{kind=link}

Thursday May 23: Five things the markets are talking about

U.S equity futures and European bourses are again under pressure, following Asian stocks lower, as Sino-U.S trade tensions show little sign of easing. The street is now officially worried that what started as a ‘tiff over tariffs’ is turning into a full-blown trade war. U.S Treasuries are steady while the ‘big’ dollar remains King.

Yesterday’s FOMC minutes showed that U.S policy makers are broadly comfortable with their current “make-no-moves” posture. A number of officials said they thought the Fed might need to raise rates because they expected tight labour markets to eventually lead wages and prices to rise, while others thought there was more labour slack than implied by the unemployment rate, at +3.8% in April.

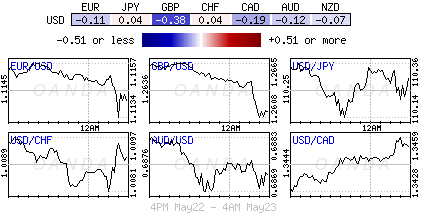

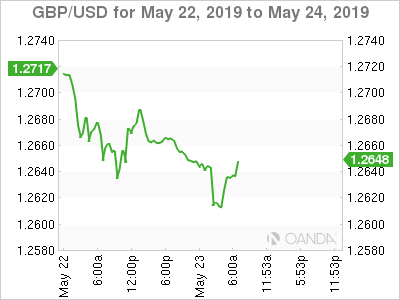

In FX, the pound has extended its losses amid a “growing revolt over Brexit” that looks increasingly likely to force PM Theresa May from power sooner rather than later. Europe’s single unit, the EUR is steady as voting gets underway in Day 1 of the European elections. While crude oil comes under pressure from inventory data and commodities from a “grinding trade war.”

On tap: Fr. & Gr. flash services & manufacturing PMI, Day 1 EUR parliamentary elections (May 23), GBP retail sales, Day 2 EUR parliamentary elections & U.S durable goods (May 24), Day 3 EUR parliamentary elections (May 25).

1.Stocks sea of red, except for India

In Japan, the Nikkei dropped overnight after renewed U.S-China trade tensions dragged down tech stocks, while index-heavyweight SoftBank Group fell more than -5%. The Nikkei share average ended -0.6% lower, while the broader Topix lost -0.4%.

Note: SoftBank Group, which has a stake in Sprint, fell on news that the U.S Justice Department’s have recommended the agency blocks T-Mobile US Inc’s +$26B acquisition of smaller rival Sprint.

Down-under, Aussie shares ended lower, ending six consecutive sessions of gains, on concerns U.S-China trade frictions were spilling into the tech sector. The S&P/ASX 200 index fell -0.3%. The benchmark rose +0.2% on Wednesday. In S. Korea, The Kospi index closed down -0.26%.

The outlier in Asia, Indian shares hit a record high overnight as results showed that the incumbent Modi-led coalition is leading in most seats in the lower house of Parliament and is set to win re-election.

In China, the blue-chip stock index dropped to a three-month low, as investors dumped tech names amid worries that Chinese tech firms could bear the brunt of an escalating trade war. The blue-chip CSI300 index fell -1.8%,while the Shanghai Composite Index lost -1.4%.

In Europe, regional bourses have declined sharply across the board led by losses in the auto and tech sector amid weaker than expected PMI data from Germany and Eurozone and German IFO Business Climate release.

U.S stocks are set to open deep in the ‘red’ (-0.8%).

Indices: Stoxx600 -1.24% at 374.50, FTSE -1.07% at 7,255.83, DAX -1.58% at 11,976.78, CAC-40 -1.54% at 5,296.19, IBEX-35 -1.24% at 9,121.00, FTSE MIB -1.54% at 20,255.50, SMI -0.53% at 9,593.80, S&P 500 Futures -0.75%

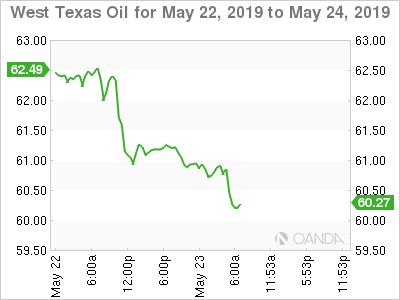

2. Oil slips -1% as U.S. stockpiles surge, gold little changed

Oil prices remain under pressure, extending this week’s falls amid surging U.S crude inventories and weak demand from refineries.

Brent crude futures are at +$70.36 per barrel, down -63c, or -0.9%, from Wednesday’s close. U.S West Texas Intermediate (WTI) crude futures are down by -51c, or -0.8%, at +$60.91 per barrel.

Note: Crude futures fell by around -2% Wednesday.

Data from the EIA Wednesday showed that U.S crude oil inventories rose last week, hitting their highest levels in nearly two-years, due to weak refinery demand. Commercial U.S crude inventories rose by +4.7M barrels in the week ended May 17, to +476.8M barrels, their highest since July 2017.

Despite weak refinery demand for feedstock crude oil, the increase in commercial inventories also came on the back of planned sales of U.S strategic petroleum reserves (SPR) into the commercial market. U.S crude oil production climbed by +100K bpd to +12.2M bpd.

Crude ‘bears’ have been getting a helping hand from slowing demand growth due to the negative impact on the global economy of the Sino-U.S trade war, while the crude ‘bull’ has been relying on escalating political tensions between the U.S and Iran, as well as ongoing supply cuts led by OPEC+.

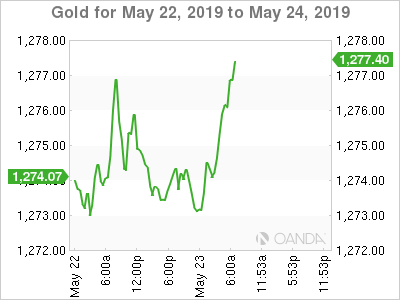

Ahead of the U.S open, gold prices are little changed as simmering Sino-U.S trade tensions support the dollar, while the ‘yellow metal’ investors continue to look for a direction after the Fed minutes indicated that U.S rates will remain unchanged for the foreseeable future. Spot gold is flat at +$1,274.03 per ounce, just shy of its lowest level in three-weeks at +$1,268.97. U.S gold futures are unchanged at +$1,274.20.

3. German Bund yields still negative after trade gloom hits PMI

Germany’s 10-year Bund yield fell further into deeply negative territory this morning after a survey showed business activity in the bloc was weaker (see below) than expected in May, adding further evidence that trade wars are dampening economic growth.

Note: Eurozone PMI’s – in the individual readings, French business activity jumped to its strongest level in six months, but German business activity undershot expectations.

Germany’s 10-year Bund yield has fallen to an intraday low of -0.111%, sliding back down towards the recent three-year low of -0.132%. French 10-year OAT yields are also under pressure, falling to +0.29%, down -1.5 bps.

Note: European parliamentary elections begin today, and initial results will be announced on Sunday evening.

Elsewhere, the yield on 10-year Treasuries has dipped -1 bps to +2.37%, the lowest in two-months. In the U.K, the 10-year Gilt yield has declined -3 bps to +0.986%, the lowest in more than 20-months, while in Italy, the 10-year BTP yield has advanced less than +1 bps to +2.637%.

4. Dollar in demand

Sterling bears believe the pound is on course to hit £1.25 sooner rather than later now that PM May could be resigning sometime over the next week since she has lost the support of some of her key cabinet members and replaced by a hard Brexiter. However, any positive comments about Brexit and a break of the £1.27 handle could see a gap higher as the weaker shorts seek a quick exit.

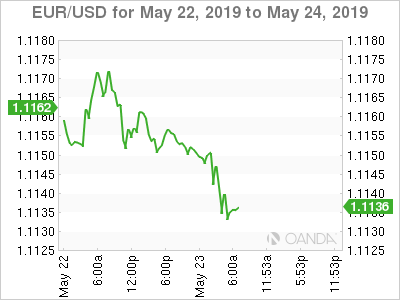

EUR/USD (€1.1131) the single unit continues its slow grind down lower towards the €1.1050 handle as Euro area Flash PMI figures showed a mixed bag in both services and manufacturing (see below). The EU Trade Minister also commented that they were ready to start trade talks, but believed the US was not ready to start tariff discussions.

The PBoC moved the dollar-yuan fix by only ¥0.02 for a third-straight day as the midpoint of daily trading remains stronger for the Chinese currency than where prior-day trading closed. The overnight fix was at ¥6.8994, vs. ¥6.8992 Wednesday. The ‘big’ dollar weakened in onshore trading, finishing at ¥6.9040.

5. German business sentiment deteriorates sharply as do PMI’s

Euro data this morning showed that German business sentiment dropped this month, as companies’ assessment of their current situation worsened.

The Ifo business-climate index slipped to 97.9 points from 99.2 points in April. Market expectations were looking for a reading of 99.1 points for May.

However, not all was negative, according to the Ifo companies in Germany’s important manufacturing sector raised their expectations for the first time since 2018.

In the chemicals industry, “optimism has taken the place of recent pessimism,” Ifo President Clemens Fuest said, but he added that “the German economy is still lacking in momentum.”

Elsewhere, the eurozone flash PMI’s for May remained fairly weak, suggesting that the eurozone economy slowed in Q2. The slight increase in the Composite PMI, from 51.5 to 51.6, was in line with the consensus (51.7). Digging deeper, the manufacturing component rose from 48.0 to 49.0, but remained below 50 for the fourth consecutive month, while the services component was unchanged at 52.5.