{kind=link}

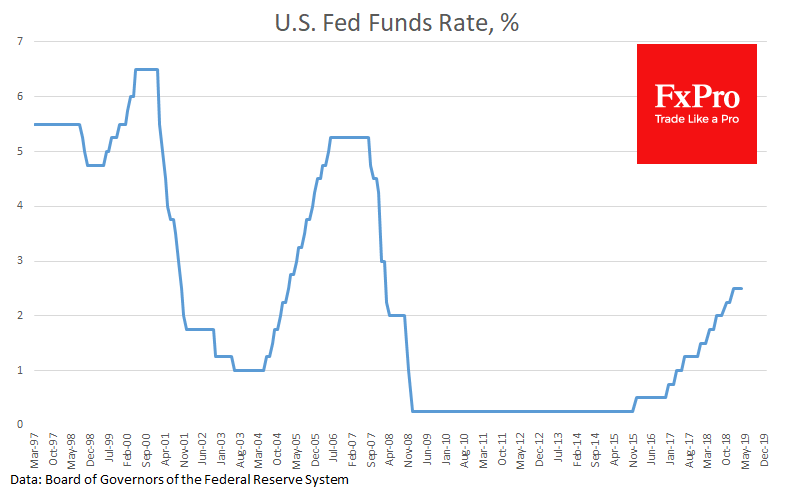

The upcoming FOMC announcement is in the focus of markets on Wednesday, having the maximum potential impact. US GDP showed an acceleration of growth to 3.2% but mainly due to the accumulation of stocks.

A trade deal between China and the United States has yet to be finished. The housing market is clearly stumbling on the road to growth. All the above are arguments in favor of maintaining a pause in monetary policy, which is the most anticipated market scenario. In the case of the implementation of less likely scenarios, we can see a sharper reaction.

The second option involves further rhetoric softening. The softness of the Fed helped US indices to add more than 20% since the end of last year, and could spur further growth. At the same time, it will be bad news for the dollar, which last week rose to 2-year highs.

It is unlikely but it cannot be completely ruled out that the Fed will try to cool the markets, noting that the US economy maintains healthy growth rates and that further rate hikes should be considered in the coming months. In this case, the stock markets risk getting severe hit, and the dollar can sharply turn to growth.

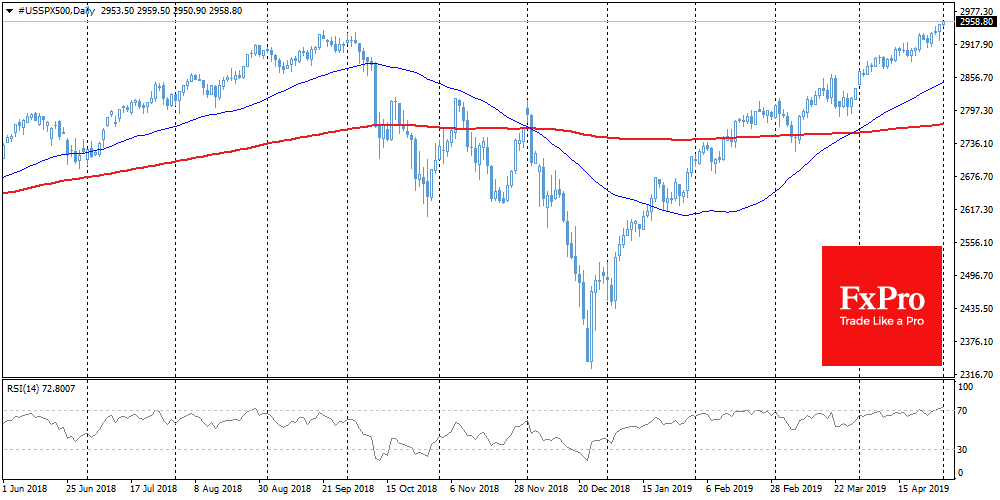

Speaking about stocks exchanges, strong reporting helped key US indices to go back to growth and update historic highs on the S&P 500 and Nasdaq. Data on a production activity and the labor market from ADP can affect this trend. The most dangerous is a sudden increase in the alertness of market participants since the initial desire to take profits risks turning into a serious correction.

Speaking about stocks exchanges, strong reporting helped key US indices to go back to growth and update historic highs on the S&P 500 and Nasdaq. Data on a production activity and the labor market from ADP can affect this trend. The most dangerous is a sudden increase in the alertness of market participants since the initial desire to take profits risks turning into a serious correction.