{kind=link}

M&S and Ocado is a match made in heaven, both companies can benefit from this joint venture. The fact that Ocado is allowed to carry its own brand along with M&S products, this gives customers larger selection of products at their disposal. Ocado was in a tight spot because it needed funds to enhance the developments of its customer solution and the upfront payment of £562 million is going to help it to fully fund this development.

For M&S, this is their first opportunity to deliver their food at the doorsteps of their customers, something which they have not done before and it was badly needed in this market. Buying 50 percent share in Ocado for M&S isn’t that difficult for M&S and the company’s strategy to finance this deal by using the rights issue of shares is an appropriate strategy. A dividend is obviously a place where investors will feel some pain because M&S will cut that by 40 percent. However, this will be compensated with the increase in revenue through an increase in revenue.

The partnership will also help M&S to look at its current chain of stores more strategically and evaluates their potential more accurately, this is because if you can deliver food on the doorstep, there may be no point of having more than one store within a certain mile of the radius.

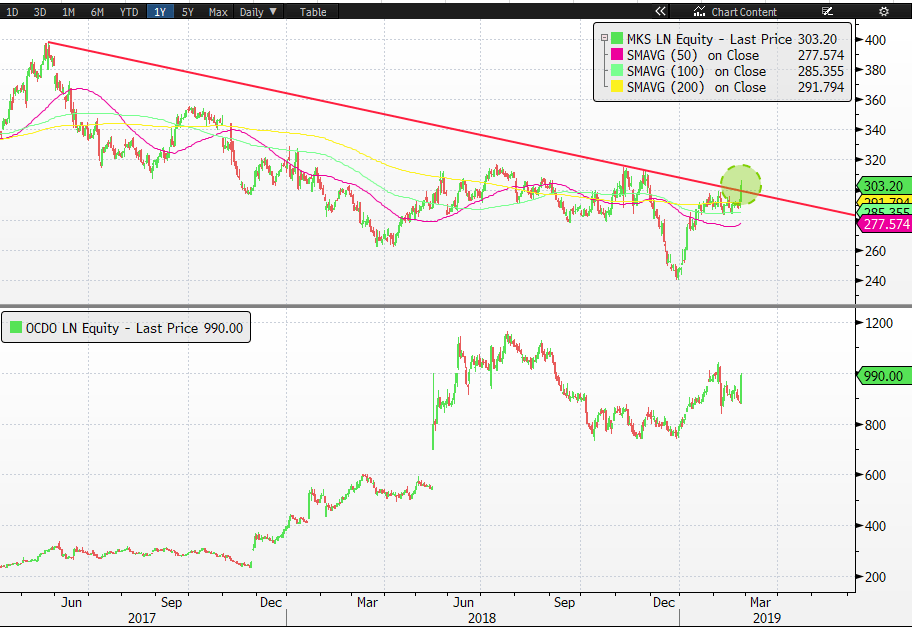

M&S shares were in strong position yesterday with a 3.2% gain while the country’s index declines. The most interesting element was the volume which was literally three times than the 20-day average and the one-month implied volatility also jumped 28 percent. The stock is trading at 12 times its estimated earning per share for 2019 and we think it is still a bargain with huge potential on the horizon.

The chart below shows that M&S stock price (in the upper panel of the chart) has broken its downward trend line, a positive sign. Also, the price is trading above the 50-day, 100-day and 200-day moving averages, all of this confirm the bull strength.