{kind=link}

- Sterling hammered on expectations PM May could resign soon

- German PMIs disappoint – euro may stay under pressure

- Risk aversion deepens as markets fear ‘new cold war’

- Fed minutes reaffirm neutral stance, dollar advances

No reprieve for sterling as May fights for political survival

The British pound continues to be hammered by political uncertainty, with the leader of the House of Commons – Andrea Leadsom – resigning from the cabinet yesterday in protest to the government’s Brexit approach. The move came after Prime Minister May unveiled a ‘softer’ Brexit plan that opened the possibility of another referendum, infuriating Brexiteers in her Conservative party. The knives are truly out for May, who has come under unprecedented pressure to step down before this week ends.

Whether that happens or not might depend to a large extent on how her Conservative party performs in today’s EU Parliament elections. If the Tories suffer as heavy a defeat as opinion polls suggest, with many of their voters defecting to the new Brexit Party, that could cause both May to quit and the Tories to start looking for a hardline Brexiteer to replace her. Naturally, that may raise the odds of a no-deal Brexit down the road, spelling more trouble for sterling.

German PMIs suggest little scope for euro rebound

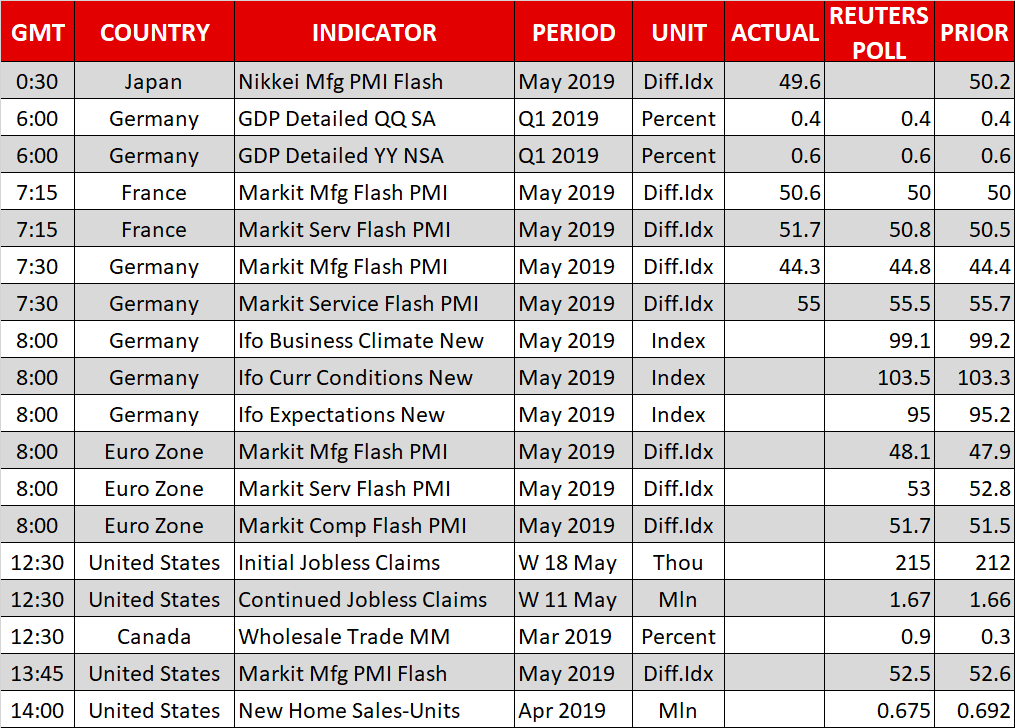

Any material rebound in the euro is probably a long way off still, as the outlook for growth in the euro area remains gloomy. Germany’s preliminary PMI surveys for May released earlier today disappointed, with the manufacturing index sinking deeper into contractionary territory and the services print falling by more than expected.

Europe’s largest economy is therefore still struggling, which may help eliminate any surviving expectations for policy normalization by the ECB. As for the euro, until growth in the bloc starts showing signs of recovery, any rallies may remain relatively short-lived. There’s also the risk of Eurosceptic parties becoming a dominant force in the EU Parliament after the elections this weekend.

Risk aversion deepens on fears of ‘new cold war’

Global stock markets are a sea of red on Thursday, with most Asian indices closing lower while futures tracking European and American bourses are pointing to a negative open, as trade concerns continue to dominate. China stepped up the rhetoric lately, with the nation’s foreign minister saying that the US is trying to hinder the nation’s development process. The overall sense in the market is that this conflict is quickly morphing from a trade dispute into a new cold war, particularly since ‘twitter diplomacy’ leaves little room for either side to back down without losing face.

Fed minutes stress neutral stance, dollar likes it

The Fed minutes released yesterday confirmed that the central bank is firmly on hold. Most policymakers shared the view that the latest shortfall in inflation is transitory, and more importantly, there wasn’t any discussion about cutting rates. This stands in stark contrast to market pricing, which still suggests a rate cut by December is a done deal.

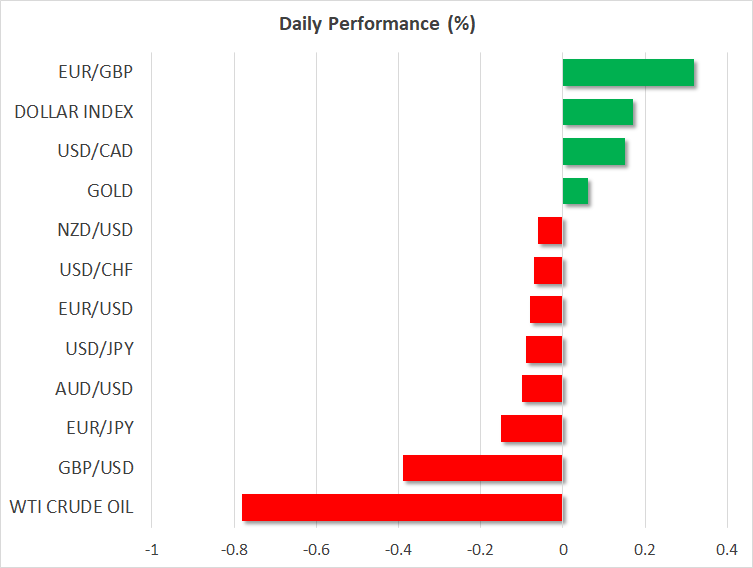

As for the dollar, it moved a little higher in the aftermath and is extending its gains today. In the big picture, the greenback could remain the market’s ‘darling’, at least until one of the bleak narratives in the other major economies starts to improve. In this sense, the biggest downside risk for the dollar would be a material rebound in European growth, which as shown by today’s euro area PMIs, is not there yet.