{kind=link}

The focus will firmly be on economic indicators next week as political and central bank events temporarily take a back seat. The latest PMI releases for the Eurozone will be one of the highlights as growth in the region grinds to a halt, while employment numbers out of Australia and the United Kingdom will attract attention too. Japanese trade and inflation figures will also be on investors’ watch list. Central banks will not be totally absent, however, as the latest meeting minutes from the RBA, ECB and the Fed should provide a fuller insight on the extent of the dovish tilt by policymakers in recent weeks.

Further risks ahead for the aussie

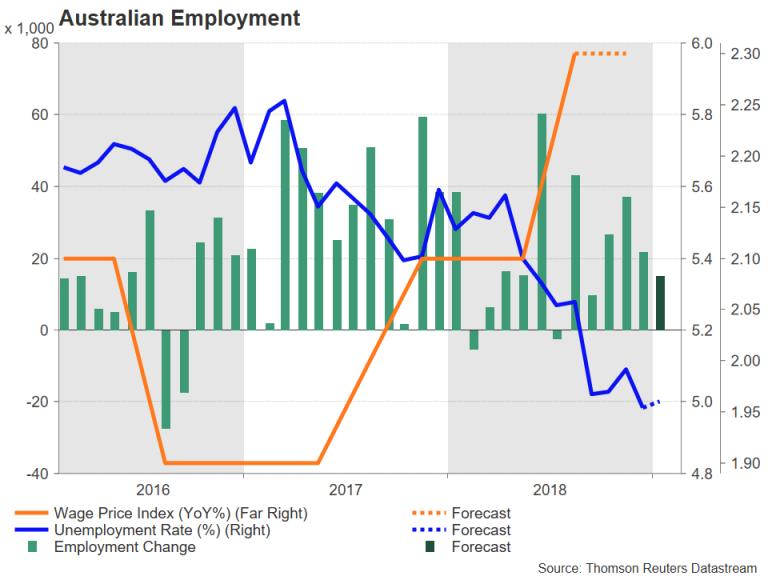

The Australian dollar managed to recover slightly in the past week from the Reserve Bank of Australia’s unexpected dovish turn in the prior week. There could be further gains ahead for the aussie if wage growth and employment numbers due out of Australia in the coming days show further tightening in the labour market.

The wage price index, due on Wednesday, is expected to show steady yearly growth of 2.3% during the fourth quarter, unchanged from the previous period. On a quarterly basis, wage growth is forecast at 0.6%. On Thursday, the labour market theme will continue with the release of the January employment report. The Australian economy is expected to have added 15k jobs in January, slowing slightly from the prior 21.6k. The unemployment rate is forecast to have held steady at 5.0%.

An overall solid set of figures should provide some support for the struggling aussie, but the currency is likely to be vulnerable to not only downside surprises in the data, but also from more dovish language from the RBA. The central bank will publish the minutes of its February meeting on Tuesday and Governor Philip Lowe will be speaking before a parliamentary committee on Friday.

Japanese inflation to tick higher

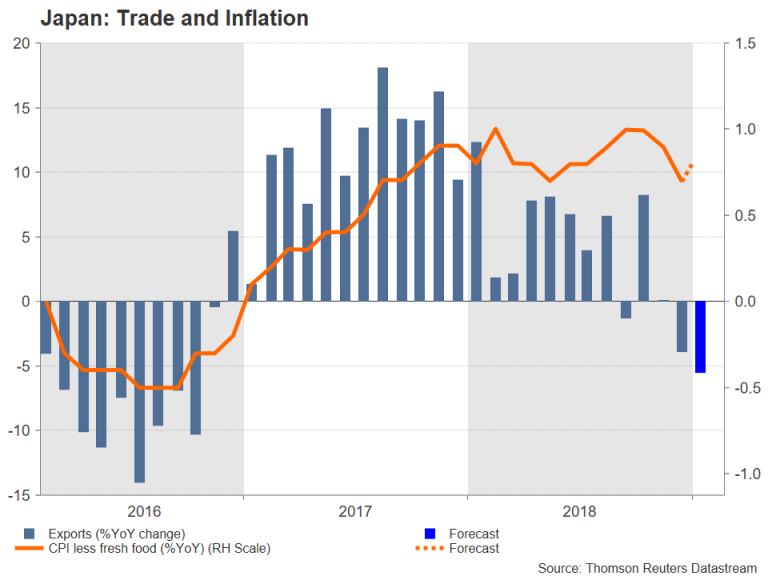

After this week’s somewhat disappointing GDP growth numbers, Japan’s economy will remain under the spotlight over the next seven days. First up on the Japanese calendar are December machinery orders on Monday. Core machinery orders – a forward-looking gauge for capital expenditure – will be looked at for possible signs that business spending could be slowing or even falling in the early parts of 2019.

Trade figures will follow on Wednesday with exports expected to have declined for a second straight month in January, while the flash Nikkei/Markit manufacturing PMI on Thursday will be the first data point for manufacturing activity in February. On Friday, the latest inflation report might provide some good news for the Bank of Japan if core CPI, which excludes fresh foods and is the Bank’s targeted price measure, edges up by 0.1 percentage points to 0.8% year-on-year in January as forecast.

Should the data signal more weakness for the Japanese economy in Q1, the yen could come under downside pressure, which is likely to be exacerbated if the broader market mood turns risk-on.

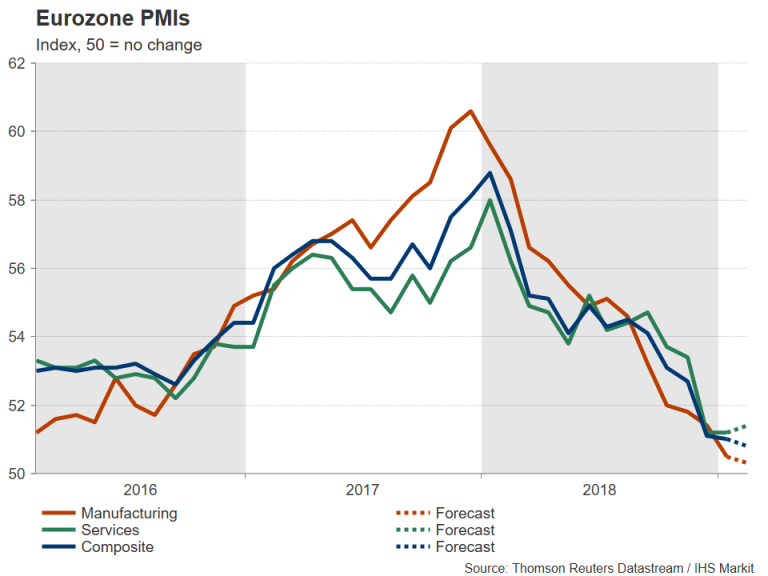

More misery ahead for the Eurozone?

Good news is in short supply when it comes to the euro area economy and this is reflected in the single currency, which continues to plough fresh lows versus the US dollar. The negative picture isn’t likely to change next week but there could be some signs that growth is steadying after months of deceleration. Germany’s ZEW sentiment survey will be the first key indicator out of Europe on Tuesday. The ZEW economic sentiment index is expected to improve marginally from -15 to -14.0 in February.

On Thursday, all eyes will be on the closely-watched flash PMI prints from IHS Markit. The manufacturing PMI is forecast to ease further to 50.3 in February, but the services PMI is anticipated to improve from 51.2 to 51.4. The German Ifo business climate index will round up the business confidence surveys on Friday and final January CPI readings for the Eurozone are also due the same day.

Meanwhile, the European Central Bank will be publishing the account of its January policy meeting on Thursday. ECB Governing Council members have been increasingly acknowledging the weakening economic backdrop in their remarks in recent weeks, adding to the growing expectations that there will be no rate hikes in 2019. However, at the last meeting, ECB head, Mario Draghi, failed to give clear signals that a change in the forward guidance on interest rates as well as a new round of TLTRO programme were forthcoming. Hence, any evidence in the minutes that Council members discussed the aforementioned in more detail than what Draghi let on in his press conference could be interpreted as a dovish sign.

Jobs data only major release from UK

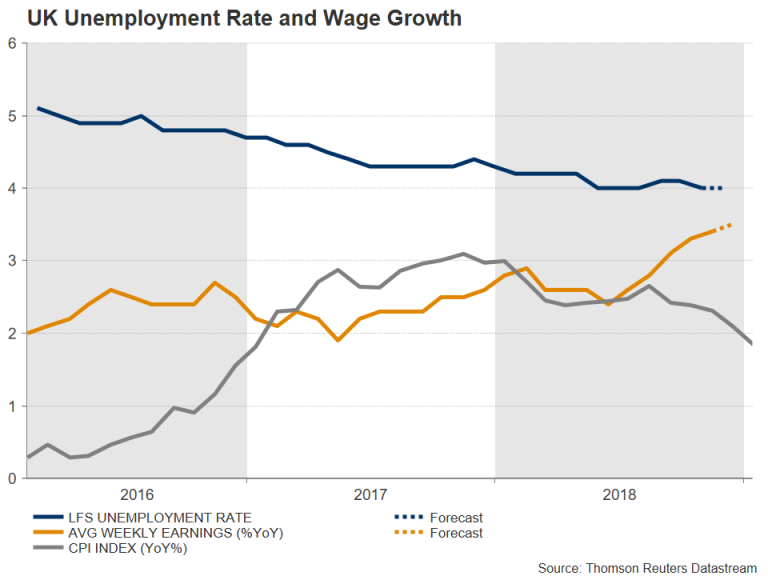

Sterling could be headed for relatively calmer trading sessions over the coming week as there may not be any significant update on the Brexit process until the following week and it’s also looking quieter on the data front. The UK labour market report on Tuesday will be the main highlight for traders.

After the worrying GDP numbers for December, a weak set of jobs figures could spark more concerns that the never-ending Brexit saga is starting to have a more profound impact on the UK economy. The jobless rate is predicted to have held at 4.0% in the three months to December, while average weekly earnings are forecast to have increased by 3.5 y/y during the same period, accelerating slightly from the prior 3.4%. Faster wage growth could be seen as offsetting some of the negative effects of lower oil prices on the consumer price index, which fell to 1.8% y/y in January.

Few headlines expected from US

US data over the coming period will probably struggle to change the mood set by the past week’s unexpectedly weak retail sales numbers for December and reports that US and Chinese negotiators remain far apart on the structural reforms that the US is demanding from China even if progress is being made in other areas of the trade talks.

The week will get off to a quiet start as US markets will be closed for Presidents’ Day on Monday and the agenda will be empty until Thursday when durable goods orders are due. Durable goods orders are forecast to have risen by 1.7% month-on-month in December, adding to the 0.7% gain made in November. The Philly Fed manufacturing index for February is also out on Thursday, as well as IHS Markit’s flash manufacturing PMI reading for the same month. A softening in manufacturing activity in February could weigh on sentiment and the dollar.

The greenback lost some steam after the poor retail sales figures but disappointment over the lack of substantial progress in the Sino-US trade talks is keeping the currency supported. But even if next week’s data does not disappoint, another risk for the dollar are the FOMC minutes of the January meeting. The Federal Reserve surprised many when it seemingly ruled out a rate hike in the near term and flagged potential changes to its balance sheet unwinding plans. Should the minutes corroborate the dovish shift, the dollar could face some increased downside pressure.

North of the border, Canadian retail sales for December will be monitored on Friday. However, a public address by Bank of Canada Governor, Stephen Poloz, on Thursday could be another focal point for traders as the speech will be on monetary policy. The Canadian dollar, which in recent weeks has been pulled in different directions from trade and growth uncertainty on the one hand and higher oil prices on the other, will likely be sensitive to any hints on future rate moves.