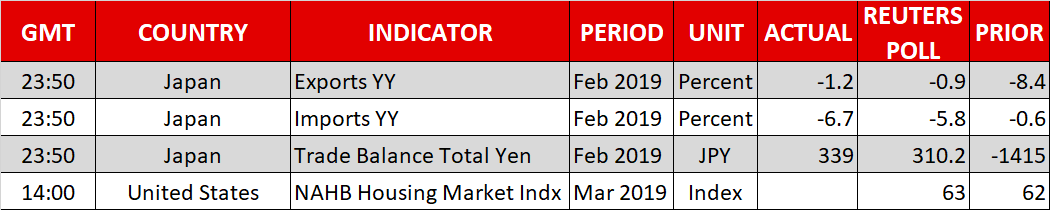

{kind=link}

- US stocks rally to six-month highs but perhaps on option expiries – implying some cause for caution

- Dollar retreats in a quiet session; looks to Fed meeting on Wednesday

- Sterling catches its breath ahead of potentially decisive week

US equities cruise to six-month highs on ‘quad witching’

In an otherwise quiet session, US stock markets rallied on Friday, with the benchmark S&P 500 (+0.50%) index breaking above a critical resistance zone around 2,820 that capped several rallies in recent months, to close at levels last seen in October. This, without any fresh catalyst or news. Second-tier US data released on the day were mixed, while incoming headlines were discouraging, with North Korea threatening to exit the nuclear talks and restart missile tests, for instance.

Indeed, considering also that US Treasury yields fell across the maturity spectrum, something typically associated with risk aversion, it seems the upbeat mood in stocks may have been owed mainly to positioning adjustments. Namely, Friday was a ‘quadruple witching’ day, where futures and options on stocks and indices all expire, often leading funds and money managers to recalibrate their exposure to equities. Hence, major moves can occur almost solely on flows, which implies some cause for caution as technical breaks recorded on such sessions – like the S&P’s – may not necessarily reflect investor sentiment, but rather some ‘forced’ rebalancing.

In this sense, the real test for the S&P 500 may be whether it can remain above the key 2820 area today, when things are back to ‘normal’.

Softer dollar, but otherwise all quiet in FX as traders await key events

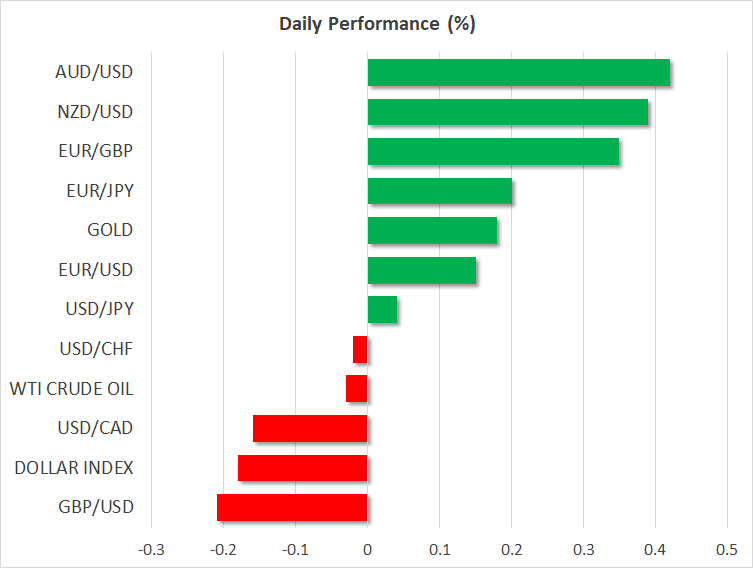

In the currency market, there wasn’t anything standout, with most pairs remaining confined in relatively narrow ranges. The exception to this pattern was the US dollar, which surrendered ground against a basket of six major currencies on Friday and continues to retreat early on Monday, though admittedly, the magnitude of this move wasn’t massive either.

This week, the main event for the US currency will be the much-anticipated Fed policy decision on Wednesday, where markets will scrutinize by how much policymakers will revise down their rate-path projections. Specifically, will the new ‘dot plot’ keep a single rate increase in 2019 on the table, or will the median dot be marked down more severely to indicate no hikes at all? With market pricing now pointing to rate cuts this year, even signals for one rate increase could come as a ‘hawkish surprise’, and potentially put some wind back into the dollar’s sails.

Outside of the US, policy meetings by the Bank of England (BoE) and the Swiss National Bank (SNB) on Thursday, coupled with a flurry of crucial economic data out of all regions, should keep traders busy.

Pound catches its breath ahead of another Brexit chapter

After Cable soared to a fresh 9-month high, the British pound briefly moved out of the spotlight at the end of last week. That won’t last though, as this week brings several key events for sterling, both in the economic and political arenas. Besides the BoE meeting and several data releases, the Brexit process will also be back in the limelight, as PM May could make a third attempt of pushing her deal through Parliament, before the EU summit on Thursday.

Interestingly, reports over the weekend suggest she may avoid another vote altogether if it’s clear there’s no support for the deal, and that she could simply ask the EU for an extension. However, this may be a relatively bearish outcome for the pound in the near term, as May would probably only ask for a brief extension until June, keeping uncertainty heightened for a few more months. For the next leg higher to materialize, traders may need to see either a long extension that fuels hopes for another referendum, or UK lawmakers warming up to May’s deal.