{kind=link}

US stocks are poised to open higher after positive steps were taken in both the US -Mexican immigration disputes and after the US and Chinese held candid and constructive talks for the first time since negotiations fell apart a month ago. On Friday night, Mexico reaffirmed their commitments to reduce migration into the US by increasing enforcement on its borders and expanding a program to allow asylum-seekers to remain in Mexico while their legal cases proceed. Mexico legislative body now has to pass the deal forward otherwise President Trump will reimpose the tariffs. Expectations are for the deal to pass and get done quickly.

On Sunday, the Group of 20 major economies finance ministers agreed on join communique that pledged to use all the policies they can to protect global growth from disruptions due to trade and other tensions. Treasury Secretary Mnuchin and China central bank chief Yi Gang signaled a possible turning point after having progressive conversations that seems to signal channels are open again for communication. The next key meeting is expected at the G20 summit in Japan at the end of the month between Xi and Trump.

Treasuries fell as the 10-year yield rose 6.1 basis points to 2.141%, while the dollar had broad gains as gold sold off. The Mexican peso is also having its best gain in almost a year. European indexes had limited gains suggesting the region’s stocks will have a tougher time rebounding back to the April highs.

-

Defense Megamerger – UTX to acquire Raytheon in all-stock deal

-

GBP – BOE to remain on hold as GDP disappoints

-

Oil – Russia remains undecided on extending OPEC + production cut deal

-

Gold – Softer on positive trade developments

UTX/RTN

United Technologies (UTX) reached a deal to merge with defense contractor Raytheon which could support further M&A in the sector. The deal would create an aerospace-and-defense company that is valued over $100 billion with annual revenue of approximately $74 billion, creating a behemoth that would only trail Boeing in sales. The new company will be called Raytheon Technologies Corp. Shares of both companies are poised to open around 4% higher.

The merger will see UTX’s Pratt &Whitney F-35 fighter jet engines combined with Raytheon’s Patriot missile defense systems. The new entity will have a diverse portfolio that will be nicely positioned to thrive even under weakness in defense spending.

In other M&A news, Salesforce is set to buy Tableau for $15.3 billion in an all stock deal. The deal supports Salesforce push in growing their analytics offering.

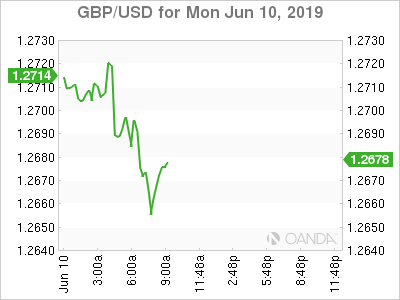

GBP

The British pound extended declines after a wrath of UK data showed broad weakness throughout the entire economy. The headline GDP reading for the month of April was a contraction of 0.4%, much worse the -0.1% dropped eyed. Growth is not expected to deliver any surprises in the second quarter and that should make the Bank of England (BOE) job easy for the next year. Rates are unlikely going nowhere anytime soon.

Production data was also abysmal with the manufacturing posting a 3.9% fall, while the industrial sector slumped 2.7%. Brexit is obviously hurting the data and the planned shutdown of plants could be alleviated once UK leaders are able to deliver a Brexit deal.

Cable is now comfortably below the 1.2700 handle and if we see the 1.2550 breached, price may not find support until the 1.2400 area.

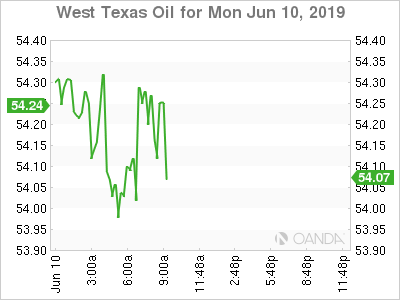

Oil

Russian and Saudi energy ministers held an intergovernmental commission meeting in Moscow as Russia begins to seek a better deal for Russian companies. Oil remained slightly bid after Saudi oil minister Al-Falih said there’s almost unanimous agreement in OPEC to extend production cuts and that Russia could agree before the current deal expires at the end of the month. Al-Falih and his Russian counterpart Novak could meet again at the G20 that occurs at the end of the month. If we see crude prices fall back into bear market territory, we could see the Russians capitulate in extending cuts. OPEC and allies still need to agree upon when to meet, with many pushing for the beginning of July.

Today’s rally in crude stemmed more from the broader risk-on rally that came from positive trade developments. With US rig counts falling four out of the last five weeks, we could see US production ease slightly, providing an opportunity for oil to stabilize once markets properly price in weakness in global demand.

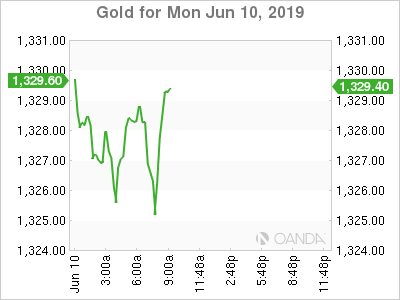

Gold

Gold prices are sharply lower as a plethora off positive market news on trade and M&A eliminated short-term demand for safe-havens. If today finishes out to be a steady grind higher for US equities, we could see gold fall further towards the $1,320 an ounce level. Technical traders are also waiting for a clean break of the $1,350 region, so we could see prices struggle until we a resumption in dollar weakness.