{kind=link}

- Fed decision at 18:00 GMT today; new rate projections to dictate market reaction

- Stocks pause rally as trade uncertainty reigns in

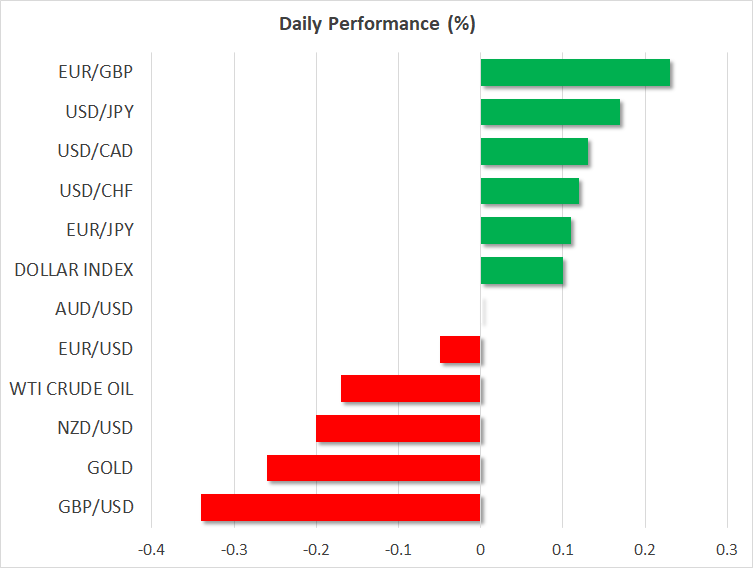

- Sterling inches down amid reports May will ask for short Brexit extension

Fed ‘dots’ to steal the show

The main event today will be the Fed policy decision at 18:00 GMT, which will be followed by a press conference from Chair Powell. No change in policy is expected, so all eyes will be on the updated forecasts for the US economy, Powell’s remarks, and most importantly, the new ‘dot plot’ with projections for the path of interest rates. The latest ‘dots’ back in December still pointed to two rate hikes in 2019, and while that is almost certain to be revised down given the Fed’s recent ‘patient’ pivot, the question is by how much they will be marked lower.

Namely, will policymakers keep even a single rate increase this year on the table, or will the median ‘dot’ be marked down more severely to indicate no hikes at all in 2019? On balance, the Fed may prefer to retain some optionality and keep another rate increase later this year in play, contingent on the economy rebounding. Simply put, it seems a little too early to completely abandon hikes at this stage. Since market pricing is now tilted towards rate cuts in 2019, a signal for even one hike could come as a ‘reality check’ for traders, boosting the dollar and weighing on equities. The opposite reactions would likely ensue in case the new ‘dots’ imply no hikes this year.

Equity rally takes a breather as trade doubts set in

US stock markets gave back some early gains to close practically unchanged on Tuesday, with sentiment taking a hit after media reports cast doubt on the narrative that the US-China trade talks are close to bearing fruit. China is seemingly walking back on some of its earlier pledges on key issues, because even after agreeing to American demands on intellectual property rights, US negotiators have not offered guarantees that the Trump tariffs will be lifted. On the bright side, Secretary Mnuchin and top US trade negotiator Lighthizer will travel to China next week, for another attempt to iron out a deal.

Taking a step back, optimism for an accord has been riding high for a while, which is combination with the ‘cautious’ shift by central banks has helped propel global markets much higher. To be fair, such optimism is well-founded because the US President seems thirsty for a deal, and ultimately that’s all that matters. That said though, the two sides still appear to be a ‘bridge too far’ on several issues, including the enforcement mechanism of any deal, so it wouldn’t be surprising to see the negotiations drag on for a while longer, before Trump ‘settles’ ahead of the 2020 elections.

Sterling pulls back as Brexit rollercoaster continues its wild ride

There’s never a boring moment in the Brexit saga, with headlines this morning suggesting PM May will only ask the EU for a short extension of Brexit until June. There’s good news and bad news here, for the pound. On the one hand, for May to request such a short delay, she must think there’s a good chance of her deal eventually passing. However, what happens if UK lawmakers don’t budge come summer? Another delay after that may be impossible for technical reasons, if the UK doesn’t participate in the upcoming EU Parliament elections.

To be frank, if May indeed asks for a short extension, that would drastically raise the risk of a no-deal happening by ‘accident’. Remember the main reason the pound rallied lately was due to the risk of a no-deal being perceived as fading, so if that market perception changes, then sterling buyers could be in short supply. Hence, in the immediate term, a short extension would likely hurt the pound, whereas a longer one could boost it, on expectations for a softer Brexit or another public vote going forward.

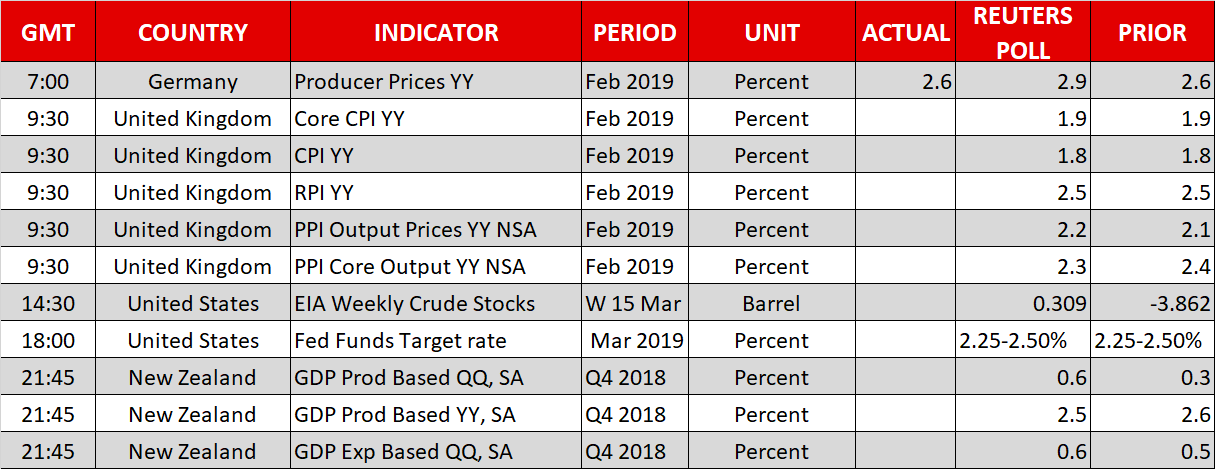

UK inflation data are due for release today, but market focus will likely remain mainly on Brexit.