{kind=link}

Risk markets attempt to recover today but lacks clear momentum. Nonetheless, that’s enough to send Swiss Franc generally lower. At the time of writing, Canadian Dollar is the second weakest. Dollar follows as third weakest despite better than expected retail sales. Sterling on the other hand recovers broadly after being pressured earlier today. The Pound is paring some losses ahead of the Brexit votes this week. Just like the EU, Sterling is awaiting some clarify on what the UK would like to do regarding Brexit.

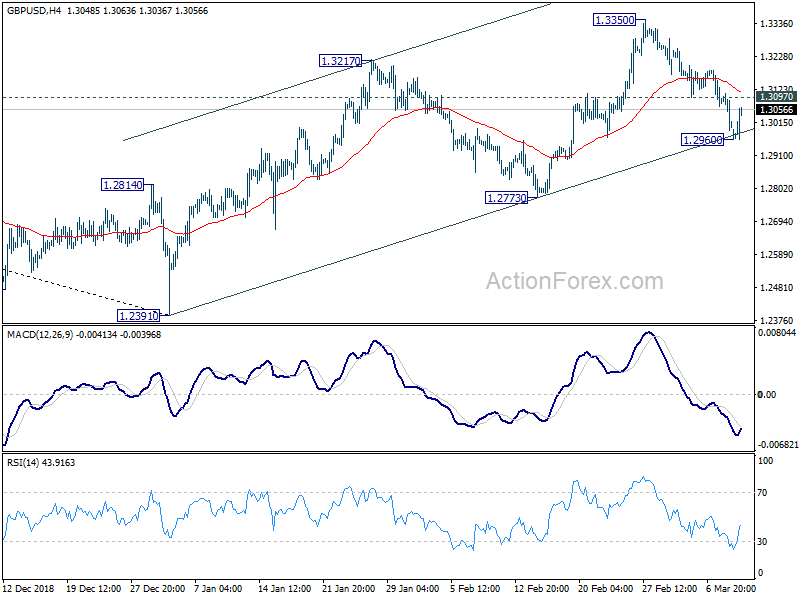

Technically, GBP/USD recovers after hitting near term trend line support and focus is back on 1.3097 minor resistance. Break will indicate completion of pull back from 1.3350. EUR/CHF rebounds strongly after testing 1.1310 near term support and retains near term bullishness. Meanwhile, Dollar is still in consolidation against Euro, Swiss Franc, Aussie and Loonie. The greenback’s retreat mildly extend lower.

In Europe, FTSE is currently up 0.24%. DAX is up 0.21%. CAC is up 0.16%. German 10-year yield is down -0.006 at 0.065. Earlier in Asia, Nikkei rose 0.47%. Hong Kong HSI rose 0.97%. China Shanghai SSE rose 1.92% to 3026.99, back above 3000. Singapore Strait Times dropped -0.14%. Japan 10-year JGB yield dropped -0.0033 to -0.035.

US retail sales rose 0.2%, ex-auto sales surged 0.9%

US January retail sales came in stronger than expected by Dollar shrugs. Headline retail sales rose 0.2% mom in January versus expectation of -0.1% mom. Ex-auto sales jumped sharply by 0.9% mom versus expectation of 0.3% mom. However, prior month’s headline sales was revised down from -1.2% mom to -1.6% mom. Ex-auto sales was also revised down from -1.8% mom to -2.1% mom.

Released in European session, German industrial production dropped -0.8% mom in January versus expectation of 0.50% mom. Trade surplus narrowed to EUR 18.5B in January. From Asia, Japan machine tools orders dropped -29.3% yoy in February, M2 rose 2.4%.

UK confirms Brexit meaningful vote on Tuesday

UK Prime Minister Theresa May’s spokesman confirmed that there will be a meaningful vote on the Brexit deal tomorrow. But at this point, it’s unsure whether the vote would be on the “agreed” deal with EU, or a “hypothetical” deal that could push EU to concede to.

The spokesman also noted that “It’s important to note the PM spoke to (European Commission President) Jean-Claude Juncker by phone yesterday evening and talks are continuing. The PM and negotiating teams are focused on making progress so we can secure parliament’s support for the deal.”

EU chief negotiator Michel Barnier refused to comment on Brexit negotiations today. Ahead of a meeting of EU ambassadors, Barnier just said “We talked all weekend and now the discussions, the negotiations, are between the government in London and the parliament in London.”

In short, there will be another parliamentary vote on the Brexit deal on March 12, next Tuesday. As it’s defeated, a vote on no-deal Brexit will then be held on March 13 to see if there is explicit consent on this path. If not, there will be another vote on Article 50 extension on March 14.

ECB Cœuré: No recession, no turnaround in policy, no need to resume asset purchases

In an interview on March 7, published today, ECB Executive Board Member Benoît Cœuré said the economy slowdown “didn’t come as a surprise” even though it has been “stronger than expected and started sooner”. ECB’s decision last week “don’t represent a turnaround in our policy” but just “carefully calibrated to this diagnosis”. And ECB was just :adjusting to the new reality rather than reversing our course”.

Coeure added “we don’t see signs of a recession at present” and “we don’t see the need” to resume asset purchases. Economic growth is “robust” although it’s “less strong than before”. And it will “take longer for inflation to reach our objective, but it will get there”.

Coeure also said Italy is “in a difficult juncture” and it’s the “only euro area country that is experience a technical recession”. There was no improvement in the labor market and in the long term, Italy’s problem is well known and it’s “productivity growth”. But “I don’t believe that any of this has to do with the euro, otherwise it would be a general problem across the euro area.”

Fed Powell: Roughly neutral interest rate appropriate with muted inflation

In CBS’s 60 Minutes show, Fed Chair Jerome Powell reiterated that current interest rates are “appropriate” while inflation is “muted”. He also described the current rate setting as “roughly neutral”. Fed is patient regarding policy adjustment and that means “we don’t feel any hurry to change our interest rate policy”.

On the economy, he said “the outlook for the U.S. economy is favorable.” And, “the principal risks to our economy now seem to be coming from slower growth in China and Europe and also risk events such as Brexit.”

Powell added that “what’s happened in the last 90 or so days is that we’ve seen increasing evidence of the global economy slowing down” and “we’re going to wait and see how those conditions evolve before we make any changes to our interest-rate policy.”

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2968; (P) 1.3038; (R1) 1.3087; More….

GBP/USD recovers as it draws support from near term trend line (now at 1.2985). Intraday bias is turned neutral first. On the downside, sustained break of trend line support will argue that rebound from 1.2391 has completed earlier than expected at 1.3350. Deeper fall would then be seen to 1.2773 support for confirmation. On the upside, above 1.3184 minor resistance will suggest that the pull back has completed. Intraday bias will be turned back to the upside for 1.3350.

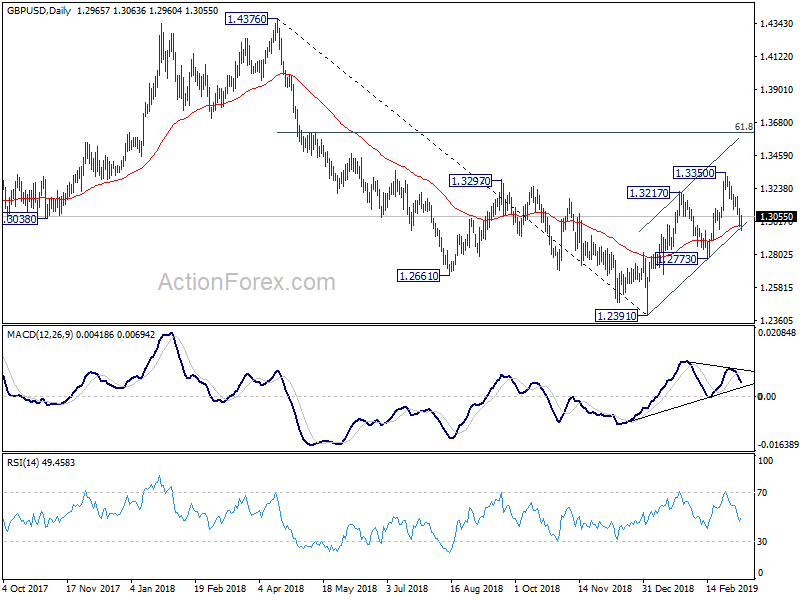

In the bigger picture, medium term decline from 1.4376 (2018 high) should have completed at 1.2391. Rise from 1.2391 is now seen as the third leg of the corrective pattern from 1.1946 (2016 low). Further rise could be seen through 1.4376 in medium term. On the downside, though, break of 1.2773 support will dampen this view. Focus will be turned back to 1.2391 low and break will resume the fall from 1.4376 to 1.1946.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Feb | 2.40% | 2.40% | 2.40% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Feb P | -29.30% | -18.80% | ||

| 07:00 | EUR | German Industrial Production M/M Jan | -0.80% | 0.50% | -0.40% | |

| 07:00 | EUR | German Trade Balance (EUR) Jan | 18.5B | 21.2B | 19.4B | |

| 12:30 | USD | Retail Sales Advance M/M Jan | 0.20% | -0.10% | -1.20% | -1.60% |

| 12:30 | USD | Retail Sales Ex Auto M/M Jan | 0.90% | 0.30% | -1.80% | -2.10% |

| 14:00 | USD | Business Inventories Dec | 0.60% | -0.10% |