{kind=link}

It’s that time of the month again and all eyes will be on the latest jobs report out of the United States on Friday at 12:30 GMT. The May figures are expected to be somewhat softer from April but no doubt still indicative of a strong economy. However, with markets strongly convinced that the Fed will have to cut rates soon, the jobs data is unlikely to alter those expectations unless there are big surprises in the data.

With some early signs that the US economy could be headed for a slowdown as the worsening trade dispute starts to bite into business confidence, the labour market so far remains very tight. But despite the decades-low unemployment rate, wage growth has been disappointingly tepid, keeping a lid on inflationary pressures.

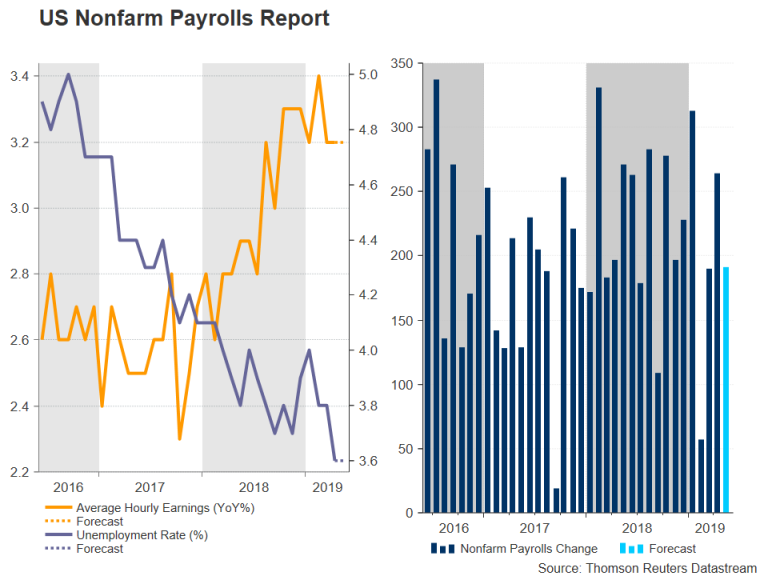

Fewer jobs likely added in May

The May report is expected to underline this picture. Nonfarm payrolls are forecast to have risen by 185k in May, easing from the prior number of 263k. Anything above 100k is seen as consistent with jobs growth keeping up with population growth, meaning alarm bells won’t be ringing about the labour market until the headline figure drops below this benchmark.

The jobless rate is forecast to stay unchanged at the 49-year low of 3.6%. More significantly, average hourly earnings are expected to have increased by 0.3% month-on-month, which would keep the annual rate at 3.2%. Wage growth has eased slightly from the decade-high of 3.4% y/y reached in February in a setback for policymakers who were hoping a healthy jobs market would fuel pay increases, which in turn would drive consumer prices higher.

Moderate wage growth a concern for the Fed

A further easing in wage growth would be a major worry for the Fed given that the central bank’s favoured inflation gauge, the core PCE price index, is already running uncomfortably below the 2% target; it stood at 1.6% y/y in April. Some would argue that alone gives the Fed a strong case to lower borrowing costs even before there’s been a notable impact from the brewing trade tensions.

Markets have clearly made up their minds, though, as Fed fund futures are pointing to as much as three 25-bps rate cuts over the next 12 months. That’s been enough to send Treasury yields spiralling downwards and the US dollar losing its safe-haven allure to plunge against its major peers.

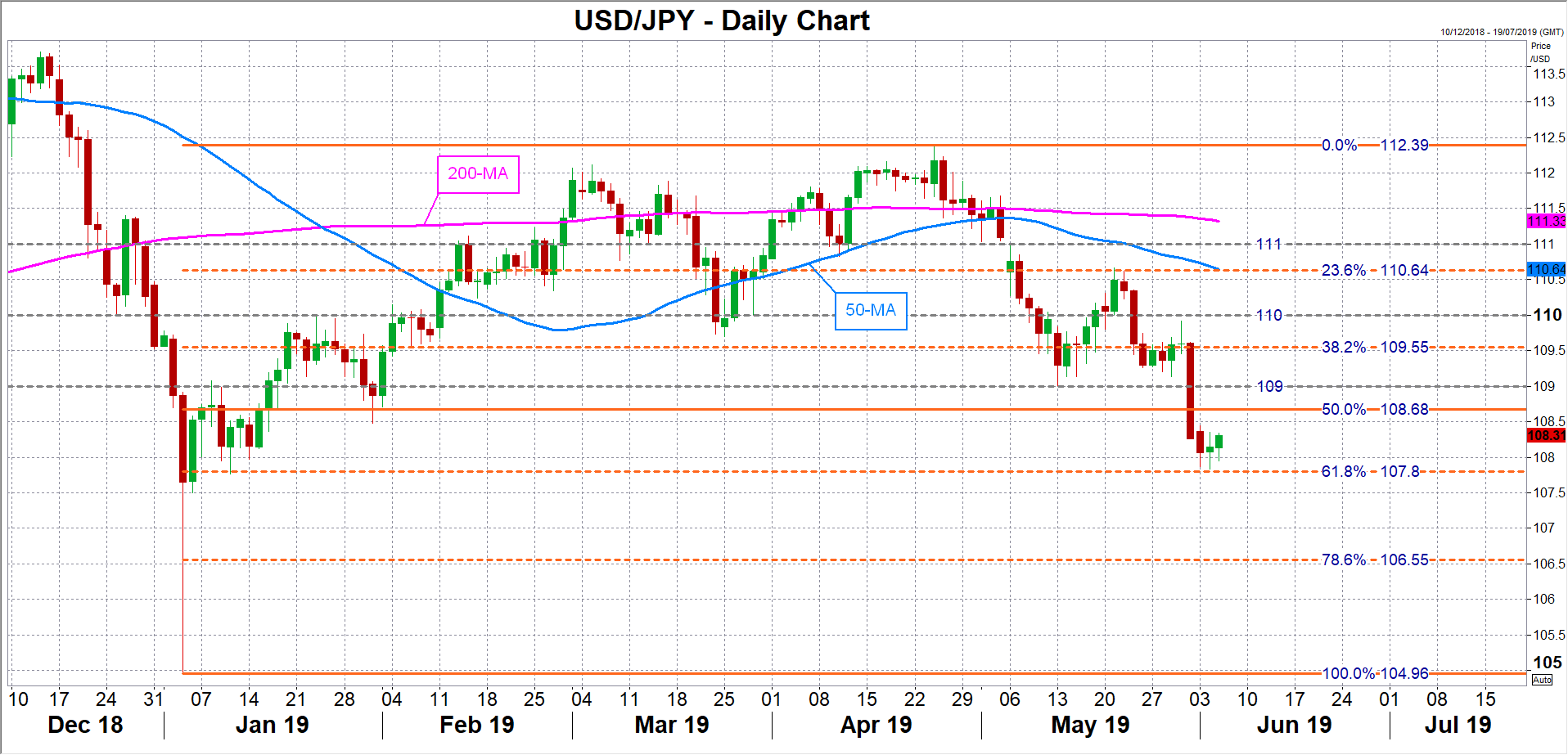

Dollar seeks support, looking for a rebound

At the moment, the dollar has found support at the 61.8% Fibonacci retracement of the 104.96-112.39 uplgeg at 107.80 yen. Should a weaker-than-expected jobs report pull dollar/yen below this level, the next support could arrive at the 78.6% Fibonacci at 106.55.

However, if the payrolls data impresses, giving the Fed reason to remain patient, the bulls could see ground for a rebound. A possible important resistance level to overcome that could help ease the selling pressure is the 23.6% Fibonacci at 110.64, which is near the 50-day moving average.

Traders may be cautious ahead of June Fed meeting

But with the next FOMC meeting about two weeks away, market reaction to the NFP report may be muted and investors will probably be paying more attention to what Fed officials will be signalling in their remarks in the coming days ahead of the blackout period before the meeting.

St. Louis Fed President James Bullard became the first voting FOMC member to suggest the Fed should cut rates if the trade uncertainty causes a sharper-than-expected slowdown in growth. Fed Chairman Jerome Powell gave less away when he spoke on Tuesday. However, he did indicate the Fed was ready to act “as appropriate” to the growing risks to the economy, potentially opening the way for a rate cut.