{kind=link}

- USD – Fed to detail end of QE and possibly inflation targeting

- Trade War – Deal could occur over next two months

- Brexit – May wants short delay

- Oil – Softer on China concerns

- Gold – Rising on tame inflation and trade deal uncertainty

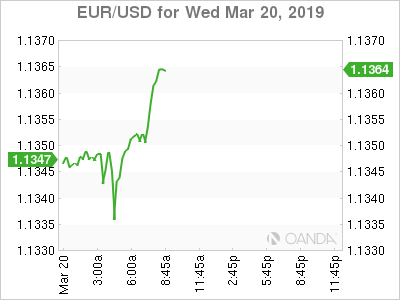

The conclusion of the two-day Fed meeting is expected to see no change with interest rates and confirm the dovish message instilled back in January. Today the Fed will provide clarity on their approach to patience, an update on their forecasts and projections, with many focusing on the dot plots, their ending of quantitative tightening and their approach to inflation.

Investors will primarily focus on the update of the dot plot forecast, which is expected to show 2019 rate hike expectations to fall from two raises to one. Some are expecting the Fed to bring down the forecast to no hikes, but that may be difficult as it would require 7 officials to downgrade their forecast. The 2020 forecast will be just as important, and we could see the Fed target one hike.

The Fed could also lower their economic projections, which could support their cautious tone. Many will pay close attention to their PCE inflation forecast as it could support the argument we are done with rate hikes if we do not see a clear path higher.

In addition to the dot plots, the Fed could end QT, or queue that for the next meeting. Just as important as the ending of the shrinking of the balance sheet, will be what is their plan on what type of debt they will hold, short term bills, or a combination with longer term bonds. Fed Chair Powell may also decide to adopt inflation targeting which would allow them to overshoot inflation.

For doves, the best-case scenario would be the Fed eliminating both hikes for 2019, announcing QT will end at this meeting or the next one, and the adoption of inflation targeting. With global headwinds, such as growth concerns, Brexit and the trade war still persisting, it might be difficult for the Fed at this meeting to come off hawkish, but they could since the market is overly pricing in a dovish meeting. If they keep hope alive for rate hikes over the next two years, we could see that take away some of the air in this recent risk-on rally.

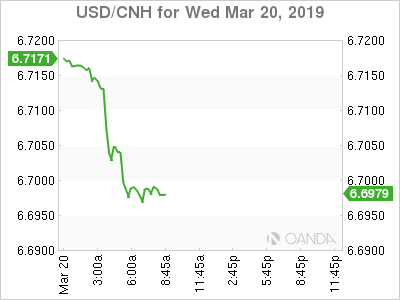

China

As we near what is expected to be a huge trade deal between the US and China, hurdles and final details will likely deliver many headlines that could raise concerns that talks may fall apart. US officials later commented that this was part of the normal process of negotiations. The market is overly pricing in a trade deal to be done over the next couple months, so it should come as no surprise that we will see stocks selloff when we see news that talks may be hitting roadblocks. Yesterday’s news that China is walking back some trade offers sent a reminder that a deal is still not done. The next step is for Us Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin to go to Beijing the week of March 25th.

Both sides remain motivated to get a deal done and we should see some framework agreement put in place over the next two months.

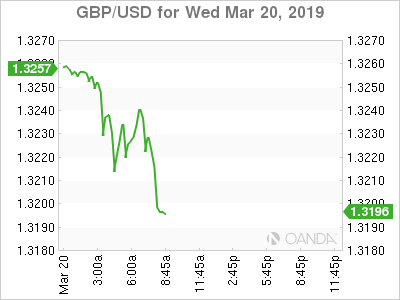

Brexit

Prime Minister May is running out of time, perhaps that is how she wants it. With nine days left to exit, she is seeking a short extension from the EU, that would give her one more chance to push a revised deal through Parliament. The risk is that if she fails after getting a short extension, we could see the UK go through a hard exit.

If we don’t see a deal by exit day, the UK will also need to decide if they will hold EU elections by mid-April, the problem is that if they don’t, they will exit from the block on July 1st with or without a deal.

The no-deal risks are rising and that is exactly how PM May wants it. She needs to scare her deal down Parliament’s throat and as we near these critical deadlines, she needs more leverage for the EU and her own Parliament.

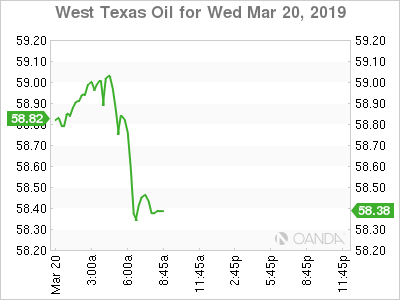

Oil

Crude prices pulled back from 4-month highs as global growth concerns returned as trade roadblocks were hit between the US and China. The markets are re-pricing their expectations for when we will see a final trade deal and that is important for Chinese demand for oil. The goals of mid-March deal are long gone and now the base case is for a deal to happen over the next two months. Oil still has some good catalysts for higher prices as we approach a key rise in demand from the US. The geopolitical risks and sanction effects are also helping keeping prices bid and we may see sellers come back in force once we see US stockpiles rise and OPEC compliance starts to wane.

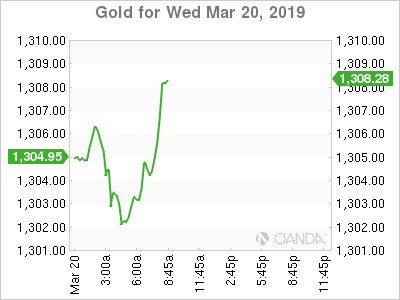

Gold

Gold is slightly lower ahead of the Fed but still above the $1,300 an ounce level. The precious metal took some time to rally after the Fed’s dovish pivot in January as investors were more focused on the potential trade deal between US and China. With the market heavily pricing in a trade deal, gold may be free to rally if we see dovishness confirmed by the Fed.