{kind=link}

Global stock markets were flat in anticipation of what the sidebar meeting between President Trump and Xi at the G20 meeting would bring. After the 80-minute meeting, Trump said that negotiations are “back on track”.

The baseline scenario leading up to the G20 sit-down of the two leaders was just the restart of trade talks. Without a big announcement or details on how closer or far they are to reach a deal, there is a high probability that the outcome will be similar to the previous G20 meeting where another truce was announced.

Fears of tariff escalation will ease, but current tariffs could remain unless real progress in made from both sides.

In their meeting in Osaka, everybody played their part without any additional drama and until more details emerge, we are back at square one. The road ahead looks complicated as China demands more equal treatment, and the US is pushing through on intellectual property protection.

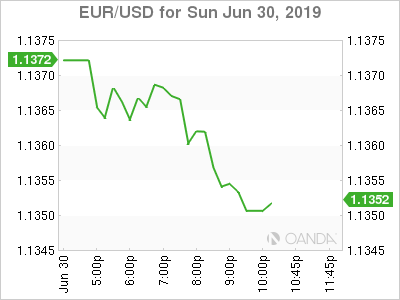

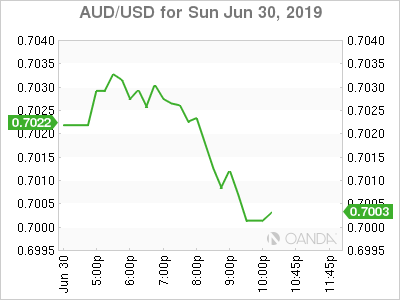

The US dollar is mixed against major pairs at the end of trading on Friday. Commodity currencies lead the charge with the New Zealand dollar almost 2 percent up on the greenback. The Canadian dollar rose 1 percent as strong economic indicators play down the probability of an interest rate cut. The Fed clipped the dollar’s wings by signalling an upcoming benchmark rate cut.

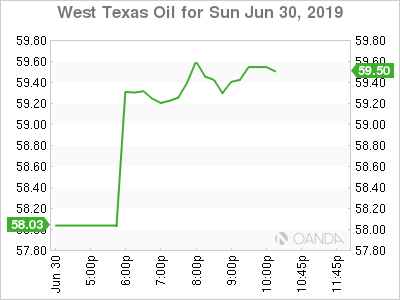

Oil is positioned to rise after trade cease fire between China and the US. The OPEC+ had a more productive G20 summit with Russian President Putin announcing an extension to the production cut agreement that will be finalized later this week when the group meets in Vienna.

Markets will look forward to an action packed first week of July. The Organization of the Petroleum Exporting Countries (OPEC) will meet with major producers to finalize the extension discussed by Putin at the G20.

Manufacturing data in China and the US will not show any impact from the G20 meeting, but the indicator could change drastically going forward. Chinese factory activity was lower than expected at 49.4 and remains in contraction, with the newly announced truce between China and the US will have to deliver an agreement or else global manufacturing will continue to deliver soft data points.

The Reserve Bank of Australia (RBA) could slash its rate to 1 percent as the central bank is part of the dovish choir of monetary policy makers that are back to their easing ways.

The week wraps up with the release of the U.S. non-farm payrolls (NFP) on Friday. US jobs are expected to bounce back after the disappointing March report that showed only a gain of 75,000. A range from 150,000 to 210,000 is forecasted with a bump in average hourly earning up to 0.3 percent.

OIL – Russia and Saudi Arabia Make Progress at G20

Oil finished the week mixed with West Texas Intermediate rising 1 percent but Brent losing 1.53 percent. Trade uncertainty ahead of get G20 added volatility to energy pricing. It was the main reason the OPEC and the other major producers pushed back their ministerial meeting to this week. Russia remains on the sidelines and seems only a big drop in oil prices would expedite an extension of the agreement to cut production to stabilize prices.

Crude prices have been pressured downward as the trade war between US-China was a negative factor on energy demand. Supply disruptions added support to prices, but the major factor was the OPEC+ which is why if Russia does not agree to an extension the initiate could be too much for Saudi Arabia to handle by itself.

Despite Trump and Xi getting back to the negotiation table on trade, Russia decided to go ahead with a production cut extension that could last 9 months.

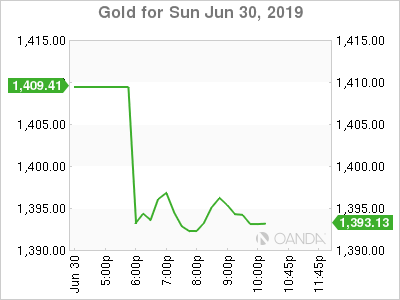

GOLD – Gold Under Pressure from Positive Trump-Xi comments on Trade at G20

The most anticipated meeting at the G20 left market participant wanting more. The sit-down between Trump and Xi yielded a new round of talks with no clear date. The OPEC+ on the other hand was more productive and pretty much announced that the production deal will be extended. The group had delayed their ministerial meeting and after the US-China ceasefire they decided to go ahead with continuing to limit production output by up to 9 months.

Gold rose 0.97 percent on Friday as the yellow metal is back on top as the favourite destination for investors seeking refuge from uncertainty. The willingness to cut rates from the Fed is keeping the dollar weak and gives the gold the upper hand as July gets underway. The market is pricing in a rate cut to be announced at the July Federal Open Market Committee (FOMC) that will put more downward pressure on the dollar.

Middle East tensions and the ongoing Brexit debate will be in the spotlight in July making a strong case for gold climbing higher as major central banks run back their easing monetary policy playbook.

Gold will be pressured as trade optimism reduces the appeal of the yellow metal as a safe haven, although given the macro headwinds it remains part of various diversification strategies. The lack of details on what has really changed from the US-China negotiations makes it hard to believe the new talks will have a different outcome, which is a positive for gold.

The next biggest obstacle for gold will be US economic indicators, if there is a significant rebound the Fed could hold the benchmark rate at its July meeting. The market has walked back the number and depth of the rate cuts after some less dovish comments from Fed members. If there are massive job and inflation gains in the NFP report, gold could fall as the rate cut narrative gets weaker.