{kind=link}

The Bank of Canada (BoC) will announce its latest policy decision on Wednesday at 14:00 GMT. No action is expected, so all eyes will be on the accompanying statement, updated forecasts, and Governor Poloz’s tone. Markets seem to expect an overly dovish message, and while the Bank is indeed likely to appear cautious overall, it is unlikely to go as far as abandon its rate-hike plans completely – which generates an upside risk for the loonie.

The Canadian economy hit a soft patch in recent months, with wage growth slowing and house prices declining, which spells bad news for home-owning consumers. The BoC’s own business survey for Q1 was also downbeat, with the headline index dipping into negative territory, indicating that firms are growing pessimistic.

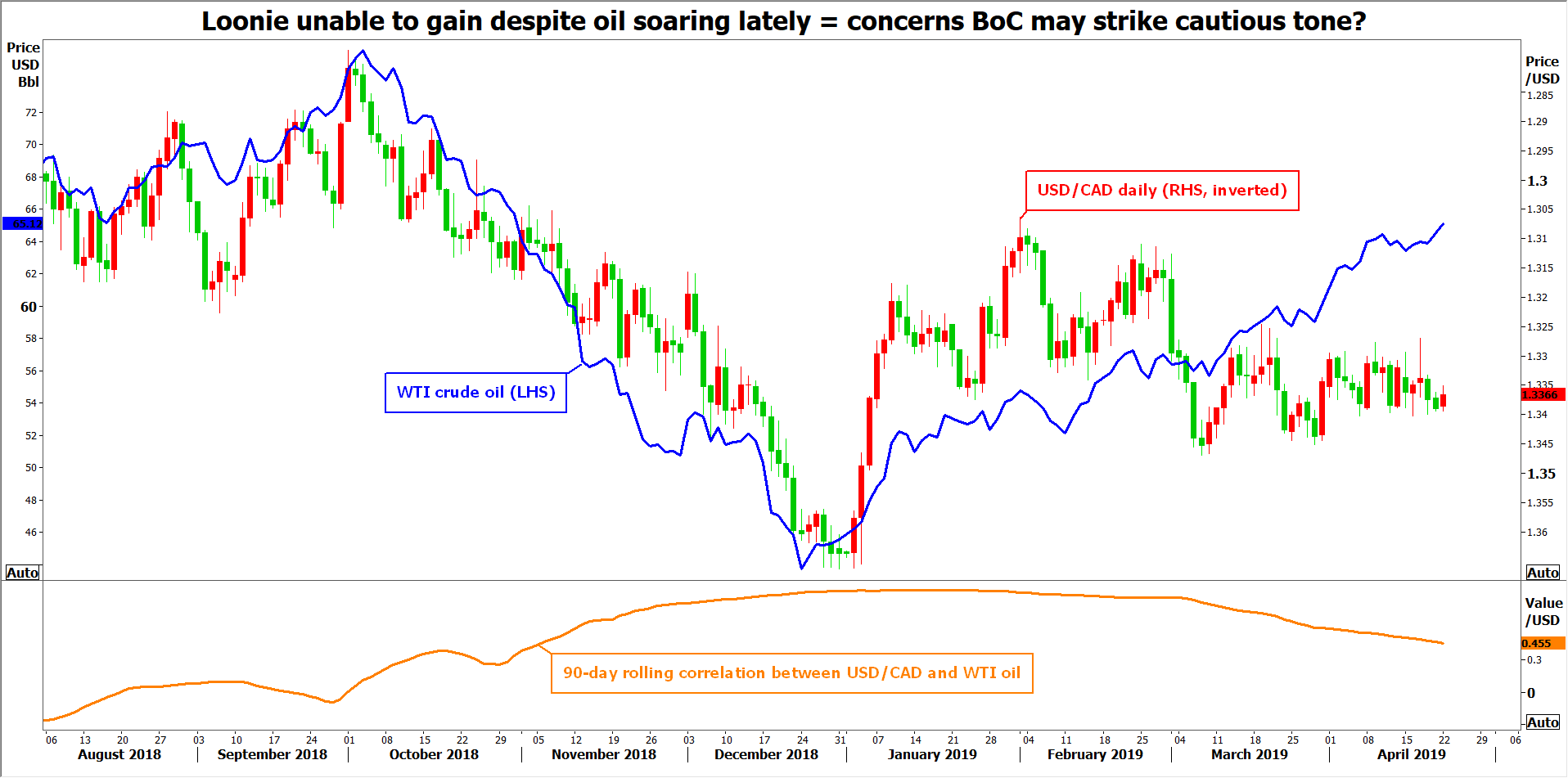

In this environment, market expectations for rate increases by the BoC evaporated, giving way to speculation for rate cuts. A quarter-point rate cut by December is now priced in with a ~30% probability. Yet, the loonie has been consolidating lately, trading sideways against the dollar as the gloom in the rates market was offset by a surge in oil prices – Canada’s biggest export.

This brings us to this week’s meeting. Markets seem to expect Poloz and his colleagues to strike a much more cautious tone, possibly by removing any surviving reference to rate hikes and effectively shifting to a neutral bias. Such a shift would probably reinforce expectations that the next move in rates will be lower, and potentially weigh on the loonie.

However, it may be too early for such a change. Policymakers are indeed likely to communicate a more cautious message, but it could be a touch less dovish than markets expect. They may not go as far as take rate hikes completely off the table. For one, the sustained surge in oil prices paints a much brighter picture for the nation’s energy sector. Meanwhile, the latest CPI data showed underlying inflation picking up, which provides a ray of hope. Separately, the officials already recalibrated their policy bias at the last meeting, so they may want to retain some optionality in case the economy does rebound, like the Fed has.

In brief, markets expect an overly-dovish BoC, and although recent developments haven’t been encouraging, they also haven’t been terrible enough to warrant another substantial shift in guidance. Perhaps more dovishness ‘on the edges’, but not abandoning hikes altogether.

As for the loonie, if this assessment proves accurate, the currency could soar. Not so much due to any massive change in the outlook for monetary policy but rather because with the risk of a dovish BoC out of the way, traders will have one less thing to worry about when adding to their long-loonie exposure, and the currency could finally play catch-up with the oil rally.

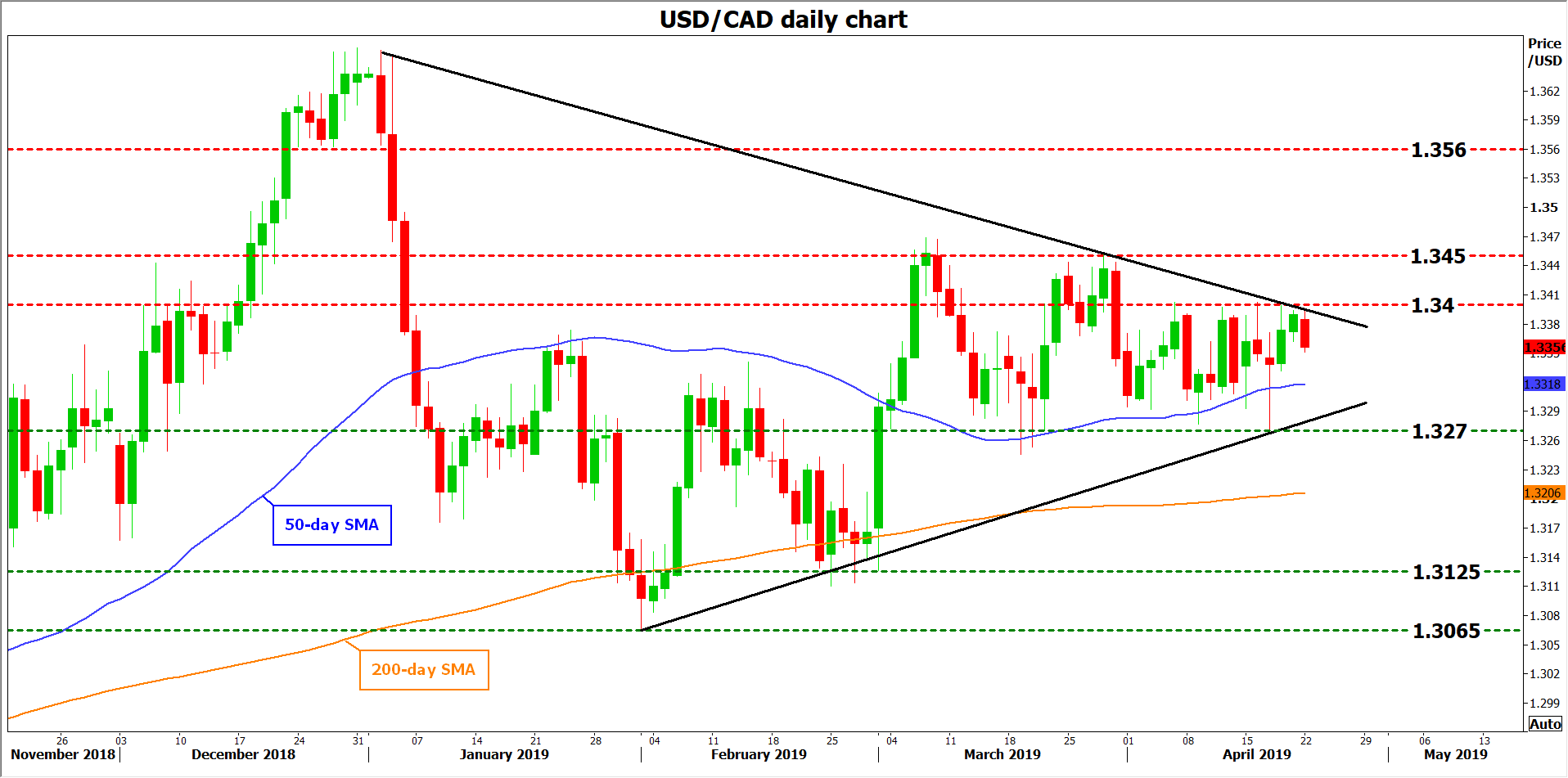

Technically, declines in dollar/loonie could encounter a first wave of support around 1.3270, marked by the April 17 low.

On the flipside, resistance to advances may come near 1.3400, a level that capped multiple bullish moves in April.