{kind=link}

U.S. Review

The Economy is Not in Danger of Stalling Anytime Soon

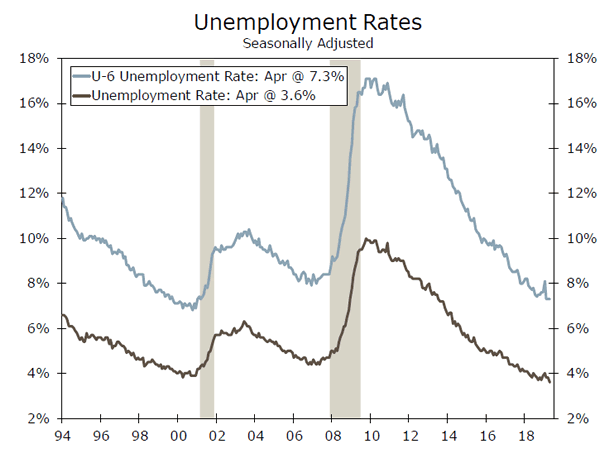

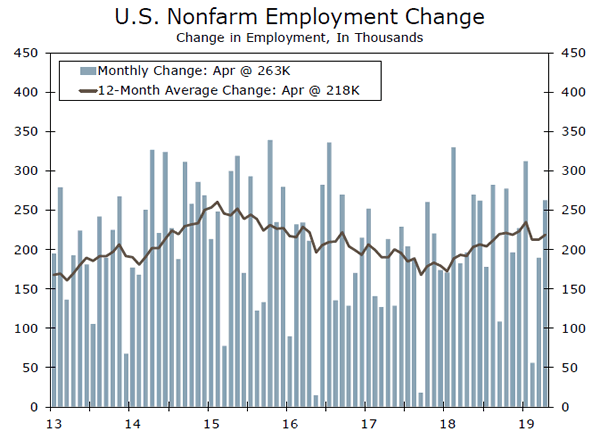

- Employers surpassed expectations, adding a whopping 263,000 jobs in April. The unemployment rate trended lower to 3.6%, but that was due entirely to a drop in the labor force participation rate. Nonetheless, the jobs market remains tight.

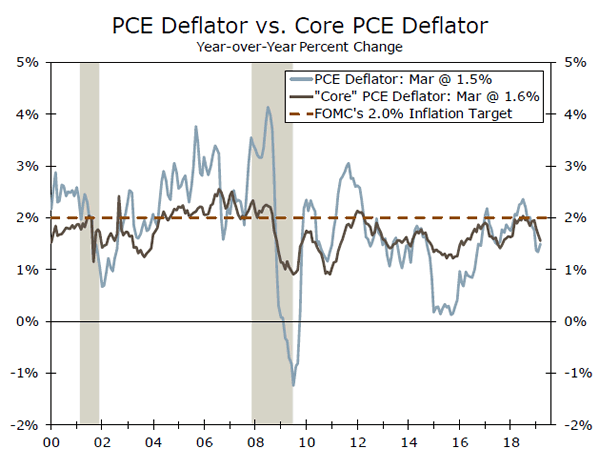

- Following the dip in the core PCE deflator, the FOMC has maintained its pledge to be patient, and left rates unchanged this week. For a detailed look at inflation, and whether the recent softness is, as Powell characterized it, “transient” we direct you to our Topic of the Week section on Page 7.

- Our main take this week: Despite the labor market remaining tight, with inflation low we still expect the FOMC to refrain from raising rates this year.

The Economy is Not in Danger of Stalling Anytime Soon

We wrote last week that the underlying details of economic growth in the first quarter were not as strong as the headline GDP growth rate would suggest. While we stand by that deduction, data this week confirm our second stated conclusion: the economy is not in danger of stalling anytime soon.

There were two events that captured markets’ attention this week: the FOMC policy meeting and the April nonfarm payrolls report. The meeting was of particular focus, not because of the widely expected outcome for rates to be left unchanged, but for any changes in the policy statement and Powell’s post-meeting press conference. The notable change to the statement was the downgrade to the inflation assessment, which followed the drop in the core PCE deflator to 1.6% on a year-ago basis in March—the lowest level in a year and a half. When questioned about the recent weakness in inflation, Powell emphasized “transient” factors as the culprit behind the pull-back. Is the recent weakness in inflation exaggerated relative to its trend? Please see our Topic of the Week on page 7 for further analysis of this topic.

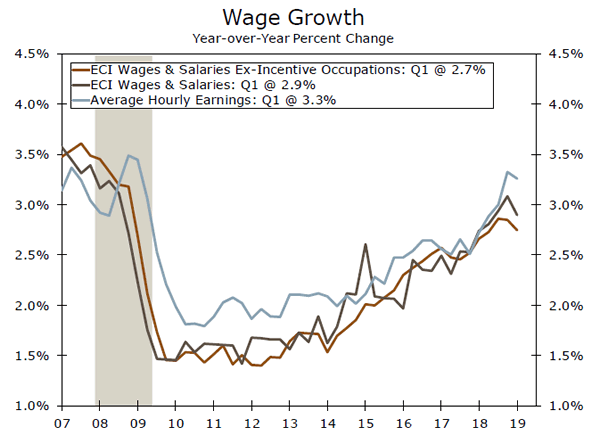

Here we turn your attention to the other end of the Fed’s dual mandate—employment. Employers added a whopping 263,000 jobs in April—beating the consensus expectation of a 190,000 job gain. The unemployment rate fell to 3.6%, the lowest in almost 50 years. But, the underemployment rate, which includes those marginally attached to the labor force, held steady at 7.3%, and average hours worked nudged down to 34.4 hours. The drop in unemployment therefore stems entirely from the give-back in labor force participation.

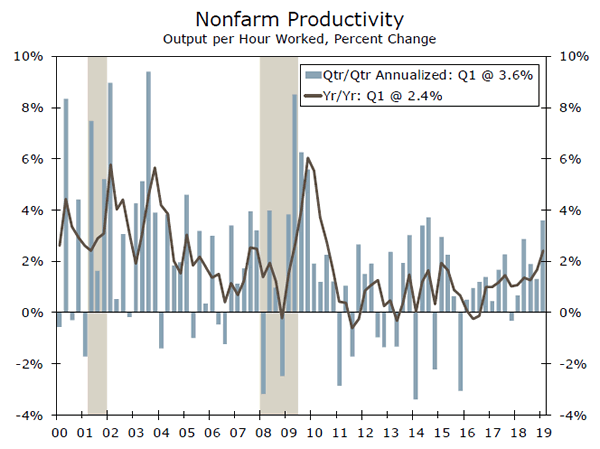

In a recent report we discuss how the recent rebound in participation, which has kept wage pressures from building to the point where labor costs would set off higher inflation, has provided the FOMC another reason it can be patient with additional rate hikes. Indeed, average hourly earnings rose only 0.2% in April from the prior month. But given they were likely held down by the timing of the survey week as well as more working days than average last April, we expect the upward trend in average hourly earnings to resume over the next couple of months. More broadly, the first look at the employment cost index in the first quarter suggested employment costs remained in line with the recent trend. With the labor market still tight, we expect to see labor costs pick up a bit in coming quarters. Even such, the trend is likely to remain fairly tame, and not pose much threat to inflation, especially given the rebound in productivity. Indeed, productivity leaped 3.6% in the first quarter, which was the strongest gain since Q3-2014. Productivity is expected to moderate in coming quarters, but will prevent gains in unit labor costs from driving inflation above the FOMC’s target. So, despite the labor market remaining tight, with inflation low we still expect the FOMC to refrain from raising this year.

With low inflation and the continued increase in payrolls and wages, real consumer spending looks to rebound from the 1.2% rate registered in the first quarter. Further, personal spending surged 0.9% in March; the largest one-month increase since 2009. Perhaps of more consequence, the bump in March spending gives PCE momentum headed into the second quarter, and likely puts to bed any lingering worries of a prolonged retrenchment in spending, which was perhaps suggested by the still-curious drop in December spending.

U.S. Outlook

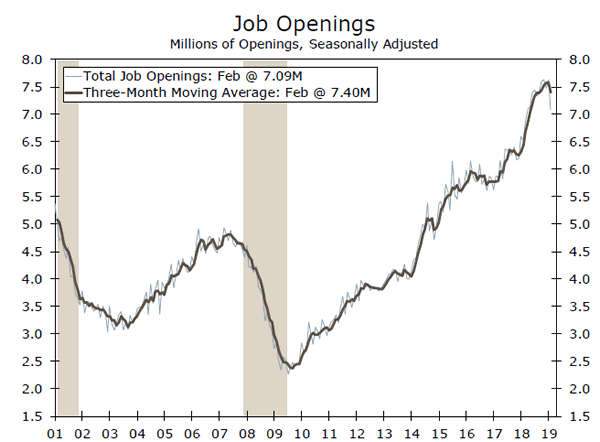

JOLTS • Tuesday

As recently as November of last year, the number of job openings was riding high, comfortably north of 7.5 million jobs and setting a new record. However, the number of available jobs has slowed since then with 7.09 million job openings reported in February.

When March numbers are released on Tuesday, there are mixed signals for what to expect. This week’s consumer confidence report showed that consumers’ impression of jobs being plentiful rose more than 4 percentage points in April after slipping a few points in March. The JOLTS report is for March, so it is unclear whether or not we will see the improvement reflected here. Weekly jobless claims figures have been spotty as well and offer no firm signal.

The labor market is still historically tight, but questions have arisen in recent weeks about a potential loss of momentum. The JOLTS report will provide the latest data points to consider that debate.

Previous: 7.09M Consensus: 7.35M

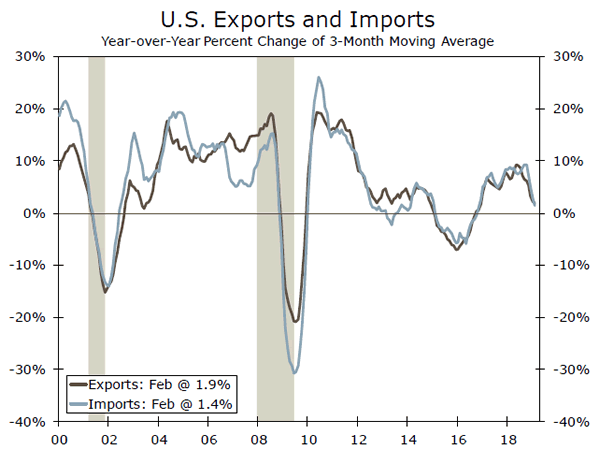

International Trade • Thursday

Trade added a full percentage point to GDP growth in Q1. In four out of the five prior quarters, trade was a net drag on the economy. The BEA has to estimate the March trade numbers in its advance GDP estimate, so when the actual trade figures for March print on Thursday of next week we will get a sense of how close those estimates came. We expect to see a modest widening in the trade deficit for March.

As the nearby chart shows, both import and export growth have been slowing on trend since the expansion of trade tariffs went into effect late last year. This has occurred alongside a drying up in global trade that has pulled global export volume growth into negative territory, a key factor identified by the IMF in its most dour forecast for global GDP growth since the global recession.

Previous:-$49.4B Wells Fargo: -$51.3B Consensus: -$51.2B

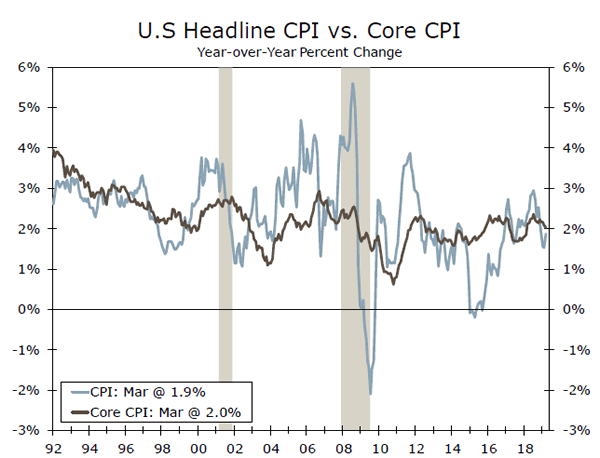

CPI • Friday

After raising rates four times last year and despite having guided expectations toward further rate hikes in 2019, the Fed pivoted and, citing a need for patience, opted to sit on hold so far this year and has even played down expectation, for any rate hike this year.

The Fed’s shift can be explained, at least in part, by the deterioration in the inflation numbers. A recent example: we learned earlier this week that the PCE deflator came in at just 1.5% year-over-year and the core deflator came in at 1.7%, which was below already modest expectations.

The CPI measure, which takes a basket-of-goods approach as opposed to actual spending, has been running a little hotter. On Friday of next week, we get the latest read on CPI inflation and expect to see both headline and core come in at 2.1% year-over-year.

Previous: 1.9% Wells Fargo: 2.1% Consensus: 2.1% (Year-over-Year)

Global Review

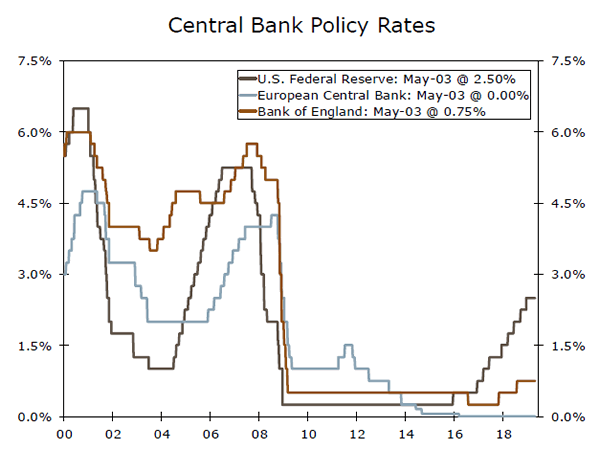

ECB and BoE Likely Still on Hold

- Eurozone GDP rebounded in Q1, with the broader European economy avoiding recession and showing some improvement, while U.K. PMIs experienced slight declines. Despite improved data, we believe the Eurozone is not out of the woods yet and the ECB is on hold for now, while the Bank of England may look to hike rates if an orderly Brexit materializes.

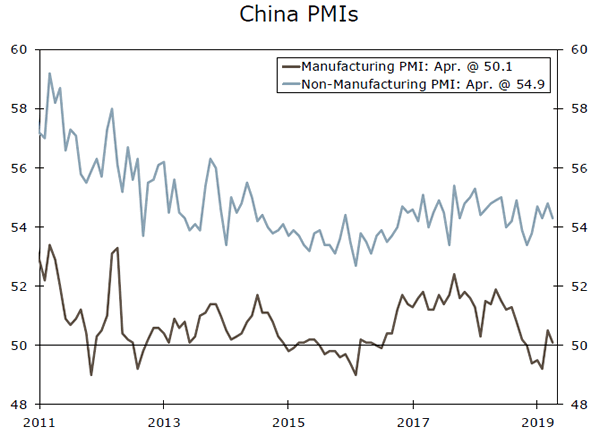

- Chinese PMIs experienced a slight decline in April, although manufacturing and non-manufacturing PMIs remain in expansion territory. We expect the economy to gradually slow; however, additional stimulus measures and a potential trade deal with the U.S. will likely help China avoid a hard landing.

Eurozone Economy Shows Some Stability

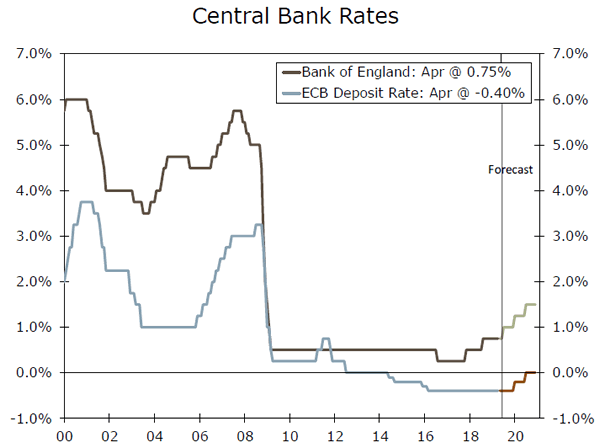

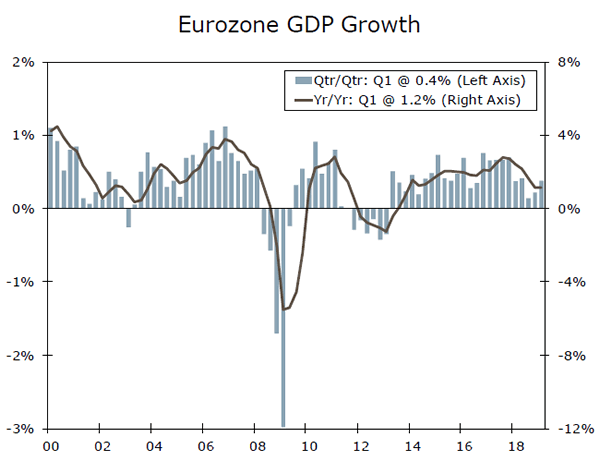

GDP growth in the Eurozone outperformed expectations this week, with the broader European economy steering away from recession. Q1 data revealed the Eurozone grew 0.4% quarter-over-quarter, higher than consensus forecast of 0.3%. This week’s data provided markets with some optimism for ongoing growth across Europe, as Italy officially exited technical recession, while Spanish GDP growth firmed to 0.7%. Also contributing to the improved sentiment was the final Eurozone manufacturing PMI for April, which was revised slightly higher, while Germany, Spain and Italian manufacturing PMIs all improved. Despite improved GDP and sentiment data, we still believe it is too early to call for a turn to robust growth for the European economy. While the manufacturing PMI recovered in April, it still remains in contraction territory. We continue to believe the ECB will keep policy rates on hold until a stronger recovery starts to materialize, and will eventually look to hike rates starting in Q1-2020.

U.K. Economy Resilient Despite Brexit Headwinds

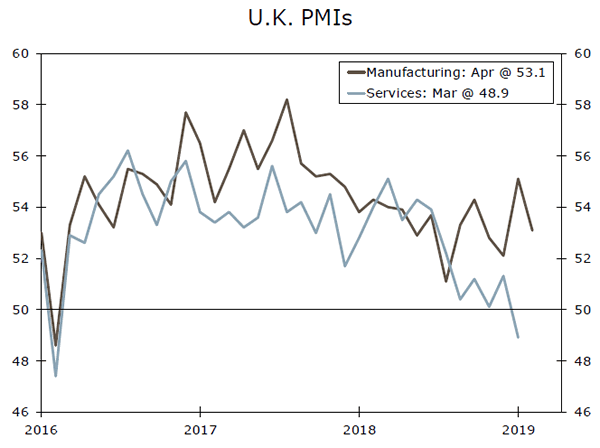

Sentiment data in the United Kingdom were also released this week, with the April manufacturing PMI falling to 53.1, down from 55.1 in March. The decline in the manufacturing PMI was largely expected, and we believe the U.K. economy will remain resilient despite the challenges that Brexit presents. As of now, we think the U.K. economy will grow around 1.3% in 2019, and given our view for a Brexit deal to eventually be made and uncertainty to be lifted off the U.K. economy, we see a pickup in growth heading into 2020. The Bank of England (BoE) reflected this view at its meeting this week, raising its GDP forecasts for this year as well as in 2020. Although citing a “no-deal” Brexit as still a possibility, BoE policymakers also suggested that interest rates would likely need to be raised more than markets are currently anticipating if a smooth Brexit were to occur. As of now, markets are currently pricing around one full 25 bps rate hike over the next 24 months. We share a similar perspective and maintain our view that the BoE will begin to hike rates after a Brexit deal is agreed upon (likely by Q4 of this year), with the first rate hike likely to come in early 2020.

Stimulus Measures Likely to Support China’s Economy

China PMIs were weaker than expected in April, with the official manufacturing PMI falling to 50.1, while the Caixin manufacturing PMI unexpectedly softened to 50.2. The services PMI also declined unexpectedly in April, falling to 54.3; however, it remains comfortably in expansion territory. Despite the weaker-thanexpected PMIs, we continue to believe the slowdown in China’s economy will be gradual. Chinese authorities continue to suggest that additional stimulus measures may be introduced into the economy, while some economic activity data indicate current stimulus efforts may be starting to have an effect on the economy. While the prospects for a long-term trade deal between China and the United States remain encouraging overall, recent headlines have been slightly mixed. A trade deal, along with additional stimulus, would likely stabilize China’s economy and keep GDP growth above 6% for the time being. As of now, we forecast GDP in China to grow at 6.2% in 2019 and to slow slightly to 6.0% in 2020.

Global Outlook

Reserve Bank of Australia • Tuesday

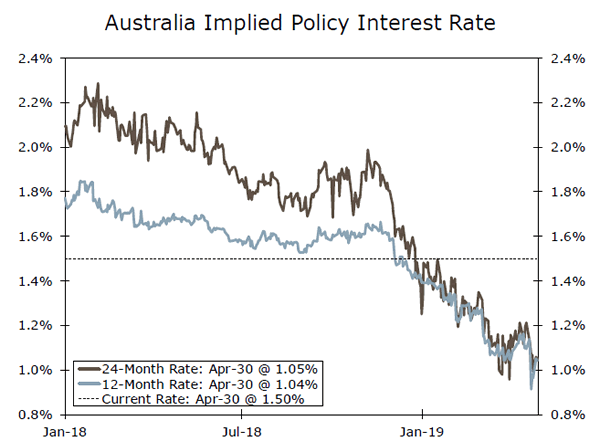

The Reserve Bank of Australia (RBA) will meet next week to make its latest monetary policy assessment. Australian economic data have been relatively soft as of late, with a deteriorating domestic housing market weighing on the country’s growth prospects. Recent CPI inflation data reflect the slowdown as well, with the Q1 CPI softening to 1.3% year-over-year, much lower than the consensus forecast, and a sharp slowdown from Q4. The Reserve Bank of Australia has noted the deceleration in the economy, with recent commentary more dovish than markets had expected. A weaker-than-expected inflation print will likely result in additional dovish statements from the RBA, while we will be focused on any indications that downside risks to the outlook are increasing. A rate cut at next week’s meeting is viewed as likely, with markets currently pricing in two policy rate cuts over the next 24 months.

Previous: 1.50% Consensus: 1.25%

Reserve Bank of New Zealand • Wednesday

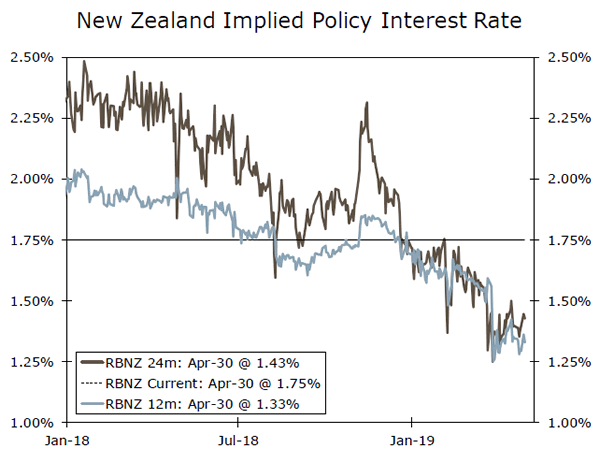

New Zealand’s economy has underperformed recently, with the most recent evidence being this week’s softer-than-expected labor market data. Despite the Q1 jobless rate falling to 4.2%, employment data were much weaker than forecast, declining 0.2% quarter-overquarter, while wage growth slowed as well. In response to a weaker economic outlook, the Reserve Bank of New Zealand (RBNZ) has turned more dovish, explicitly stating at its March meeting that the likely direction for the next Official Cash Rate move would probably be down. This week’s soft labor market data likely reinforce this bias, with markets currently expecting the RBNZ to eventually ease monetary policy as well. As of now, markets are implying about two interest rate cuts from the RBNZ over the next 12-24 months. We view a rate cut at next week’s meeting to be likely, while the consensus leans toward the central bank moving forward with a rate cut as well.

Previous: 1.75% Consensus: 1.50%

Mexico CPI Inflation • Friday

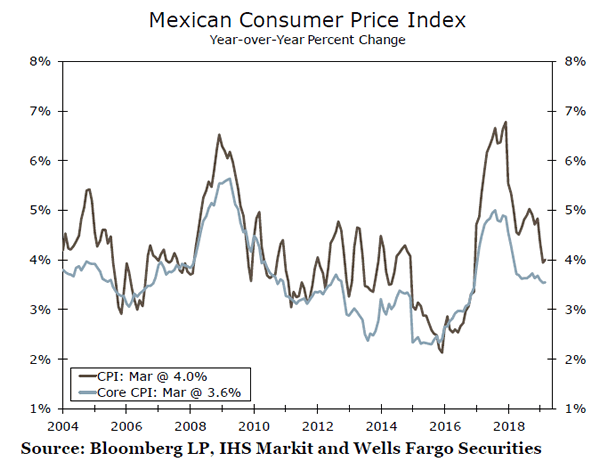

Since early 2018, CPI inflation in Mexico has been on a downward trajectory. This has primarily been a result of significant policy rate hikes from the Central Bank of Mexico, a trendless currency and relatively subdued oil prices. The economic conditions that resulted in lower inflation may start to turn, however, as the central bank is on hold for now and oil prices have moved higher. Given this, we think CPI inflation may finally start to move higher as well. In addition, the deceleration in Mexico’s economy should provide the central bank with some scope to start cutting interest rates, which might also boost inflation over time. We also expect the peso to gradually weaken, which should contribute to inflationary pressures, while we think geopolitical tensions that should pull some excess oil supply out of the market could potentially boost oil prices further. For April, we expect CPI inflation to quicken up to around 4.4% year-over-year.

Previous: 4.0% Wells Fargo: 4.4% (Year-over-Year)

Point of View

Interest Rate Watch

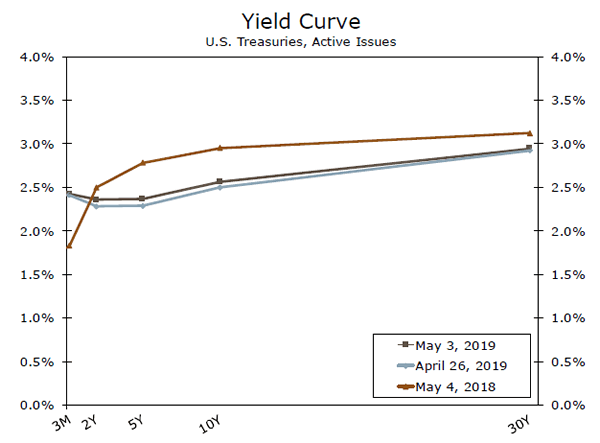

The FOMC Is Still Patient

As expected, the FOMC left the fed funds rate unchanged at its meeting this week. The committee appeared less concerned about growth than it did at its March meeting. The statement characterized GDP growth as “solid” once again, while Chair Powell expected business investment and consumer spending to bounce back in Q2, supporting “healthy GDP” growth this year.

Less upbeat in the statement was the FOMC’s read on inflation following a dip in core PCE inflation and continued weakness in inflation expectations. With inflation still flagging, the FOMC maintained its pledge to be “patient” with future adjustments to policy.

The recent slowdown in inflation has been viewed as a potential reason the FOMC may cut rates in upcoming months even as risks surrounding the growth outlook, like trade policy and a slowdown abroad, had subsided. Heading into this week’s meeting, markets had priced in about a 50/50 chance of a rate cut by the FOMC’s September 18 meeting.

Powell pushed back on the weakness in inflation, emphasizing “transient” factors as the reason for the slowdown. We agree to a large extent and discuss those factors in more detail in our Topic of the Week on the next page. With Powell indicating that he does not believe the weakness is likely to persist, and that “we don’t see a strong case for a rate move in either direction,” market expectations for a rate cut have been pared back. A 50/50 probability is not priced in until the December 11 meeting now.

However, yet again, inflation is missing to the downside of the FOMC’s “symmetric” target. Moreover, other committee members have expressed more concern about the persistent shortfall.

We see low inflation as the key reason the FOMC is likely to refrain from raising rates the rest of this year and the first half of 2020. But a rate cut this year continues to look premature, in our view. Not only is recent softness in core PCE inflation somewhat exaggerated, but financial conditions have eased considerably since the start of year, and should continue to support above-trend growth.

Credit Market Insights

Not That Kind of Cut

At its meeting this week, the FOMC announced a 5 bps cut to the interest on excess reserves (IOER) rate, yet Chair Powell made sure to emphasize that this was merely a “small technical adjustment” that should not imply any monetary policy loosening on behalf of the FOMC. The IOER, which the Fed pays to depository institutions on the excess reserves they hold at the central bank, had previously functioned as the ceiling of the fed funds target range. However, the effective fed funds rate—or the actual, marketdetermined rate on overnight interbank loans—has recently drifted up toward the top of the FOMC’s 25 bps target range for the fed funds rate, and has in fact been above the IOER for the past month. To bring the effective fed funds rate under greater control within the intended range, the FOMC has now thrice tweaked the IOER, with this week marking the first adjustment without any accompanying change to the fed funds target range. By reducing the incentive for banks to park funds at the Fed, a lower IOER thereby increases the supply of loanable overnight funds, easing upward pressure on the effective fed funds rate and helping to keep it within its intended range. We view this merely as a technical adjustment that should keep the effective fed funds rate closer to the midpoint of its target range as the Fed remains on hold. However, as we have previously written, it further raises the prospect of a reconfiguration of the Fed’s monetary policy toolkit in a post-Great Recession world.

Topic of the Week

How “Transient” Is the Slowdown in Inflation?

The FOMC’s preferred measure of trend inflation, the PCE deflator ex-food and energy, slipped further below the Fed’s 2% target in March, easing to 1.6% on a yearago basis. Federal Reserve Chair Jerome Powell, however, downplayed the recent easing in core inflation in his post-FOMC meeting press conference this week.

Powell characterized the recent softness as “transient,” and we agree that the weakness in inflation since the start of the year is exaggerated relative to the trend. In January, the cost of “portfolio management and investment advice” tumbled 4.6%, which was enough to shave off almost a full tenth from the core index. This is an imputed measure tied heavily, albeit with a lag, to changes in equity markets which are now at fresh highs. In addition, a new methodology was introduced for collecting prices at department stores in March, which contributed to the largest ever one-month decline in apparel prices.

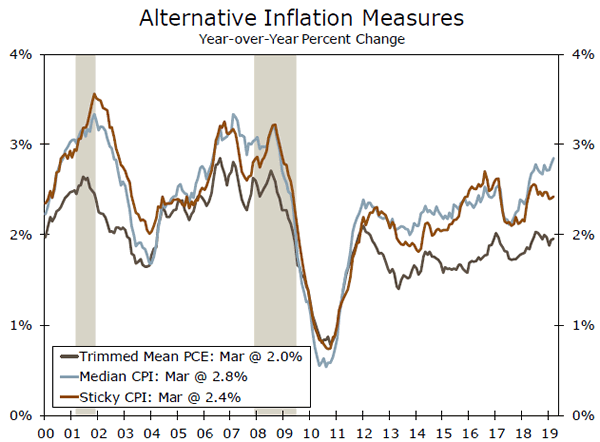

Alternative measures show the trend in inflation holding up better. Powell cited the Dallas Fed’s Trimmed Mean PCE deflator, which currently sits at 2.0%. In the Trimmed Mean PCE, items are sorted based on their monthly price change, with items at the tails of the distribution thrown out. Unlike a traditional “core” index, food and energy can therefore be included if monthly changes are moderate. The Atlanta Fed’s Sticky CPI has also been steady in recent months. The index captures items that do not change prices frequently and therefore helps filter out the “noise” of recent moves. Meanwhile, the median price change within the CPI has strengthened.

The resilience of the alternative inflation indexes suggests the slowdown in the core PCE deflator overstates recent weakness in inflation. Nevertheless, inflation continues to come up short of the FOMC’s target. Although likely to edge back up in the coming months, we do not expect the core PCE deflator to re-visit 2.o% this year. Even as the labor market continues to tighten, the pickup in productivity growth has kept inflation pressures muted, while historically low inflation expectations point to price changes remaining modest.