{kind=link}

The widely expected US Nonfarm payrolls report is coming out on Friday at 1230 GMT to direct markets over the path of interest rates as this week’s comments by the Fed chairman, Jerome Powell, did not convince investors that the central bank’s next move is going to be a rate cut.

Following the Federal Open Market Committee (FOMC) policy meeting which left interest rates unchanged on Wednesday, Powell surprisingly claimed at his press conference that the factors behind recent inflationary weakness are “transitory” and therefore the case for a rate cut is not as strong as previously. While some analysts have taken on board this message, the majority continue to believe that borrowing costs could ease by the end of the year, with all eyes turning now to the government’s comprehensive employment data for the month of April for extra clues on whether the Fed could soon change its guidance again.

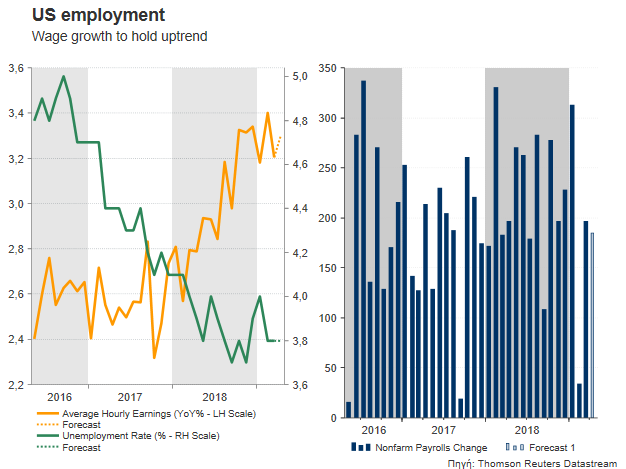

Average hourly earnings are what markets will look at first as any improvement in the wage growth would theoretically translate into higher consumer spending and therefore stronger inflationary pressures. Indeed, forecasts suggest that wage growth rose from 0.1% to 0.3% on a monthly basis in April, driving the yearly gauge slightly up to 3.3% versus 3.2% seen in March. Even though the yearly measure is still under the decade-high of 3.4% reached in January, investors may not get too worried as long as the unemployment rate holds around the 18-year low of 3.8%, indicating a tight labor market. Nonfarm payrolls, however, could be a bit bothersome if the figure drops from 196k to 185k, especially after the ISM survey for the growth-driving manufacturing sector indicated that job creation in the industry remained weak in April after a plunge in March.

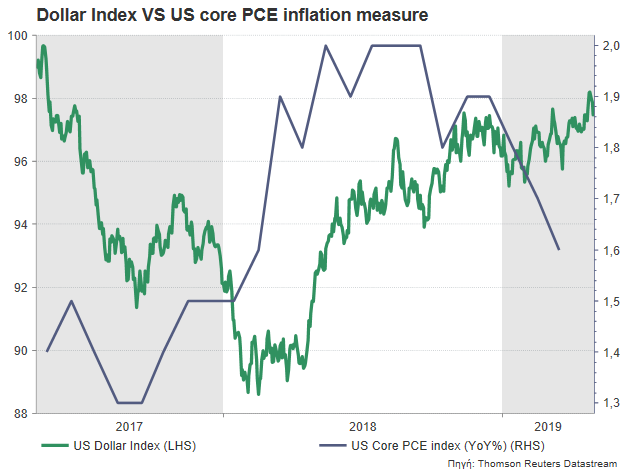

Overall the US labor market is still in good shape and consumption seems to be promising given the recent upbeat data on personal consumption and retail sales. Still, because of the down-trending inflation that has recently dropped further below the Fed’s 2.0% price target, policymakers have no incentive to resume rate hiking. The resilient dollar could be partially blamed for the low inflation. Protected by its safe-haven feature that offsets the negative effects from the US-Sino trade war, and supported by the economic weakness in Europe, the elevated dollar makes imported goods cheaper to US consumers, forcing domestic companies to lower their prices to mitigate competition from abroad. Of course, Trump’s tariffs maybe somewhat inflationary but at the same time they are damaging for businesses which import foreign components to complete an assembled product. Therefore, unless US inflation rebounds and the trade drama comes to an end, the Fed is not likely to push up interest rates.

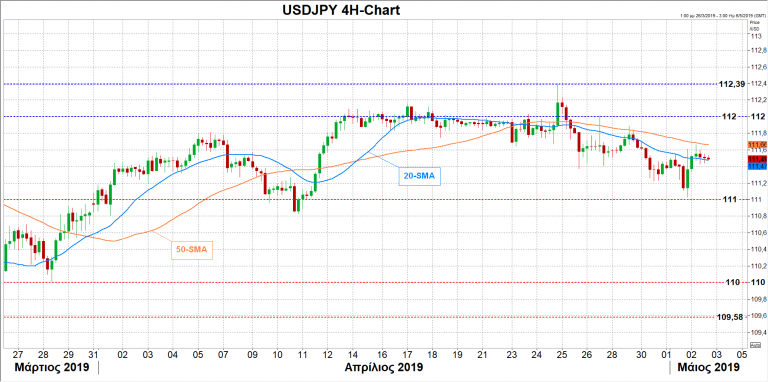

Consequently, the NFP report could bring temporary gains to the dollar if the data beat expectations as the world is still uncertain about the future of global growth, with USDJPY probably rallying to face strong resistance within the 112-112.39 area. Before that, the pair would have to overcome the 50-period simple moving average (SMA) at 111.66.

On the other hand, a miss in forecasts, especially on the wage front, could drive the pair as low as 111. The area between 110 and 109.58 could be a bigger challenge for the bears to overcome.