U.S. Highlights

- December retail sales came in significantly weaker than expected, falling 1.2% m/m, with the decline being broad-based. Consumption in Q4 is now tracking around 2.6% annualized – softer than expected, but still a pretty good showing.

- The retail sales report provides a weak handoff to 2019. The fact that the government shutdown extended into January and consumer confidence retreated on the month, further reinforces the notion for a soft print in first-quarter spending and GDP.

- Core inflation remained at 2.2% (y/y) in January, where it has sat for five of the past six months. And there is little indication that it will move in either direction soon. This should provide comfort for the Fed to remain patient.

Canadian Highlights

- This was a quiet week in financial markets, with the S&P/TSX moving up 1% and the CAD almost unchanged. Oil benchmarks advanced on reassuring signs of OPEC+’s curtailment discipline.

- The week was also light on data, but a poor manufacturing sales showing served to further reinforce the moderating growth narrative and slightly impacted our Q4 GDP tracking.

- Housing data delivered a pleasant surprise, advancing 3.6% on the month. Average homes prices, however, continued to decelerate.

U.S. – Wall of Uncertainty

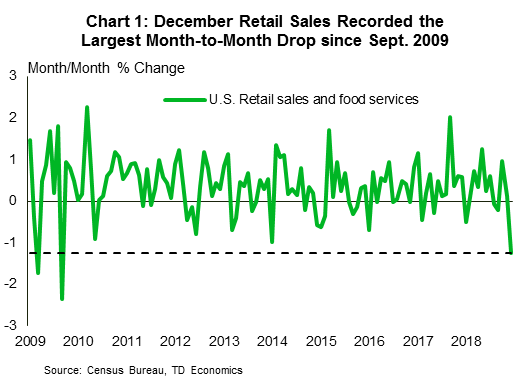

They say good things come to those who wait. But judging from developments this week, we’ll have to wait a bit longer. The delayed December retail sales report finally came out this week, but the results were deeply disappointing. While consensus had set a low bar for a nearly-flat print, sales fell a whopping 1.2% m/m – the worst decline since September 2009 (Chart 1). Moreover, the pullback was broad-based. Apart from gains at autos and building materials stores, everything else was in the red. Sales in the ‘control group’, which strips out volatile categories and is then used in the calculation of GDP, fared even worse (-1.7%).

The weak report raised a few eyebrows, with its reliability in question among economics circles. December’s result is hard to square with other industry reports, such the Redbook index, which shows same-store sales accelerating in year-over-year terms in December. The fact that non-store sales (-3.9%) weren’t spared from the pullback also raises some suspicion. This category is largely made up of online sales, where there were no other major signs of stress during holiday season. Still, giving the Commerce Department the benefit of the doubt here, it would appear that the threat and subsequent materialization of the late-year government shutdown, together with a sharp selloff in equity markets amidst elevated trade tensions with China, prompted Americans to keep a tight grip on their wallets.

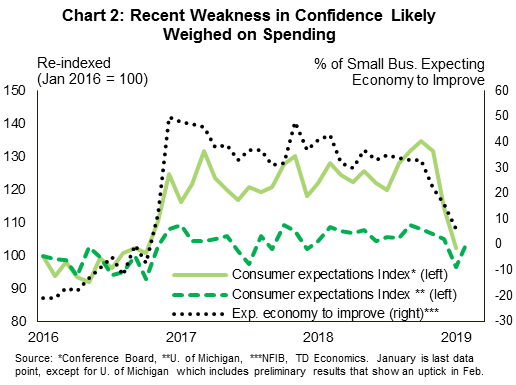

Consumer spending in the fourth quarter is now tracking around 2.6% ann. – softer than we previously expected, but still a pretty good showing. The December weakness also provides a weak handoff to the start of 2019. The fact that the government shutdown dragged on until late-January and consumer confidence deteriorated on the month (Chart 2), further reinforces the notion of softer spending, with consumption expected to advance at just below 1.5% (ann.). A pullback in small business confidence and industrial production in January provide further credence to the view for a soft quarter overall.

Similar to last year, however, we don’t expect the first-quarter performance to set the pace for the rest of the year, so long as a resilient labor market shores up spending. Consumption is expected to rebound in the second quarter, provided that there is no major disruption on the trade front or another government shutdown. Progress appeared to have been made on both of these areas this week. Reports indicate that Chinese and U.S. negotiators made headway in agreeing on broad principles, with negotiations to continue next week in Washington. It appears that President Trump will get his border wall funding by declaring a national emergency, and is also expected to sign a bipartisan spending bill that will avoid a second shutdown.

This week’s developments reinforce the notion that the Fed will stay put until muddy waters begin to clear. The other part of the Fed’s calculus, inflation trends, provide added comfort for patience. Core CPI has been holding at just above the Fed’s target recently (2.2% y/y), with little indication that it will shift in either direction. For now, it’s all about keeping the faith and playing the waiting game.

Canada – A Snooze Button Week

This week was nothing to write home about on the Canadian data and financial markets fronts. The S&P/TSX composite edged up around 1.4% on the week. Oil markets fared better, with the WTI benchmark moving more than 5% and Brent an even more impressive 6%. The absence of a U.S-China deal was countered by reassurances of Russian cuts and intentions by Saudi Arabia to curtail output further in the upcoming months. OPEC has already demonstrated commitment to its output curtailment plan; January output for the group fell more than 1 million barrels per day below its November peak. The Canadian dollar, however, didn’t follow suit, remaining almost flat against its U.S. counterpart.

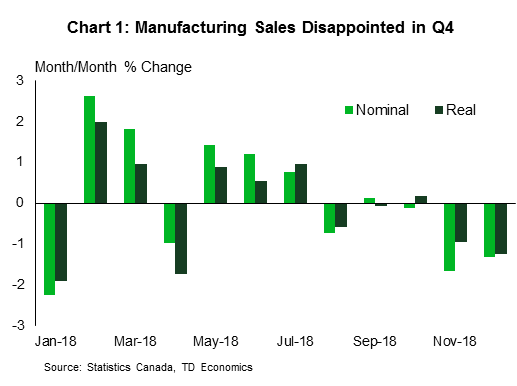

It was also quiet on the economic data front. Still, and at the risk of sounding like a broken record, one Statistics Canada release served to further reinforce the moderating growth narrative. Manufacturing sales fell for the third consecutive month, coming in at a disappointing -1.3% with an almost equal decline in volumes (Chart 1). While a 10.4% drop in petroleum and coal services was the culprit, the overall decline was still broad-based, with 12 of the 21 industries in decline.

Energy sector woes during the fall of 2018 may have been partly contributing to recent Canadian data disappointments (both in real and nominal terms), although some of the declines are also due to maintenance work at some refineries. Combined with a range of other slowing indicators, the print pushed our Q4 real GDP tracking down to 0.9%, slightly below the Bank of Canada’s 1.3% estimate in its latest MPR. Looking forward, more near-term sluggishness is expected as the Alberta oil cuts are set to impact volumes during the first quarter of 2019. The manufacturing sector should receive support in the medium term on the back of a weak loonie, still-strong growth south of the border, and evidence of capacity constraints. At least this is the hope, as Canada’s growth outlook is dependent on a much-needed rotation from consumer spending to investment and export-driven growth.

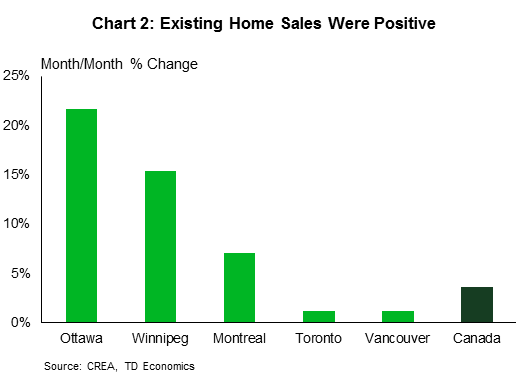

Meanwhile, Canada’s housing market delivered a relatively pleasant surprise this morning, with existing home sales advancing 3.6% – the strongest monthly change since June (Chart 2). Montreal’s surge, at 7.1% was particularly notable, but the closely watched Vancouver and Toronto markets also put in a positive showing. Still, average home prices continued to decelerate, falling 2.9% on the month as the regulation-prone B.C. and oversupplied Alberta markets continued to weigh on price growth. Moreover, the overall British Columbia market still turned in a monthly sales decline.

That said, while one month of data is not sufficient, the headline print, together with positive housing starts data should support a return to positive growth in residential investment in the first quarter of 2019.

Canada: Upcoming Key Economic Releases

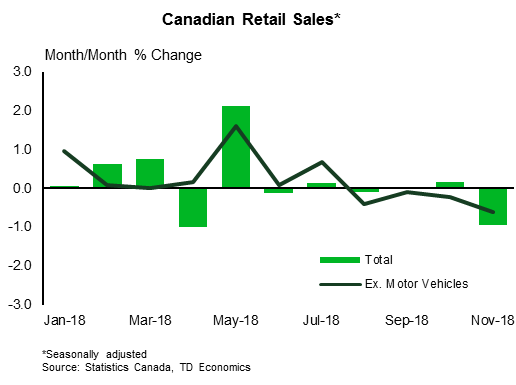

Canadian Retail Sales – December

Release Date: February 22, 2019

Previous: -0.9%, ex-auto: -0.6%

TD Forecast: -0.4%, ex-auto: -0.4%

Consensus: 0.0%, ex-auto: -0.5%

TD looks for a 0.4% contraction in December retail sales due to weaker sales at gasoline stations, with little offset from core retail sales. Seasonally adjusted gasoline prices fell by over 4% during the month which presents a headwind to sales after a 5% decline last month, although favourable weather and holiday driving may contribute to an offsetting increase in volumes. Elsewhere we expect the continued weakness in the housing market to weigh on retail sales of building materials and home furnishings, while auto sales should see a modest decline to leave the ex-autos measure in line with the headline print. Real retail sales are likely to post a slightly larger decline than the nominal series owing to higher consumer prices, which will weigh on service-sector growth in December.

{kind=link}