{kind=link}

The movements in early Wednesday trade from Asia suggest that investors are tepidly putting some risk back on the table, even as uncertainties surrounding US-China trade tensions continue to cast a cloud over market sentiment. Most Asian stocks are trading in positive territory, perhaps taking their cue from US counterparts which rebounded from the sharpest drop in four months.

With Donald Trump downplaying trade tensions between the United States and China as a “little squabble”, there is cautious optimism that both sides will eventually reach a trade deal, with investors potentially looking at the G20 meeting in Japan next month as a possible target for a breakthrough in trade relations. It is likely that European markets will attempt to benefit from the positive tone seen in the previous US and Asia trading sessions, but this does not change the fact that spectators are very concerned that both Washington and Beijing have raised tariffs on each other’s goods. This is a major negative for the world economy and investors should remain alert as global sentiment remains fragile and highly sensitive to trade developments.

US retail sales, industrial production data may serve as near-term Dollar catalysts

The US Dollar can continue its climb from Tuesday’s trading session, should the US retail sales and industrial production data due later on Wednesday, come in better-than-expected. The Greenback’s upward trajectory in 2019 should remain intact as long as the US economy continues to be in a “good place”, as often referenced by Fed officials. Broader concerns over the ramp-up in US-China trade tensions should also support the US Dollar, as it offers investors refuge during periods of uncertainty.

Greenback steady even as Trump repeats call for lower US interest rates to “match” China stimulus

US President Donald Trump has once again called on the Federal Reserve to lower interest rates, in a bid to “match” stimulus measures in China. He described such a move by the US central bank as “game over”, and that the US will win in its trade conflict with China.

Amid such repeated calls by Trump for US interest rates to be lowered, the Dollar Index is holding around the 97.5 mark at the time of writing, even though the Fed funds futures now point to more than a 70 percent chance of an interest rate cut by December. Markets are casting an eye over the potential ramifications of heightened trade tariffs on the US inflation and growth outlook, which may ultimately tip the balance in favour of a Fed rate cut before 2019 is over.

Currency spotlight – EURUSD

Elsewhere, the Euro offered a fairly muted reaction this morning despite the first estimate of German Q1 GDP printing above market expectations. Economic growth in Germany expanded 0.7% year-on-year during the first quarter of 2019. The Euro is likely to remain on standby until Eurozone Q1 GDP figures are released later in the day. Should the pending GDP figures from Europe meet or exceed market expectations, the Euro has scope to push higher against the Dollar and other major currencies. We should however not discount the threat that downside risks to the Eurozone economy from external headwinds can lead to a flurry of selling positions on the Euro entering the market.

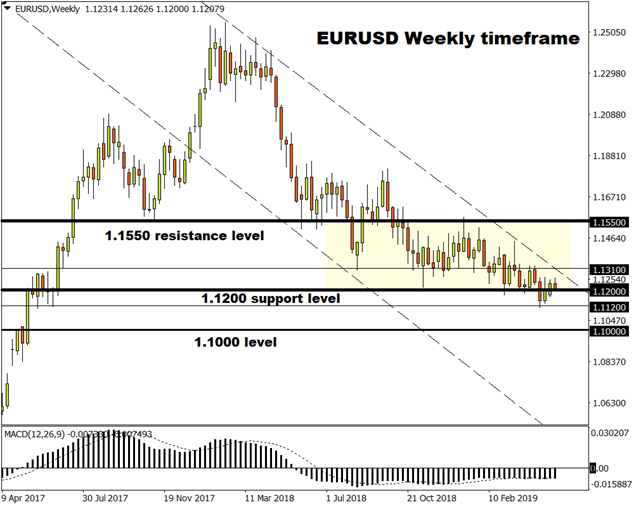

Focusing on the technical picture, the EURUSD remains bearish on the weekly timeframe with prices trading within a bearish channel. A solid weekly close below the 1.1200 support level is likely to inspire a steeper decline towards 1.1120 and 1.1000 in the medium term. Should 1.1200 prove to be a strong support level, the EURUSD could test 1.1310.