{kind=link}

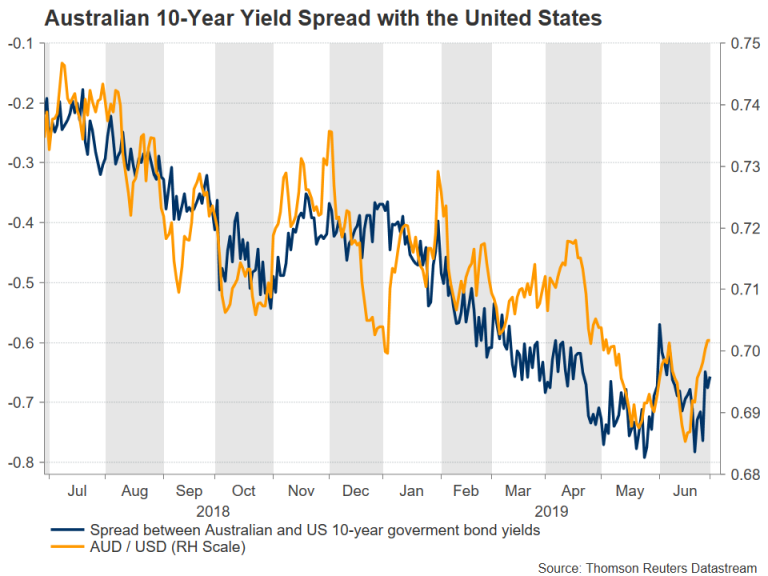

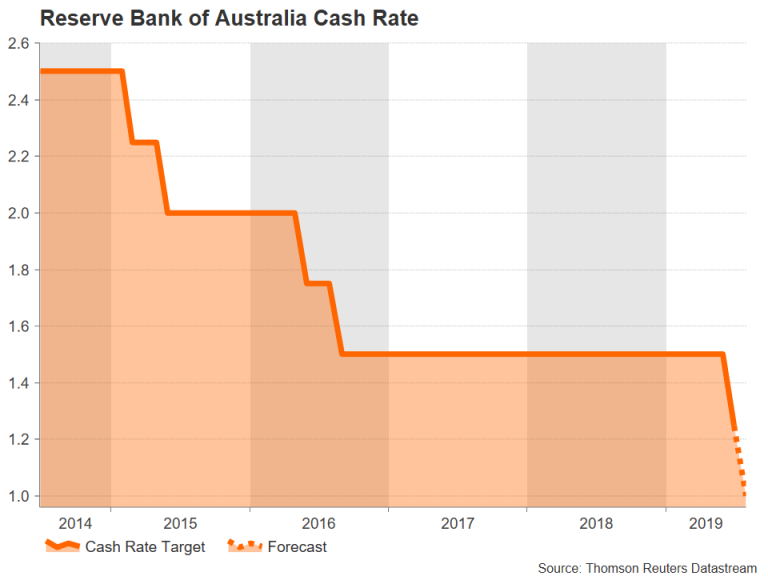

The Reserve Bank of Australia is widely anticipated to lower its cash rate for the second straight meeting when it announces its next policy decision at 0430 GMT on Tuesday. After cutting rates for the first time in nearly three years in June, the RBA is expected to ease policy again amid a cooling global economy and increased uncertainties stemming from trade and geopolitical tensions. But despite strong signals from policymakers that more rate cuts are likely, the Australian dollar has been on the up on narrowing yield differentials between Australian and US yields.

Lowe says another rate cut “not unrealistic”

RBA Governor, Philip Lowe, couldn’t be clearer in flagging another rate cut when he said “it is not unrealistic to expect a further reduction in the cash rate” in a speech on June 20. Lowe has become increasingly concerned about the slowdown in GDP and jobs growth, pointing to the spare capacity in the economy, especially in the labour market.

The RBA had been relying on the tightening labour market to spur wage growth, which in turn would lift inflation. But the annual CPI rate fell to 1.3% in the first quarter, well below the Bank’s 2-3% target band and Australia’s jobless rate has been ticking higher in recent months, meaning wage growth isn’t likely to accelerate anytime soon to provide the much-needed boost to consumer prices.

Market expectations for July rate cut running high

Market expectations of a rate cut at the July meeting soared after Lowe’s comments and investors have priced in about an 81% probability that the RBA will lower the cash rate to a new record low of 1.00% from 1.25%. Those odds may seem a little high given that the United States and China – Australia’s biggest trading partner – just agreed to resume trade talks and delay any additional tariffs for the time being.

However, with no deadline set for a trade deal, an agreement could be months away and disappointing manufacturing PMI data out of China today reinforced the view that the year-long trade dispute has already started to hurt the country’s growth prospects. So unless the global growth outlook was to shift to a significantly more positive one, the Bank will struggle to meet its objectives of price stability and full employment.

Aussie turns bullish as greenback loses shine

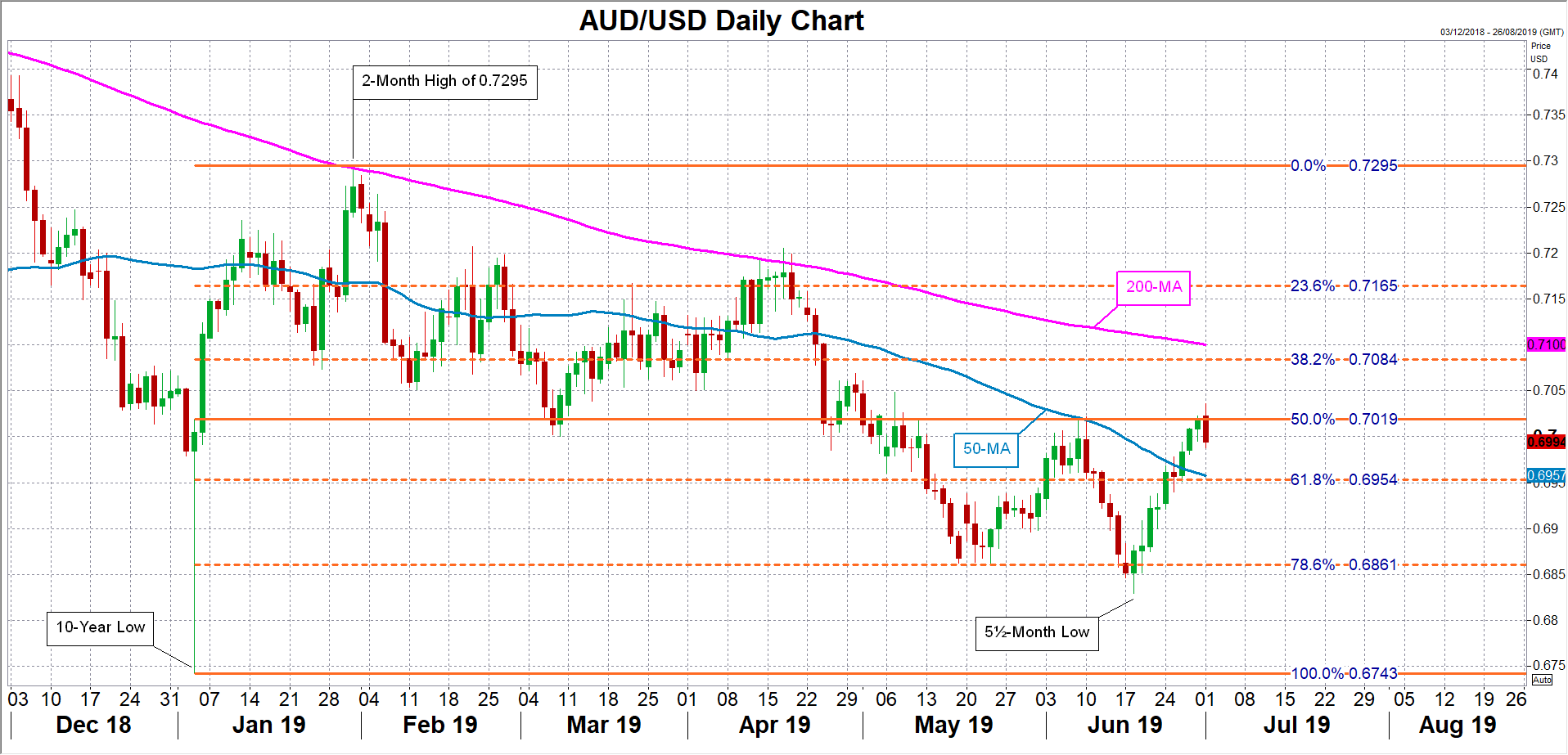

But the gloomy outlook and dovish stance by the RBA haven’t been enough to place the aussie firmly on a downpath. The aussie had slid to a 5½-month low of $0.6829 in the days after the RBA’s June cut but following the US Federal Reserve’s dovish turn at its meeting on June 18-19, the Australian currency has been unable to overcome the bearish bets made against the US dollar.

Expectations that the Fed will cut rates more than the RBA lifted the aussie to a near 2-month high of $0.7036 earlier today. But while a bearish dollar means the aussie may not find much downside unless the Fed was to become less dovish, further positive momentum is likely to be limited.

Risk of RBA delaying rate cut until August

Immediate resistance for additional gains could come at the 38.2% Fibonacci retracement of the upleg from $0.6743 to $0.7295, which falls around $0.7084. A break above this level is possible if the Bank surprises with no rate reduction in July. Such an outcome shouldn’t be discounted as the RBA may decide to wait for its updated economic projections, to be published in its August Monetary Policy Statement, before making another cut. The $0.71 handle, near the 200-day moving average could be a target if the RBA signals it’s not in as much hurry to lower rates as investors have perceived

However, if the Bank proceeds with a 25-basis point rate cut on Tuesday and indicates further easing in the coming months, the aussie is likely to come under some short-term selling pressure and ease towards the 61.8% Fibonacci at $0.6954, just below the 50-day moving average.