifies on Semiannual Monetary Policy Report

- Trade War impact on Chinese Trade and Inflation data

- German Industrial Production could fuel contraction bets

Euro

Stimulus bets from the ECB may grow if we continue to see a trend of softer than expected data out of Germany. The brewing trade war between the US and Europe will likely to continue to weigh on car manufacturers, with Germany bearing the brunt of the troubles. Industrial production on a monthly basis is expected to rebound, but following a very disappointing factory orders reading, we should not be surprised if the German data comes in softer.

If we see Lagarde become the ECB Chief, we could see fiscal stimulus expectations rise, which should be very positive for both growth and the euro. Draghi’s ECB has stated they are in no rush to deliver a rate cut this month, but if the data continues to show significant slowdowns, a 20 basis-point cut could happen this month.

CAD

The Bank of Canada (BOC) is widely expected to keep rates steady, with only one economist calling for a 25-basis point cut. Monetary policy is expected to remain on hold for the rest of the year, as the recent data has been surprisingly better than expected, not counting Friday’s cool labor market number. Employment has been on a tear, with the first half being the best start since 2002.

Oil

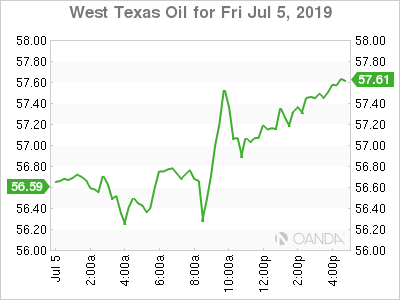

The crude selloff that stemmed from global slowdown concerns appears to be fully priced in. West Texas Intermediate crude may find key support from the mid-$50-barrel area. Oil got a boost on an improving outlook for demand on a surprising robust US nonfarm payroll report. Fresh stimulus bets are still strong for the Fed to deliver a rate cut at the end of July and for the other big three banks, the PBOC, ECB and BOJ, to remain active in delivering additional stimulus.

If we do see US and China come through with scheduling face-to-face talks, we could see markets again to price in further optimism we could see a deal done this year. Global demand would get a reprieve if China and US could finalize a trade deal.

Geopolitical risks are also keeping a bid in place for oil as Iran continues to increase their nuclear activities. Up until now, most of Europe has been trying to negotiate with Tehran, but if Iran continues to with their nuclear agenda, we could see deeper international sanctions that could completely cripple Iran’s economy.

Gold

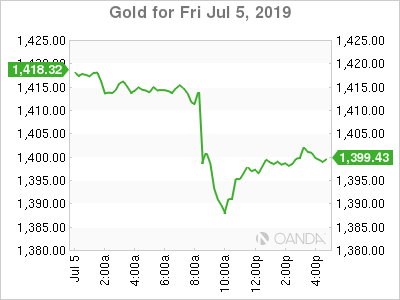

Gold lost some of its mojo after a robust nonfarm payroll report eased up dovish bets on the Fed. The overall outlook for bullion is still looking bright as gold ETF inflows appears insuppressible. Robust demand for the yellow metal will continue to be supported on the backdrop of expectations of fresh stimulus to be released by the four largest central banks.

Bitcoin

The cryptocurrency markets have been on a mission to deliver wide range interest that will attract retail, institutional and mainstream commerce interest over the past several weeks. With social media giant Facebook entering the digital coin space, all coins have benefited on renewed interest. Bitcoin remains the bellwether that has yet to be threatened by other altcoins and we should not be surprised if it eventually makes a complete recovery of the $16,000 plummet that started at the end of 2017.

Monday, July 8th

- CNY Trade Balance

- 2:00am ET EUR Germany Industrial Production m/m

- 2:00am ET EUR Germany Trade Balance

- 4:30am ET EUR Sentix Investor Confidence

- 9:30pm ET AUD NAB Business Confidence

Tuesday, July 9th

- 6:00am ET USD NFIB Small Business Optimism

- 7:00am ET MXN CPI m/m

- 8:15am ET CAD Housing Starts

- 7:50pm ET JPY PPI y/y

- 9:30pm ET CNY CPI and PPI data

Wednesday, July 10th

- 2:00am ET NOK Norway CPI m/m

- 2:45am ET EUR France Industrial Production m/m

- 4:30am ET GBP GDP m/m

- 4:30am ET GBP Industrial and Manufacturing Production data

- 10:00am ET CAD BOC Interest Rate Decision

- 10:30am ET DOE US Crude Oil Inventories

- 7:50pm ET JPY Core Machine Orders m/m

Thursday, July 11 th

- 2:00am ET EUR Germany CPI y/y

- 2:45am ET EUR France CPI m/m

- 3:00am ET CZK CPI m/m

- 3:30am ET SEK CPI m/m

- 8:30am ET USD CPI m/m

- 8:30am ET USD Initial Jobless Claims

- 6:30pm ET NZD Manufacturing PMI

Friday, July 12th

- 12:30am ET JPY Revised Industrial Production m/m

- 3:00am ET TRY Turkey Industrial Production m/m

- 5:00am ET EUR Industrial Production m/m

- 8:30am ET USD PPI m/m