{kind=link}

It’s another action-packed week, with the pivotal G20 summit that will decide how risk sentiment develops, finally upon us. Elsewhere, the Reserve Bank of Australia (RBA) is expected to slash rates again, while oil traders will pay close attention to the OPEC meeting. Economic data are not in short supply either, with the US employment report likely to add the final touches to expectations around how deep the Fed will cut in July.

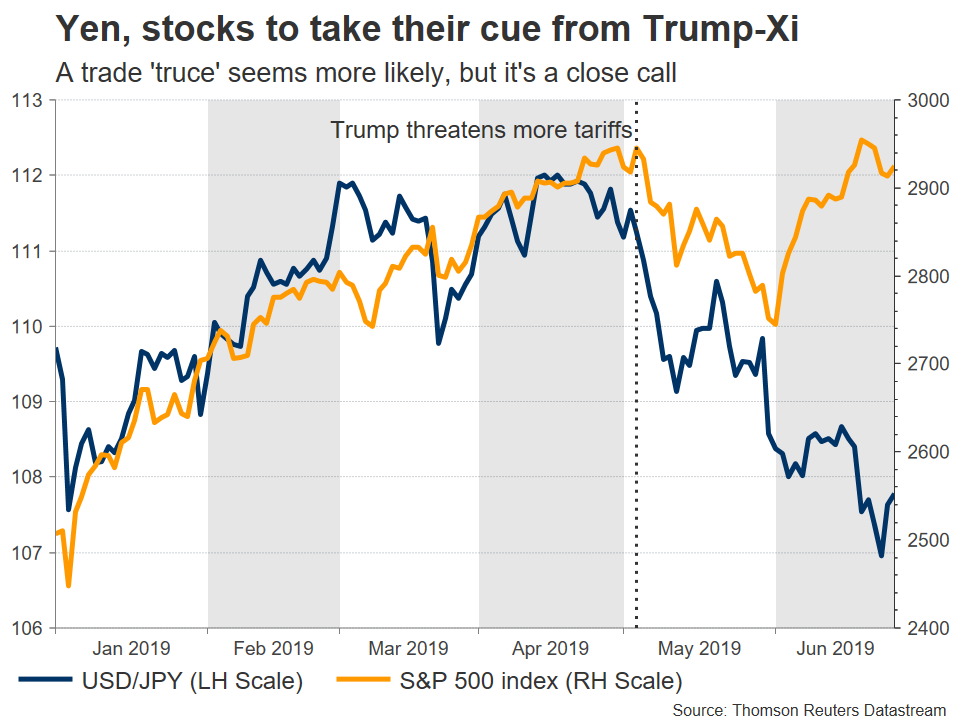

Trump-Xi meeting at G20 paramount for risk appetite

Despite being the epicenter of attention for a while now, the meeting between the American and Chinese leaders hasn’t happened yet – it’s scheduled for Saturday. Thus, markets will probably open with gaps on Monday. Traders hope that Trump and Xi can sort out some of their differences on trade, allowing formal negotiations to resume soon.

On the margin, that does seem like the most likely outcome. Trump wants more talks, something made clear by him calling Xi recently, and China is unlikely to refuse. Even if the two sides remain far apart on key issues, they still have an incentive to portray a positive picture, for fear of damaging business sentiment in their respective home economies if they don’t.

Should the two leaders indeed agree to restart negotiations, stocks would likely be the biggest winner alongside commodity currencies like the aussie and kiwi. Meanwhile, safe havens such as the Japanese yen and gold could give back some of their latest gains.

The risk is that Trump – feeling he has more negotiating leverage with US stocks back at record highs – decides to play more ‘hardball’ and sticks to demands that Xi finds unreasonable. In this case, stocks could drop while haven assets grind higher.

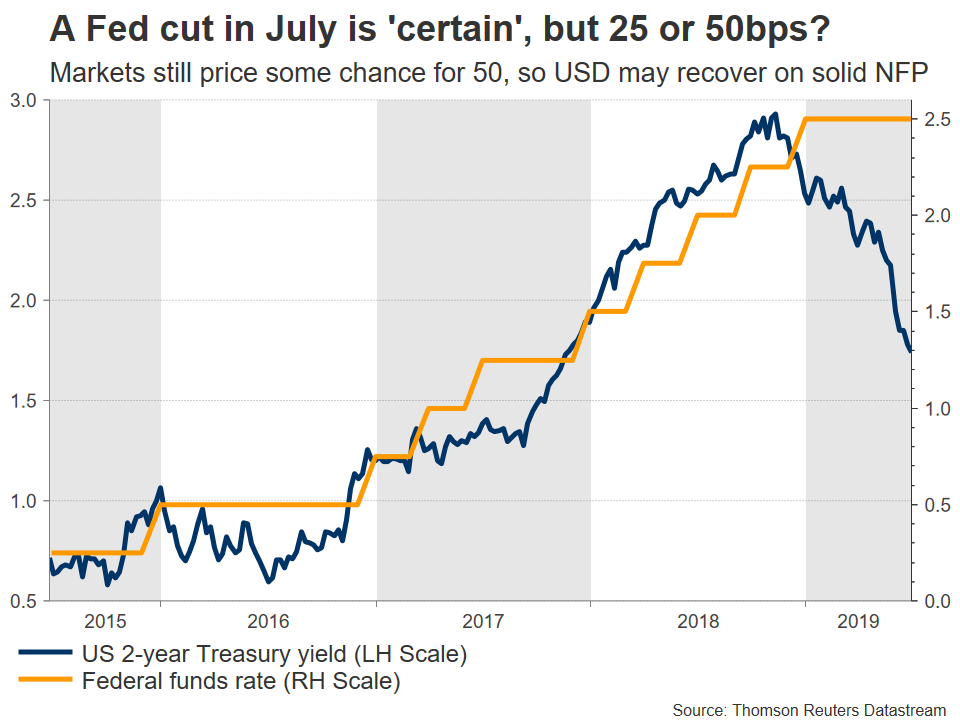

US payrolls & PMIs crucial for how deep the Fed will cut in July

In the US, the week kicks off with the ISM manufacturing PMI for June on Monday. The non-manufacturing survey follows on Wednesday along with the private ADP jobs figures for the same month, culminating with the official employment data on Friday. Forecasts point to a solid report, with nonfarm payrolls expected at 165k, the unemployment rate steady at 3.6%, and a slight acceleration in average hourly earnings.

Since these will be among the final major releases before the Fed’s July policy meeting, they will be crucial in setting expectations for that event. The Fed has essentially locked itself in for a rate cut then – the question is whether it will slash rates by a typical 25 basis points (bps) or whether it will ‘shock’ markets with a more aggressive 50bps cut.

Barring a major disappointment in incoming data, a 50bps move seems a little excessive, as even one of the most dovish FOMC members – James Bullard – pointed out lately. Markets still assign a ~25% probability for a 50bps cut, so the dollar has some room to recover in the next weeks as this is priced out. Overall though, the outlook for the greenback isn’t bright. The Fed has a lot more ‘firepower’ to ease than other major central banks, meaning that the dollar’s potential downside in a prolonged global easing cycle would likely be greater than its peers.

American markets will remain closed on Thursday for Independence Day.

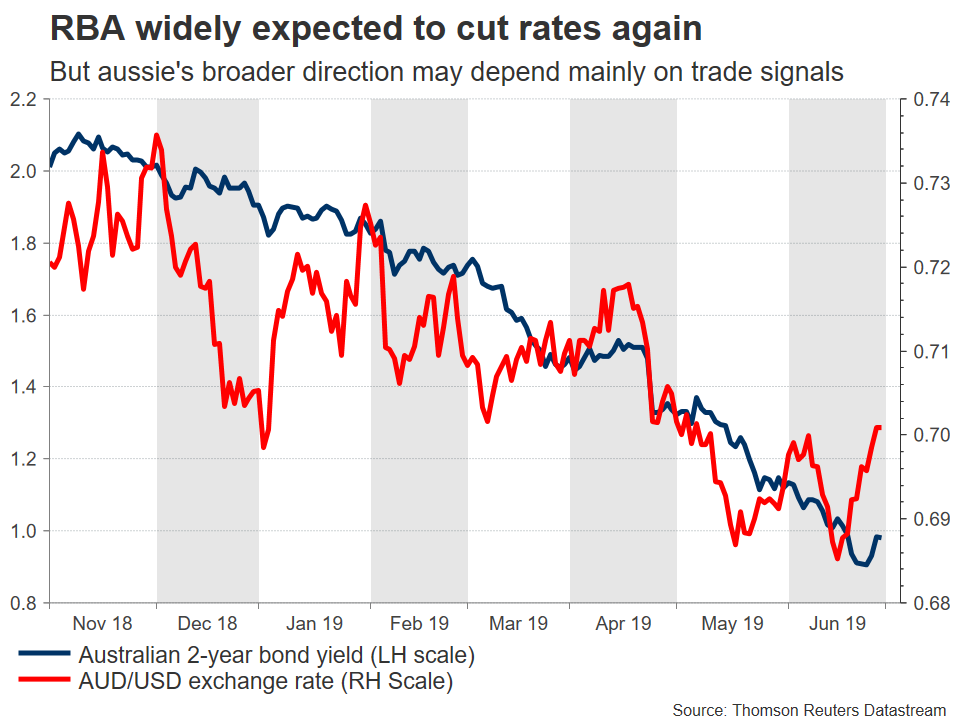

RBA projected to slash rates again

Both economists and markets believe the RBA will cut rates for a second consecutive time when it meets early on Tuesday, with market pricing assigning a 75% probability for such an action. This number jumped lately after Governor Lowe noted that the latest cut by itself would probably not be enough to support the economy.

Despite recent data not being horrible, investors are convinced the RBA will act with force. Perhaps the biggest argument for acting again so soon is the exchange rate. If the Bank doesn’t cut now, then the aussie could surge, especially if the trade signals from the G20 are optimistic. A stronger currency makes it more difficult for inflation to rise, so the RBA likely wants to avoid that route.

While the aussie may drop on a potential rate cut, much of its broader direction will also depend on trade. In other words, a lot of RBA easing is already priced in, and given that the Fed is now also ready to loosen along with other major central banks, monetary policy is not a clear negative force for the aussie anymore. Trade may therefore play an even bigger role in driving the currency moving forward.

Governor Lowe will speak a few hours after the decision, while the nation’s retail sales for May are due on Thursday.

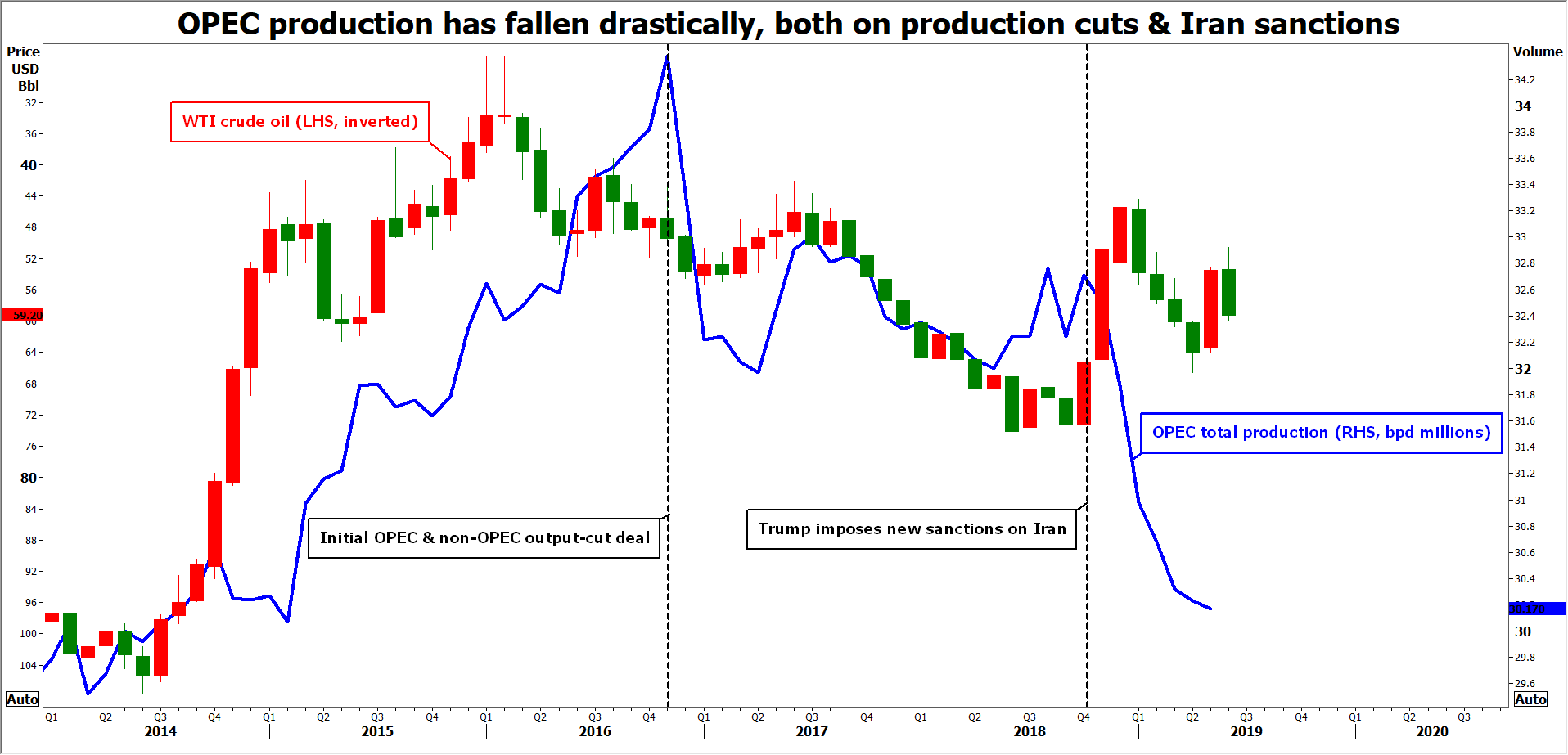

OPEC and allies meet to extend production cuts

It will be a pivotal week for the oil market too. Not only will the G20 outcome shape the demand outlook, but the supply picture will also be updated when OPEC and its allies meet on Monday and Tuesday. The main question is whether these producers will extend their output cuts, and if so, for how long.

Judging by recent comments from the various energy ministers, a 6-month extension seems like a near certainty. This implies that for oil prices to rise materially from here, the cartel needs to deliver something over and above what markets already expect, for instance a one-year extension or deeper production cuts – or both.

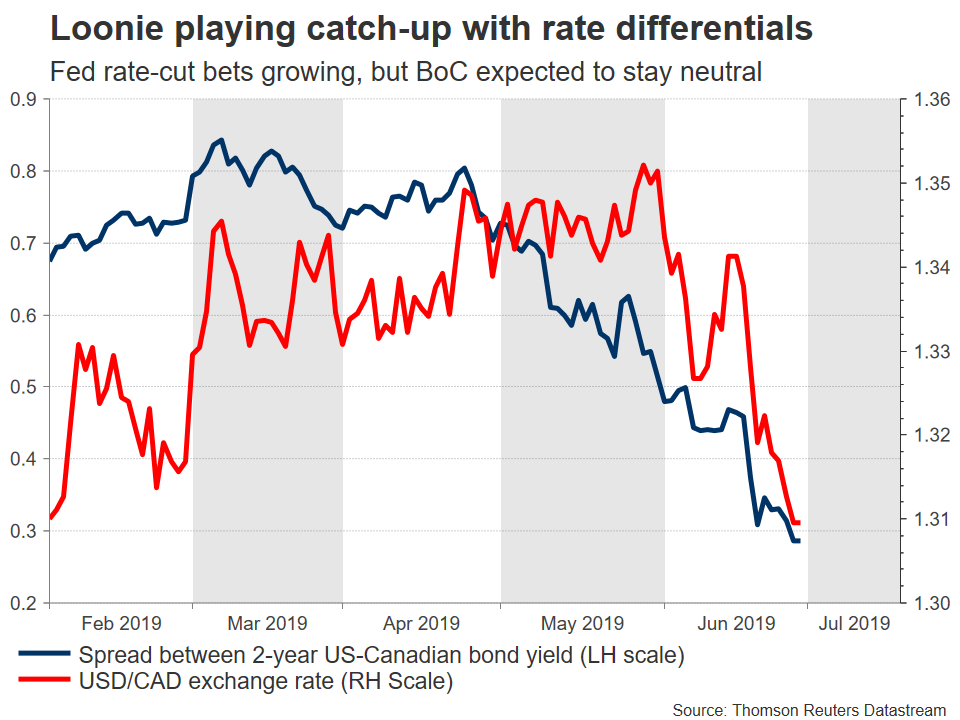

Canadian jobs data on tap as loonie prepares to fly

The yen and the franc may have gotten all the attention lately, but the loonie has also been shining. Canadian economic data are solid, in contrast to most of the world, which puts the Bank of Canada (BoC) in the odd situation of being almost the only major central bank not preparing to cut rates.

Hence, the employment data for June that are due on Friday could be the catalyst for even more gains in the loonie, if they confirm the narrative that the BoC will be an ‘island of neutrality’ as others ease. Before that though, the oil-linked currency will also be sensitive to how the G20 and OPEC meetings play out.

UK PMIs unlikely to distract markets from Brexit

The British pound has recovered some ground lately, partly due to a more conciliatory tone on Brexit by the two candidates aiming to become Prime Minister, and partly due to broad dollar weakness.

In the economic realm, the PMI surveys for June will be released on Monday, Tuesday, and Wednesday for the respective manufacturing, construction, and service sectors – but as usual the currency will probably respond mainly to politics. In that sense, all eyes remain on the Tory leadership race, where Boris Johnson is leading by a wide margin.

Chinese & Japanese business surveys to gauge health of global economy

In China, the PMIs for June will be in focus. The official surveys will be released over the weekend, while the private Caixin figures are due early on Monday and Wednesday for the manufacturing and service sectors, respectively. Admittedly, with the trade war escalating recently, the risks surrounding these numbers seem tilted towards a decline. In such case, global risk appetite could take a hit.

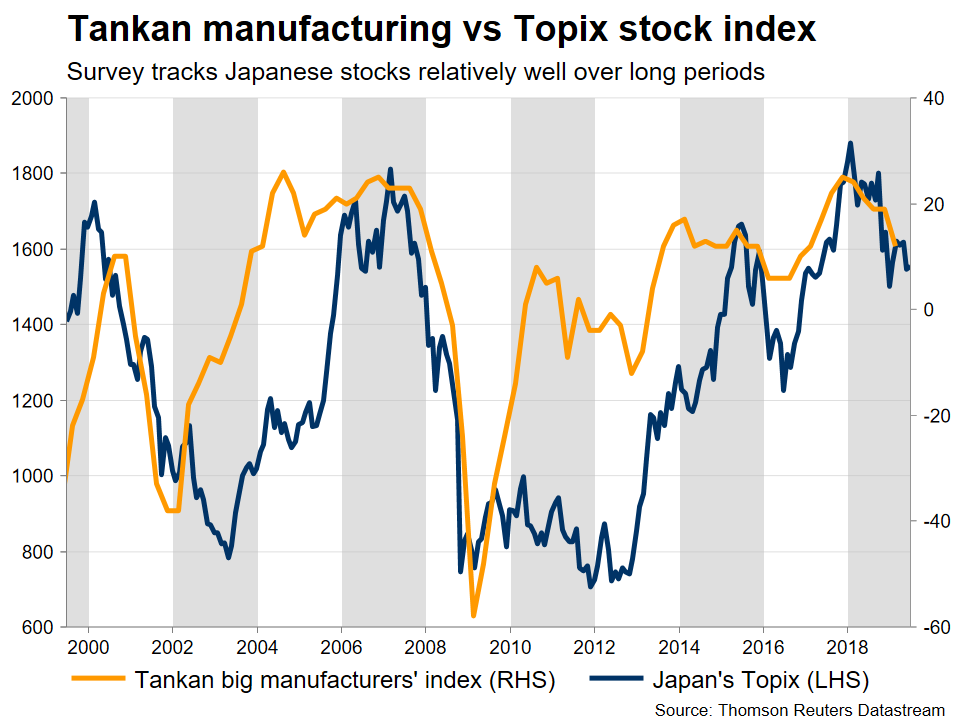

In Japan, the quarterly Tankan survey for Q2 is due on Monday. Forecasts point to a drop in business confidence, which likely reflects trade worries. Regardless, the yen doesn’t typically react to economic data and will therefore take its cue mainly from changes in risk sentiment, given its haven status.

Overall, the outlook for the Japanese currency is improving. Besides risk aversion making a comeback, foreign central banks are also preparing to ease. That could continue to narrow the relative rate differentials between Japan and the rest of the world, making the yen more attractive by comparison.