{kind=link}

U.S. Highlights

- The biggest event this week was the Fed’s pivot away from patience. It is now poised to act in the event of a further deterioration in the outlook. This cheered markets, with stocks and bonds rallying.

- The Fed’s dot plot also showed that the majority of FOMC members judge the funds rate to already be at its long-run neutral level, and expect to lower rates next year. This is a seismic shift from expecting hikes back in December.

- Our new forecast released this week, calls for the Fed to cut rates twice this year, as insurance against the downside risks that have accumulated due to trade tensions, and a late-cycle economic slowdown.

Canadian Highlights

- It was a loaded week on the Canadian economic calendar. The Trans Mountain pipeline project was approved. Construction will take time, but this will eventually help to alleviate pipeline bottlenecks.

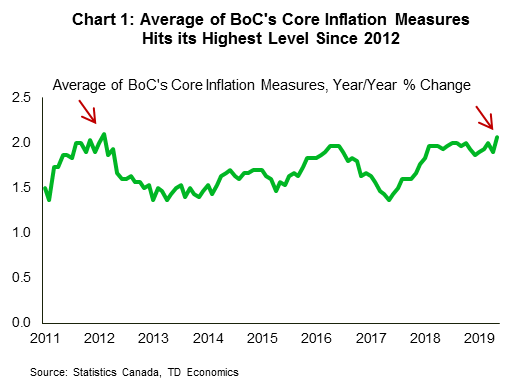

- Inflation surprised to the upside in May, rising to 2.4%. The average of the Bank of Canada’s core measures also moved above 2.0% (to 2.1%) for the first time since 2012.

- Manufacturing and retail sales volumes dipped in April, but are still stronger so far in Q2 compared to Q1, leaving the recovery narrative on track.

U.S. – The Powell Pivot

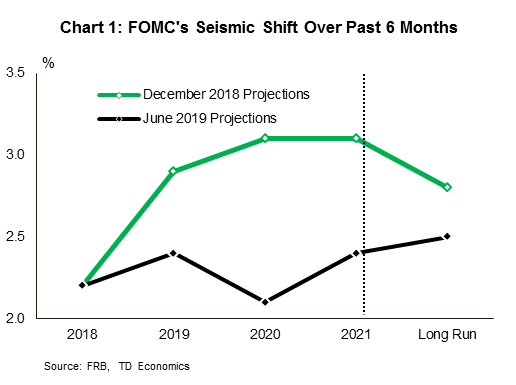

For the second time in the past six months, the Federal Reserve has pivoted on where it thinks interest rates are headed over the next few years. Back in December, the median projection of FOMC members was for 175 basis points of rate hikes by the end of 2020. Now, it is a 25 basis point cut. That is quite the pivot (Chart 1). In its statement the Fed has also shifted from patience to action. The FOMC will now “closely monitor the implications of incoming information for the economic outlook and will act as appropriate to sustain the expansion”.

At the same time, the Fed’s expectations for economic growth have shifted a lot less. The median FOMC forecast for growth is 2.1% this year and 2.0% next year, down only slightly from 2.3% and 2.0% back in December. Looking only at growth expectations it is hard to justify the pivot in interest rates. However, the updated growth forecasts incorporate a lower path of interest rates. Previously, the FOMC believed the economy would grow at that pace as it continued to raise rates. Now it expects that a cut will be required to sustain that near-trend pace.

A big part of the pivot is the continued miss on its inflation forecast. In December, the FOMC expected inflation to be back at 2% by the end of this year, and now that isn’t looking too likely. Given the difficulty sustaining the 2% inflation target, it has lowered its estimate of the “neutral” rate to 2.5%. That is the level at which the rate neither stimulates, nor stifles economic growth. Clearly the Fed has come around to the view that rates over the past little while have been less stimulative than they previously believed.

A majority of FOMC members now believe that at least one rate cut will be required to keep inflation at target and promote maximum employment, and seven out of 17 members judge that it will need two quarter-point rate cuts.

The Fed is paying close attention to signs that the economy is slowing. Both the Philly and Empire Fed manufacturing sentiment indicators released this week showed that sentiment soured in June. Now, those readings may have been taken at the time that the President had threatened tariffs on Mexico, before pulling back at the eleventh hour. But, other manufacturing sentiment indicators globally have cooled, supporting the Fed’s vigilance on downside risks.

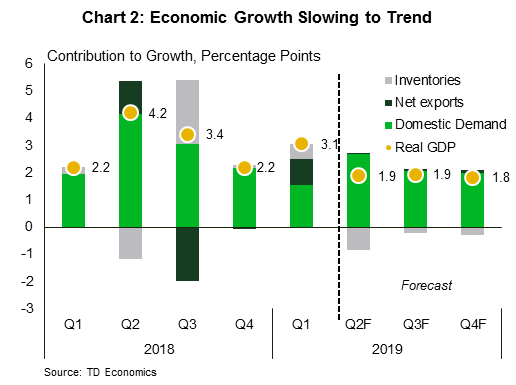

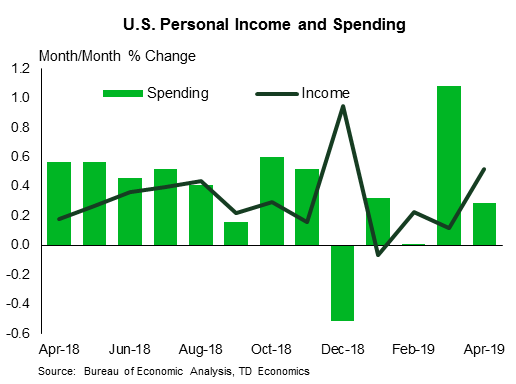

Our recent forecast (Chart 2) lowered our fed funds rate call for this year, adding in two insurance cuts (see report). We expect cuts are needed to keep growth on track, as persistent trade uncertainty weighs on business sentiment and investment. The upside to rate cuts is that they should provide a bit of fuel for the housing market, which has been largely moving sideways over the past year. Housing data for May showed that while construction activity remains lackluster, the resale market increased 2.5% on the month. That suggests the drop in mortgage rates over the past six months may finally be lifting activity. And a more modest path for rates ahead will help improve affordability.

Canada – Data Affords BoC Chance To Be Patient

It was an absolutely loaded week on the economic calendar, capped by a trio of top-tier data releases, a U.S. central bank interest rate decision, and some positive news on the Trans Mountain pipeline to boot. On the latter, the federal government gave the go-ahead for the project while hoping to have shovels in the ground within the next few months. However, with stiff opposition to the project likely to continue, and completion only slated for 2022 at the earliest, it will be some time before relief on pipeline capacity pressures from this channel manifests.

The loonie took flight this week, rising by around 1 cent to about U.S. $0.76 amid the dual-tailwinds of rising oil prices and a softer U.S. dollar. Positive messaging by Trump ahead of his G20 meeting with President Xi and U.S. -Iran tensions sent oil prices higher. And, while the Fed didn’t cut rates, the dovish tilt in communications weighed on the greenback. It also nudged global bond yields lower, including Canadian rates, temporarily erasing gains made on a hotter-than-expected inflation report.

Sticking with the aforementioned report, it appears that inflation is back in Canada, at least temporarily. Headline inflation surprised to the upside, surging 2.4% year-on-year in May from 2.0% the prior month. Surely catching the Bank’s eye, core inflation broke higher, with the average of the three measures coming in at 2.1% (Chart 1) – the strongest since 2012 and two of three core measures rising during the month. However, despite these hot headlines, there are some reasons to fade the strength in this report. Most notably, among the largest contributors to the monthly gain were the traveler accommodations and travel tour categories, with some give back likely in these categories in the months ahead.

Monthly gyrations aside, Canadian inflation remains anchored around the Bank of Canada’s 2.0% target. The upside surprise to inflation is in contrast to recent performances south of the border, where surprises seem to have only come on the soft side. Well-behaved inflation gives the Bank of Canada the leeway to remain on hold, and inflation’s proximity to target implies less urgency to cut rates even if the Federal Reserve does. Details behind our latest economic outlook and rate forecasts can be found here.

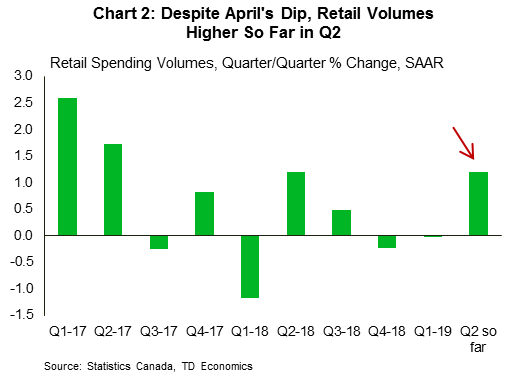

Other major releases were on the softer-side, with manufacturing and retail sales volumes lower in April. Real manufacturing shipments dipped 0.8% during the month, while the inventory-to-sales ratio disappointingly increased. However, other details painted a better picture, as the unplanned maintenance and plant shutdowns that weighed on sales will be reversed in coming months. And, the prior month’s gain was upwardly revised, leaving sales up an annualized 2.1% so far in Q2. A similar picture emerged from the retail spending report, with sales volumes down 0.2% in April, but momentum from Q1 should ensure a decent quarter for spending (Chart 2). As such, the Bank’s (and our own) narrative for stronger Q2 growth remains on track.

U.S.: Upcoming Key Economic Releases

U.S. Personal Income & Spending – May

Release Date: June 28, 2019

Previous: spending: 0.3%; income: 0.5%

TD Forecast: spending: 0.5% m/m; income: 0.3%

Consensus: spending: 0.5% m/m; income: 0.3%

We anticipate spending to have advanced at a strong 0.5% m/m pace in May, up from a 0.3% in April (which may be revised to the upside). We don’t discard a stronger print at 0.6% if the rebound on durable goods spending is stronger than we currently anticipate. In the details, we expect a 0.4% m/m increase in services spending to be the main driver of the May rebound, with a rise in spending on both durables (+2.0%) and nondurables (+0.5%) also helping on the headline. Moreover, we forecast income to rise 0.3% m/m, a tad slower than in the prior month.

Canada: Upcoming Key Economic Releases

Canadian Real GDP – April

Release Date: June 28, 2019

Previous: 0.5% m/m

TD Forecast: 0.2% m/m

Consensus: 0.2% m/m

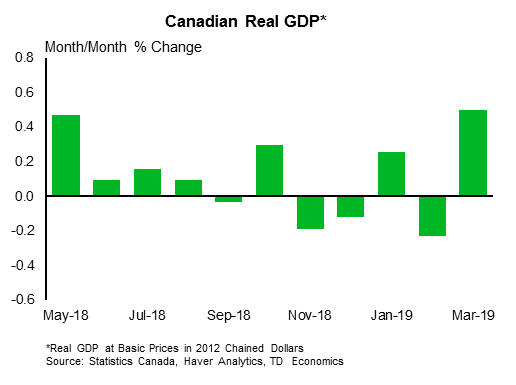

Monthly GDP growth is forecast to slow to 0.2% in April on the heels of a 0.5% increase the prior month. A moderation in services will provide the main driver, as further gains to energy output and strong residential construction drive continued strength in goods-producing industries. This will offset a modest drag from manufacturing, owing to a one-off in auto production, while utilities output is also expected to edge lower. Services will benefit from a rebound in real estate although weaker retail activity will weigh on the sector. However, a 0.2% headline print should provide some comfort to policymakers concerned over global headwinds, and keep Q2 GDP tracking well above the Bank of Canada’s 1.3% projection from April.

Canadian Business Outlook Survey – June

Release Date: June 28, 2019

The Bank of Canada’s Business Outlook Survey should convey a more cautious tone owing to the sharp escalation in global trade tensions since the April report. The previous survey noted that US-China tensions were already weighing indirectly on firms, and in the three months since we have seen a sharp increase in existing tariffs and threats to expand tariff coverage to all Chinese imports. This, alongside the increased tensions between Canada and China will weigh on the balance of opinion around future sales and business investment while other areas of the report will aim to emphasize an improvement on the domestic front following the transitory slowdown in Q4/Q1. The former is likely to set the overall tone, suggesting a high bar for an upbeat message.