{kind=link}

The RBNZ will announce its decision early on Wednesday, at 02:00 GMT. The forecast from economists is for a rate cut, but investors are not convinced, with market pricing assigning only a ~40% chance for one. Indeed, the Bank may hold its fire for now and postpone any cut until the summer. The kiwi will probably spike higher in that case, though any positive reaction could be short-lived.

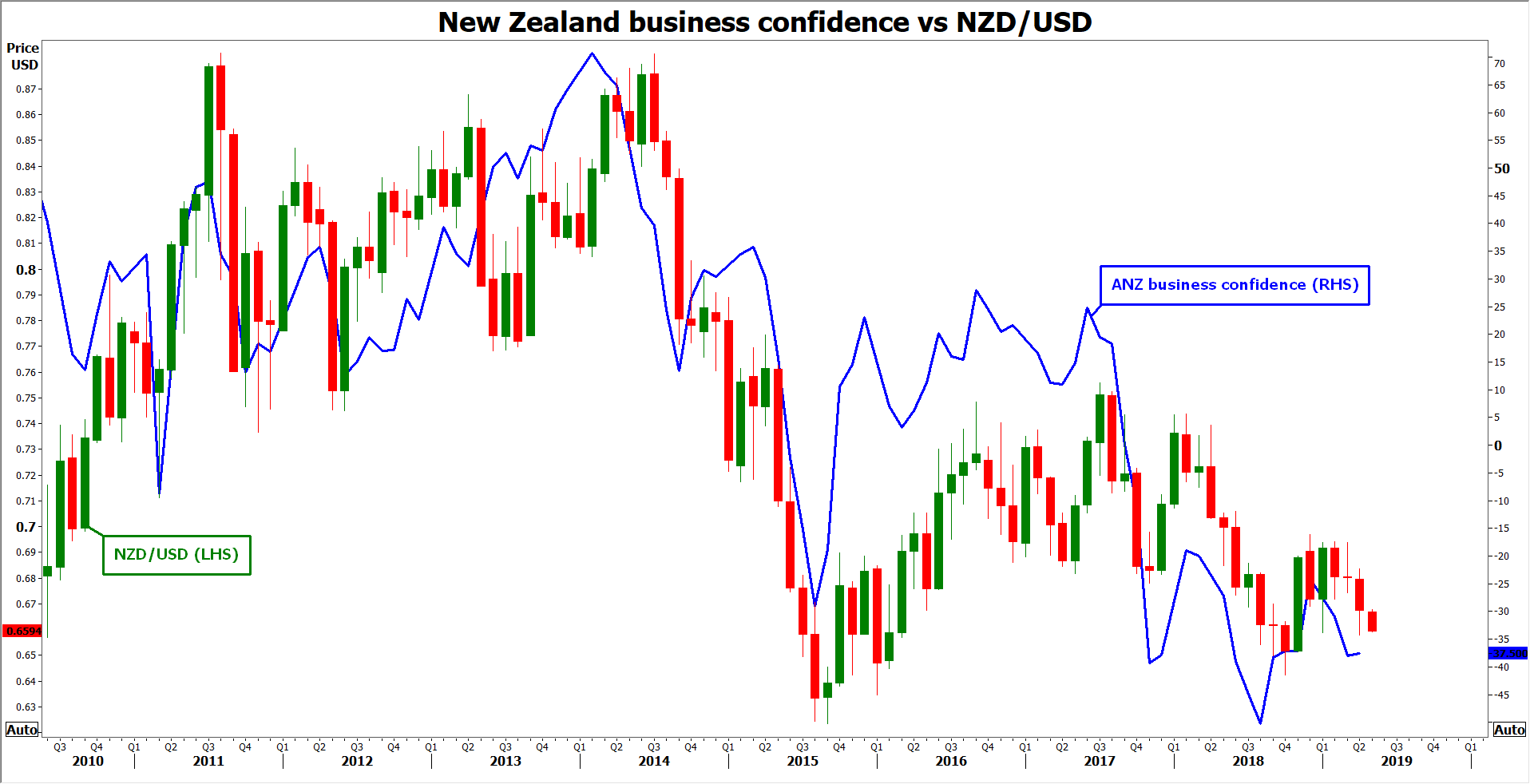

The Reserve Bank of New Zealand (RBNZ) adopted a clear easing bias when it last met in March, indicating that the next move in interest rates will likely be lower given weakness in both the domestic and the global outlook. Since then, developments have been mostly discouraging, with inflation and wage growth slowing in Q1, while the labor market cooled. Likewise, business confidence remains extremely low, spelling downside risks for business investment and therefore for future growth.

It’s not all bad news, though. Prices for commodities New Zealand exports, like dairy and milk products, are rising. Meanwhile, the kiwi is trading much lower than what the RBNZ had estimated in its latest forecasts, which combined with rising oil prices, paints a brighter picture for future inflation. A weaker currency raises import prices, exerting upward pressure on overall inflation. More importantly, China’s economy seems to be stabilizing after a barrage of stimulus, though recent news that the US could soon impose new tariffs will probably keep a lid on such optimism.

This brings us to this week’s meeting. Markets seem uncertain of whether the RBNZ will cut rates right now, assigning a ~40% chance for a cut tomorrow. Yet, a rate cut by August is more than fully priced in, which shows that traders believe it’s a matter of when, not if, the RBNZ will ease.

It’s a close call, but risks seem tilted towards the RBNZ postponing any rate cut for the summer, effectively buying itself some time to examine more data before acting. The economy is softening, but not dramatically, so there’s little pressure to cut rates immediately. Since this meeting is accompanied by new forecasts, the Bank could still keep the easing narrative alive by projecting a lower path for interest rates, consistent with its dovish language.

As for the market reaction, if the Bank indeed keeps rates unchanged for now, the initial reaction in the kiwi will likely be higher. That said, if the RBNZ also reinforces market expectations for future cuts by revising down its rate forecasts, any positive reaction could be relatively short-lived.

Another factor arguing for the kiwi to gradually reverse lower, even in case of an on-hold decision, is the risk of further escalation in the US-China trade conflict. Markets have largely shrugged off such concerns so far, effectively betting that Trump is only posturing to gain negotiating leverage – which may be wishful thinking.

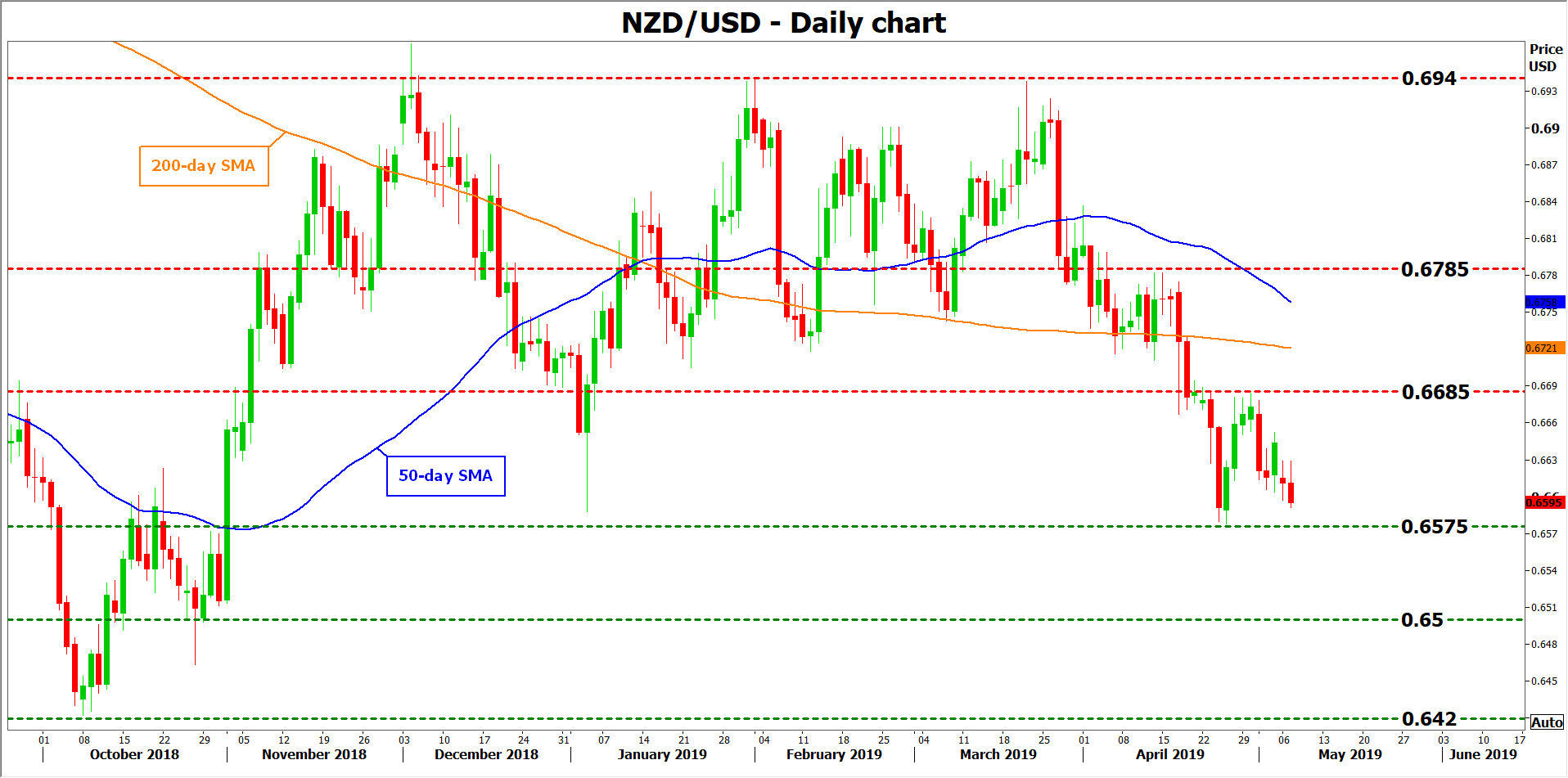

Technically, initial resistance to advances in kiwi/dollar may be found around 0.6685, the April 30 high, with an upside break aiming for the 200-day simple moving average (SMA) at 0.6721.

Technically, initial resistance to advances in kiwi/dollar may be found around 0.6685, the April 30 high, with an upside break aiming for the 200-day simple moving average (SMA) at 0.6721.

On the flipside, if the Bank does cut rates, the pair could fall below 0.6575 to test the 0.6500 handle. Even lower, attention would turn to the October lows near 0.6420.