{kind=link}

U.S. Highlights

- Apart from vehicle sales, recent data paint a positive narrative for consumer-related industries at the start of spring. Real consumer spending and pending home sales surged in March, while consumer confidence improved in April.

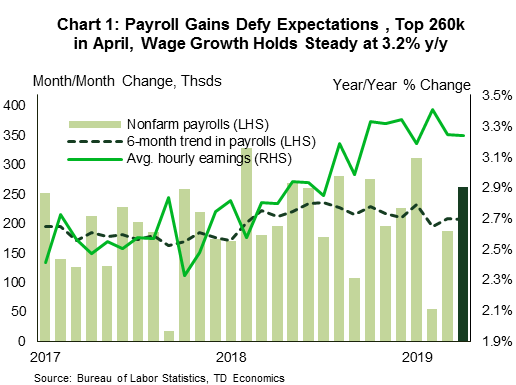

- Payrolls were up 263k in April, much better than expected; wage growth held steady at 3.2% y/y and the unemployment rate fell to a near-50 year low of 3.6%. A drop in the labor force participation rate assisted the latter.

- The Fed held rates steady this week, with an emphasis put on inflation running below target. But in the press conference, Fed Chair Powell noted that inflation was driven down by “transient” factors, adding that there is no strong case “for moving in either direction”. Indeed, for now, all of the tea leaves suggest that the Fed will remain on hold for some time.

Canadian Highlights

- It was a soft week for Canadian markets, partially reflecting a generally lackluster view on near-term economic prospects.

- This was confirmed in the data. Economic activity pulled back in February, setting the economy up for another soft quarterly expansion to start 2019.

- Early data for the second quarter also points to softness, with April auto sales falling month-on-month for the first time in three months alongside a weak PMI report. Growth acceleration still appears likely, but it now looks more like another sub-trend performance is in store.

U.S. – Inflation Undershoots, Jobs Overshoot, Fed Stays Put

It was a busy week for those keeping a careful watch on the U.S. economy. A volley of first-tier economic data and an FOMC rate decision took center stage, while trade developments reverberated in the background.

While the consumer had a soft showing overall in the first quarter, a two-month data dump this week provided added detail on recent momentum. Real consumer spending was flat in February, before surging 0.7% in March. This spending upswing points to consumers shaking off the adverse effects of the prolonged government shutdown, and provides a solid handoff to consumption in the second-quarter.

The (mostly) positive narrative on consumer-related industries at the start of spring was further bolstered by a 3.8% m/m surge in pending home sales in March and a pickup in consumer confidence in April. The former leads existing home sales by 1-2 months, and points to further stabilization in the housing market. However, vehicle sales were disappointing, falling 6% m/m in April to 16.4M units. Despite this, overall consumer spending is still tracking a 3% annualized pace in the second quarter, a sharp acceleration from the 1.2% clip in the first quarter. This will provide support to overall economic activity as other temporary factors that boosted growth in the first quarter fall off.

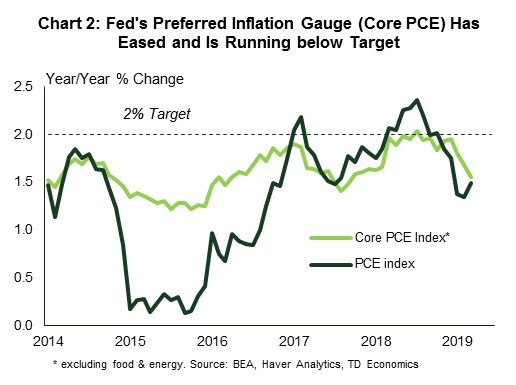

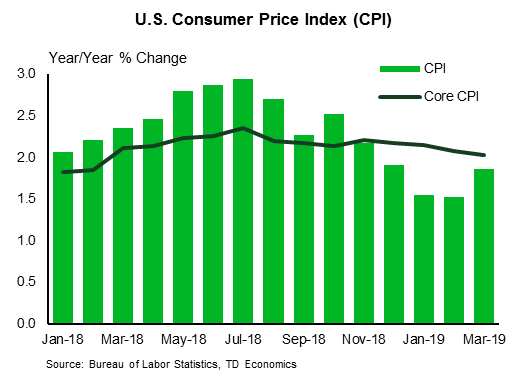

Healthy consumer spending is being supported by a strong labor market. Payrolls rose 263k in April, beating expectations (190k) once again (Chart 1). The jobless rate moved down to a near-50 year low of 3.6%. However, that was driven by a disappointing decline in the labor force participation rate. Wage growth held steady at 3.2% y/y. But with softer inflation (see Chart 2), wage gains look even better in real terms. Given the current tightness, we expect wage pressures to remain, but job gains to slow to a more sustainable sub-150k per month through the remainder of 2019.

Rounding out the April data reports were the ISM indices. Both moderated on the month but continue to hover around the 55-point mark, which is in tune with the broader narrative of slower, but still decent, growth this year.

With the labor market and economic growth not looking too shabby, inflation remains the Fed’s key concern and main reason for holding rates steady, as it did this week. The FOMC statement emphasized that inflation has run below target. But in the press conference, Fed Chair Powell noted that inflation was driven down by “transient” factors, adding that there is currently no strong case “for moving in either direction”. We agree with the Fed’s assessment. Given that inflation has persistently undershot the Fed’s target, it would take a notable acceleration in price pressures to push the Fed to hike. We do not expect inflation to accelerate that quickly, and all of the latest data support our view that the Fed is likely to remain on hold for quite some time.

Canada – Slump Prolonged

It was something of a down week for Canadian markets. The S&P/TSX composite index fell gradually through the week, while the loonie, despite some mid-week swings, looks set to end the week close to where it began. In oil markets, the benchmark WTI contract fell roughly US$2 per barrel to $61, within the range that we expect to persist for the next while. From a Canadian oil perspective, we look for the heavy oil discount to widen somewhat, consistent with the economics of crude by rail, which, for the time being, seems like the only game in town for getting a marginal barrel of oil to market. This will have a modestly negative impact on revenues, but should help clear out still sizeable inventories.

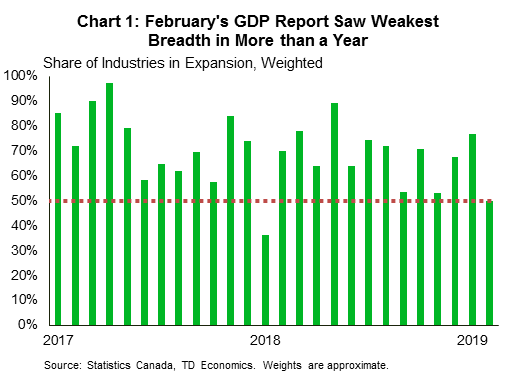

On the data front, the main event this week was monthly GDP, which came in below market expectations for a flat print, contracting by 0.1% month-on-month (See commentary). Weather was partially to blame, causing issues in the transportation and real-estate sectors, among others, but doesn’t explain all of the weakness. Mining activity dropped again, and the broader mining, quarrying, oil & gas sector is now down 5% year-on-year. The breadth of the pullback was best evidenced by the share of growing industries hitting its lowest level in more than a year (Chart 1).

The GDP data appears to confirm what we’d been suspecting: that the Canadian economy likely again struggled to eke out growth at the start of the year. We now track first quarter growth at 0.6% q/q, annualized, just a bit above the Bank of Canada’s 0.3% view. If there is a silver lining, it is that some of the details look decent, with signs of life in investment after a disappointing 2018. Nevertheless, with the first half of the year shaping up to come in soft, the Bank of Canada’s more dovish turn seems appropriate.

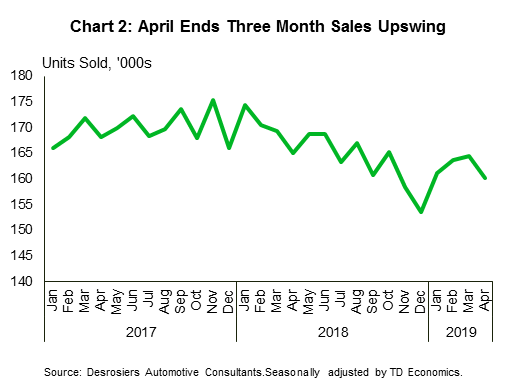

More signs of first-half softness were evident in the very early indicators for the second quarter. Canadians bought fewer cars in April, once seasonal variation is taken into account (Chart 2). The three-month upswing we saw at the start of the year has come to an end, and the level of sales now sits more or less in line with the downtrend that began last year. To be sure, this data can be noisy, so we shouldn’t read too much into a single month, but it hardly provides a positive start to the second quarter.

Other, relatively second-tier data also indicated softness. April housing resale activity in Vancouver fell 29.1% year-on-year, with the benchmark price dropping 8.5%, and the Markit Manufacturing Purchasing Managers Index (PMI) fell below the 50 ‘no-change’ mark for the first time since early 2016 on weak details. We won’t get too carried away with this data – it is worth noting that despite soft housing markets (resale activity fell 32% last year), British Columbia’s economy overall turned in an impressively strong growth performance last year, expanding 2.4% on fairly broad-based strength. All this is to say that some of the challenges facing the Canadian economy are unlikely to be resolved quickly, so expect the subpar performance to continue for a bit longer – it’s a slow slog back home.

U.S.: Upcoming Key Economic Releases

U.S. Consumer Price Index – April

Release Date: May 10, 2019

Previous: 0.4% m/m; core 0.1% m/m

TD Forecast: 0.4% m/m; core 0.2% m/m

Consensus: 0.4% m/m; core 0.2% m/m

We look for headline CPI to pick up two tenths to 2.1% in April on the back of a strong 0.4% seasonally-adjusted monthly increase. The main driver behind the monthly gain is another sizable jump in gasoline prices (+10.2% m/m). Furthermore, we anticipate core CPI inflation to register another “soft” 0.2% m/m gain (2.1% y/y), as a firm 0.2% increase in core services prices will likely offset a third consecutive monthly decline in prices in the core goods segment (which we pencil in at -0.1% m/m). We expect OER to remain largely steady at 0.3% m/m and for the ex-shelter segment to improve marginally on a monthly basis.

Canada: Upcoming Key Economic Releases

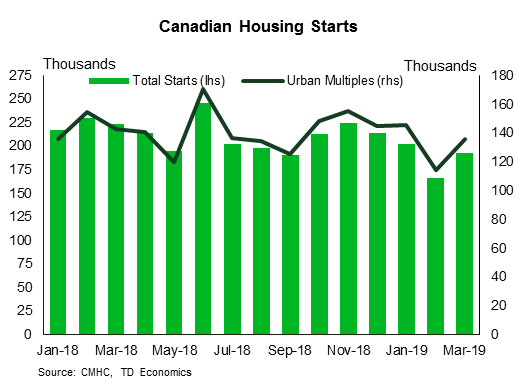

Canadian Housing Starts – April

Release Date: May 8, 2019

Previous: 192.5k

TD Forecast: 197k

Consensus: N/A

TD looks for housing starts to rise to a 197k pace in April on pickup in both single and multi-unit construction. Permit issuance for single family homes has started to recover from post-crisis lows, suggesting some more upside to construction activity after starts registered their first increase since November last month. We also see scope for further gains in multi-unit starts even after a 20% rebound last month; multi-unit urban starts remain well off their peak from mid-2018 and while we are unlikely to retest such levels anytime soon, low vacancy rates and affordability constraints continue to underpin demand for apartment units.

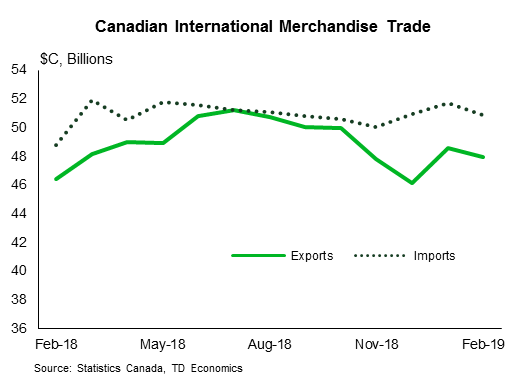

Canadian International Trade – March

Release Date: May 9, 2019

Previous: -$2.90bn

TD Forecast: -$2.30bn

Consensus: N/A

TD looks for the merchandise trade deficit to narrow to $2.3bn in March, helped by a further recovery in crude oil prices and a rebound in non-energy exports following the broad pullback last month. Adjusted to Canadian dollars, WTI prices rose by 7% in March while WCS prices rose by 12%. However, energy export volumes will be challenged by tight WCS spreads which continued to hold near $10 throughout the month, a level that discourages rail shipments while pipelines continue to operate at full capacity. We also expect a broad recovery in non-energy exports from March although forestry products should remain under pressure due to continued weakness in residential construction south of the border. Stronger exports should be partially offset by a pickup in import activity while real export growth will come in well below the nominal advance due to higher industrial prices.

Canadian Employment – April

Release Date: May 10, 2019

Previous: -7.2k, unemployment rate: 5.9%,

TD Forecast: -10k, unemployment rate: 5.9%

Consensus: N/A

TD looks for the economy to give back 10k jobs during month of April, which will help nudge the pace lower after averaging 36k for the six months through March. We have argued that recent labour market gains are unwarranted by current economic backdrop, and while it is difficult to predict the timing of a giveback, we think this tilts the risks towards a soft print. Full-time employment should drive the pullback, which will add to the downbeat tone of the report, while the goods-producing sector should account for most of the jobs lost during the month with manufacturing in the spotlight after Markit PMI tipped into contractionary territory for the first time in three years. Job losses of 10k should see the unemployment rate edge higher to 5.9% assuming modest labour force growth while we expect wage growth to hold at 2.3% y/y.