{kind=link}

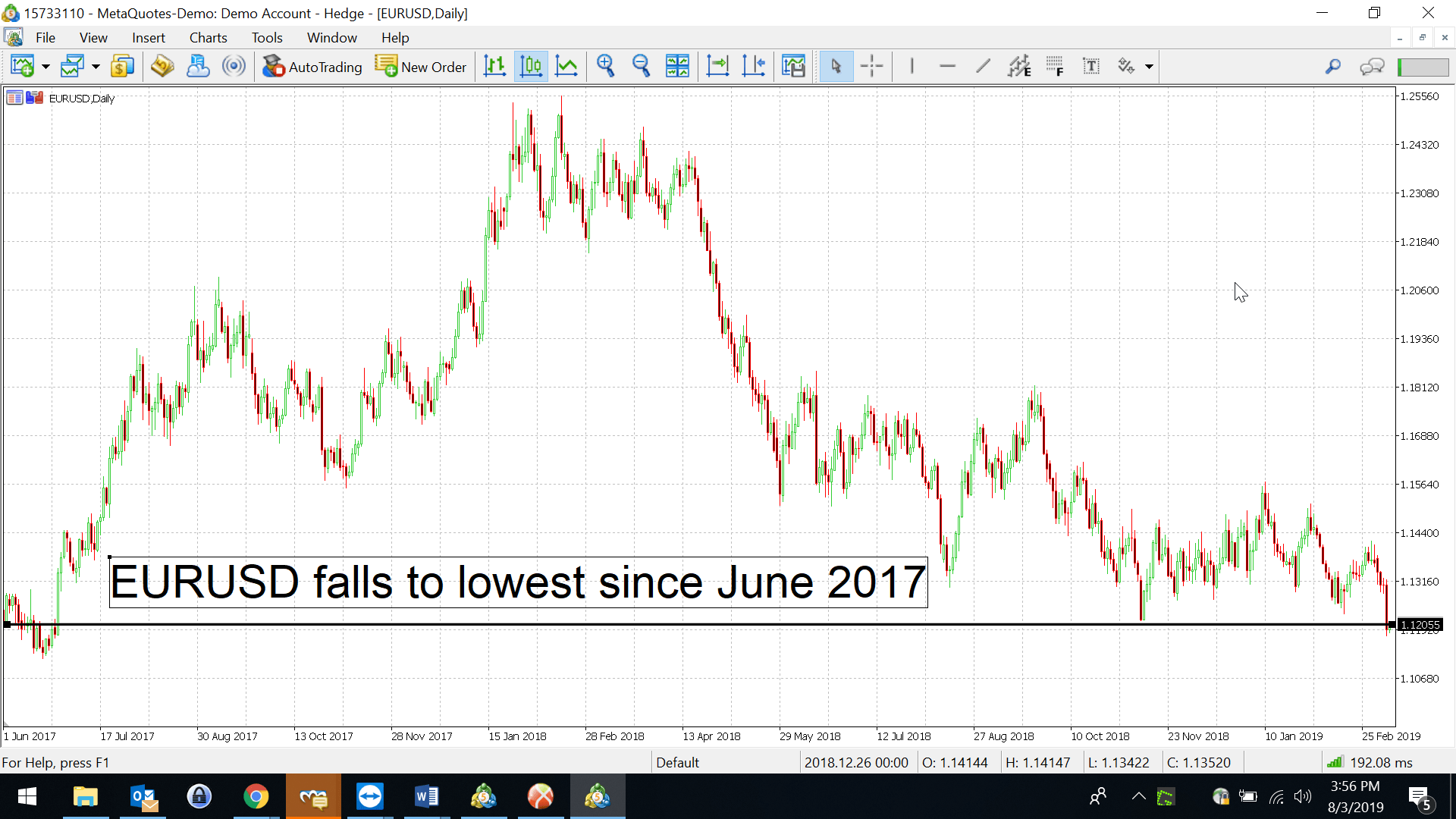

The European Central Bank (ECB) is stepping in again to support the economy. But markets aren’t buying it. EURUSD sank by over onepercent, dipping below 1.118 before climbing back closer to 1.12 at the time of writing, hovering at its lowest level since June 2017.

The ECB confirmed reports leading up to yesterday’s policy decision, by unanimously choosing to issue a new series of cheap loans to banks and keep rates on hold at least until the end of 2019. The central bank also downgraded its forecasts for both inflation and economic growth. Needless to say, none of this is positive news for Euro buyers.

Given the drop in the Euro, markets appear to be interpreting this decision as yet another instance in whichthe ECB is behind the curve. With growth and inflation still very much on feeble footing, one interpretation is that previous rounds of “policy accommodation” have failed to sufficiently boost the Eurozone. The ECB’s latest round of stimulus also indicates that the economy is far from being able to stand on its own, and is still reliant on “added accommodation”. They’re concerned enough by the worsening outlook to warrant a fresh round of stimulus, just three months after ending theirbond-buying programme.

Also note that Europe is still having to contend with “pervasive uncertainties”, as Mario Draghi described it, including Brexit uncertainties, cooling growth in China, and the still-unresolved nature of trade talks between the US and China.

Allthis paints a very gloomy outlook for the Eurozone for 2019, leaving Euro bulls with the enormous task of having to prove their case.

China External Trade Slumps in February

Beyond the dovish ECB forecast, investor confidence is taking another hit with China missing its February external trade target.

Exports declined by more than 20 percent, with imports declining by over fivepercent; both far below market expectations, even after factoring in the Chinese New Year holidays. The threat of US tariffs and a slowing European economy haveweighed on Chinese shipments, adding to concerns surrounding the world’s second largest economy.

While China has revisedits 2019 growth targets to 6.0-6.5 percent, policymakers in Beijing have promised stimulus measures, including a three percentage-point cut to its Value Added Tax. Should these stimulus measures start to take effectand reflect positively in China’s economic data, this may encourage risk-on sentiment to be reflected in the Yuan, and other Asian currencies.

For now I would however expect risk sentiment to be carried by the recent return of fears over a slowing global economy.

US February NFP Closely Watched

With the EU and China dragging global growth, coupled with Brexit uncertainties, this leaves the United States as the bright spark in a gloomy global economiclandscape. Economic divergence is back in the air, meaning the Greenback has returned as the chosen one for investors’ number one currency. It is no coincidence at all that the Dollar Index extended to its highest level of 2019, at the same time that a downbeat Draghi and ECB drove the Euro to its lowest levels of the year so far.

February’s US non-farm payrolls, due later today will be the latest indicator of the resilience of US economic growth. While markets project hiring to have moderated compared to January, it’s still expected to keep with the broader storyline – the US economy is on solid ground and more importantly, it remains way ahead of its developed peers.

This week, the US Dollar reached a new high for 2019, and may climb even higher should the NFP surprise to the upside. If the global outlook deteriorates further, that may prompt investors to engage in the divergence trade and seek shelter in the Greenback, despite the dovish stance currently held by the Federal Reserve.