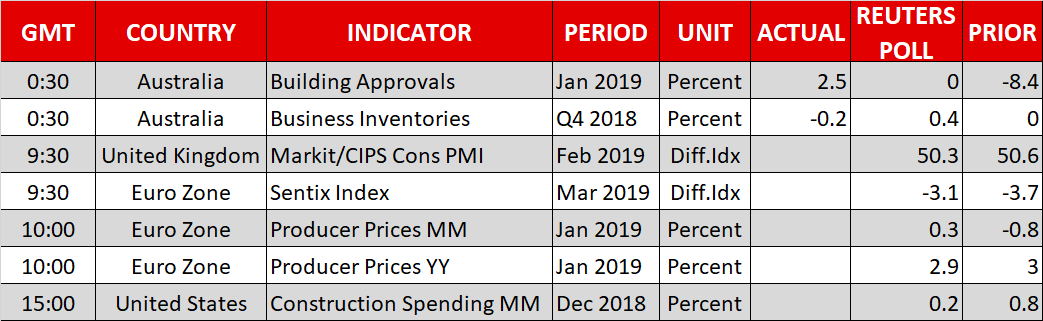

{kind=link}

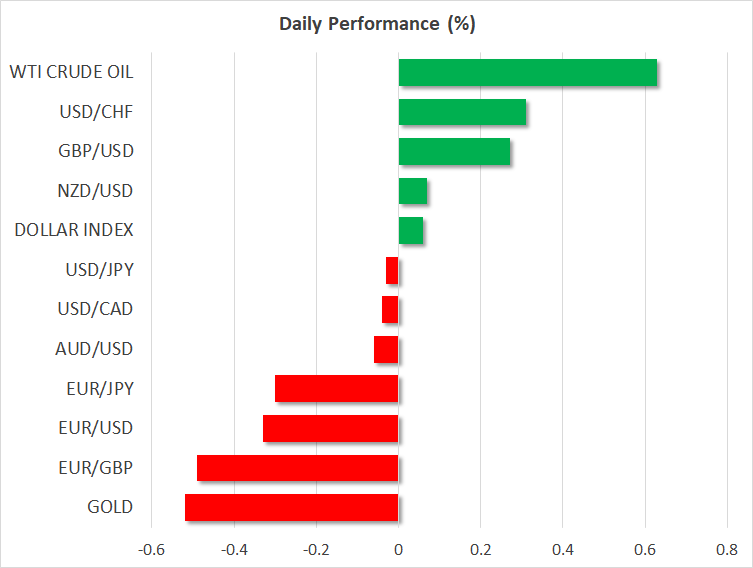

- Stocks cruise higher on reports that a trade deal is just around the corner

- Dollar advances, despite soft US data and ‘jawboning’ by Trump

- Loonie crushed as Canadian GDP disappoints, oil retreats

Equities bask in trade optimism

US stock markets closed higher on Friday, and futures suggest these indices will likely open in the green on Monday as well, fueled by renewed optimism that a US-China trade deal is just around the corner. Media reports over the weekend reinforced such expectations, indicating that an accord is very close to being struck, with China offering to lower tariffs on several US goods and curbing its own subsidies, in exchange for the immediate removal of US tariffs.

Against this positive backdrop, Asian markets are a sea of green today, as traders continue to reallocate funds towards riskier but higher yielding assets. In the FX world, currencies like the aussie and the kiwi opened with gaps to the upside, though quickly filled those to trade almost unchanged, with the aussie weighed down by a string of disappointing tier-two Australian indicators overnight. As for what’s next, with a deal now practically in the bag, market attention could shift towards the pivotal Trump-Xi meeting that is reportedly being planned for mid-March, where the two leaders are expected to put pen to paper and officially close the deal.

Dollar defies soft data and Trump jawboning, edges higher

The world’s reserve currency continues to defy naysayers, with the dollar index managing to close notably higher on Friday, even despite a bunch of disappointing US data. More impressively, the dollar is building on those gains early on Monday, staying largely unfazed by some remarks from President Trump over the weekend, who for the umpteenth time reiterated that the currency is too strong.

The greenback is currently drawing strength from the latest uptick in US Treasury yields, which are surging on the back of trade optimism, and whose increase amplifies the dollar’s carry appeal via widening interest rate differentials. Hence, the dollar remains ‘the best of all worlds’ for now, given its unique ability to gain both when trade tensions escalate and when they subside.

Loonie pulverized as Canadian GDP disappoints, oil prices drop

The Canadian dollar had the rug pulled out from under it on Friday, losing more than 150 pips versus its US counterpart, following disappointing Canadian GDP data and a sharp drop in oil prices. The nation’s economic growth for Q4 clocked in at a mere 0.4% annualized pace, far below the projected 1.2%. The miss greatly dampened expectations for any further rate hikes by the Bank of Canada, which meets this week. Looking at market pricing, investors now assign a mere 20% chance for just one quarter-point rate increase this year, and if the Bank validates as much on Wednesday, the loonie could continue to suffer.

Light start to a busy week: UK construction PMI today

The economic calendar is relatively light on Monday, with the only tier-one release being the UK construction PMI for February. As always though, Brexit considerations will be far more important in driving the pound, which is on the front foot this week following some encouraging remarks by the EU’s Barnier on Friday that Europe is ready to offer Britain further guarantees on the Irish backstop.

As for the rest of the week, the schedule is quite packed. The RBA will announced its policy decision early on Tuesday, the BoC on Wednesday, and the ECB on Thursday. To top it all off, the week is also filled with several key data releases, the most notable being the US employment report on Friday. In politics, China’s National Congress commences today.