U.S. Highlights

- Global central banks have followed the cue set by the Fed, as they too take a break from tighter monetary policy to assess mounting risks to global growth.

- Activity in the U.S. services sector cooled a bit in January as government-funding uncertainty and trade tensions weighed on business sentiment. Nonetheless, non-manufacturing activity remained well in expansion territory.

- Senior U.S. trade officials are off to Beijing next week to work on a trade deal, even as a meeting between the two countries’ presidents seems unlikely before the March 2nd deadline. All eyes will be on Washington to avert yet another government shutdown as the temporary funding gap expires on February 15th.

Canadian Highlights

- We received mixed signals this week, with household credit growth moderating on the back of an outright decline in consumer credit, while the labour market kicked off 2019 with a bang.

- The signal being sent by the credit data deserves attention, but is not overly concerning at present. A period of household adjustment may moderate economic growth, but it also means stronger balance sheets – a welcome development.

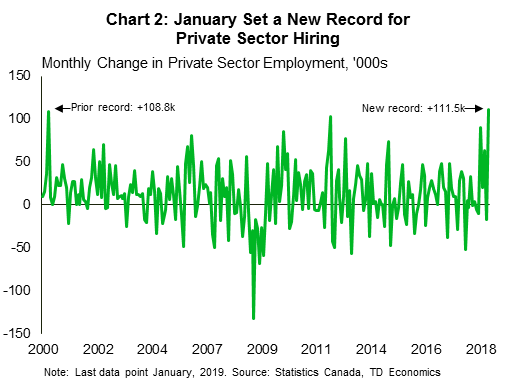

- The strong labour market, including a new record for monthly private sector hiring is encouraging, indicating that the household adjustment is taking place against a solid economic backdrop.

U.S. – Central Banks Have Cause For a Pause

In a week where economic data was sparse (partly due to delayed releases as a result of the government shutdown), global developments filled in the gap. On the heels of the Fed’s decision last week, the Bank of England (BoE) and the Reserve Bank of Australia (RBA) both left policy rates unchanged this week.

The BoE cited the likelihood of slower growth due to elevated financial uncertainty on the possibility of a no-deal Brexit, while the RBA highlighted trade-related downside risks to global growth. Elsewhere, the European Commission also significantly reduced its GDP outlook for the euro zone in 2019 and 2020 as it expects growth in the bloc’s largest economies to be held in check by global trade tensions.

The decidedly dovish shift in U.S. and global central banks’ statements reflects the turn south in economic and inflation momentum in the latter half of 2018, as well as the accumulation of event risks over the next several months. Among these, trade tensions between the U.S. and China looms largest.

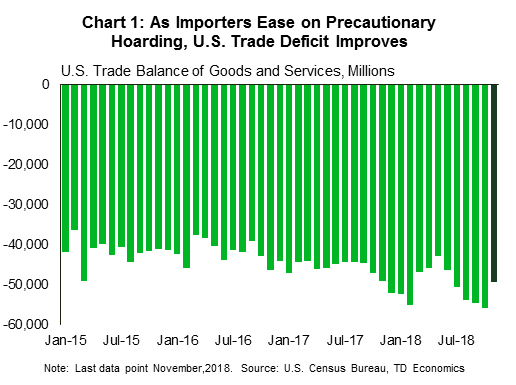

On that front, prospects for a trade deal were dealt a blow this week with the announcement that President Trump is unlikely to meet with Chinese President Xi before the March 2nd deadline for additional U.S. tariffs. Continued uncertainty about the tariff hike has led to volatility in the international trade data. Imports fell fairly substantially in November, perhaps reversing some earlier inventory hoarding, as hopes for a trade deal increased (Chart 1). They could rebound again in the months ahead as prospects dim.

As long as the economic tea leaves remain cloudy, expect data-dependent central bank officials to remain cautious, taking the time to evaluate the cumulative impact of tighter financial conditions and slowing trade. Stateside, this will have to be balanced against economic data that so far has continued to show resilience. As expected, initial jobless claims fell by 19k back towards post-recession lows during the week ended Feb 2nd as the effects of the longest U.S. government shutdown faded. In conjunction with the jobs report released last week, the data points to continued labor market strength.

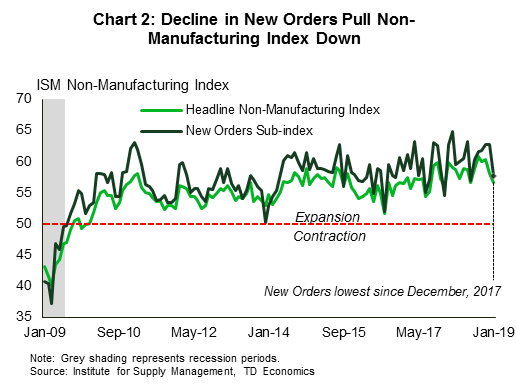

Still, there are signs that the shutdown has had a negative impact on activity. The pace of expansion in the services sector decelerated in January. The ISM non-manufacturing index fell to 56.7 in January from 58.0 in December, reflecting concerns about the government shutdown, which negatively impacted new orders (Chart 2).

In his State of the Union address President Trump pleaded for unity, but continued to press a hardline on border security and immigration. All eyes will be watching the February 15 deadline for a longer-term funding package to avert yet another government shutdown that could take an additional toll on U.S. economic growth.

Canada – Don’t Fret Deleveraging (Yet)

Canadian markets had a mixed week. The TSX looked likely to end the week up a tick at the time of writing, despite some volatility through Thursday’s trading session. The modest gain came despite softer oil prices, with both U.S. and Canadian benchmarks trading a few dollars lower.

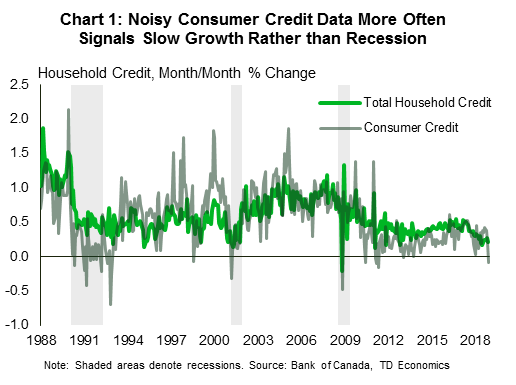

On the data front, it was a quiet week with only two major indicators for economy watchers to digest. First up was the household credit data for December 2018. Unsurprisingly, total credit continues to decelerate in the wake of past interest rate increases. However, what drew the most attention was an outright decline in consumer credit – the first in five years (Chart 1). Credit is the lifeblood of any modern economy, so such a move bears closer scrutiny particularly as some have begun throwing out the term ‘recession’.

Breaking out the ‘r-word’ is a bit premature. For one thing, shrinking consumer credit is a necessary condition for recession, but not sufficient. Its ‘hit rate’ as a predictor of a downturn is, charitably, about 33% – meaning that this signal is wrong twice as often as it is correct. What the data is saying, however, is that we are experiencing decelerating growth, particularly for consumer spending. This should come as no surprise. Canadians are digesting rising interest costs at the end of a multi-decade borrowing cycle – a moderation of credit is only a natural result.

To be sure, the balance between repairing household finances and maintaining spending growth is a tricky one – too sharp a deceleration of credit (or an outright contraction/deleveraging) can have a marked, negative impact on the economy, just as too much credit growth drives financial risks higher. The interplay of incomes and credit measures will be closely watched by the Bank of Canada in setting the path of borrowing costs going forward. The result so far looks to be what we expect (and we all should hope for): a more modest pace of economic growth, but one that comes with healthier consumer finances and a broadening of growth sources. So, while the credit data is throwing up a caution flag, we aren’t hitting the panic button just yet.

Reinforcing the ‘caution, not panic’ narrative is a still solid labour market. January saw an impressive 66.8k net jobs added as monthly private sector hiring set a new record (Chart 2). While not all details were as great (total hours worked were actually down a bit, and Alberta experienced another challenging month), the solid, if modest hiring trend of 2018 appears to be continuing (see our report on the trends that drove last year’s performance).

So, the takeaway from this week’s data seems to be that yes, the Canadian economy is likely entering a period of more modest growth, but this should not cause too much concern. The process of repairing household balance sheets should be welcomed, provided the pace remains within reason. We have no reason to doubt that it will, particularly given that Canadian labour markets remain solid by almost any measure. It is a long road ahead, but so far so good.

U.S.: Upcoming Key Economic Releases

U.S. Consumer Price Index – January

Release Date: February 13, 2019

Previous: -0.1% m/m; core 0.2% m/m,

TD Forecast: 0.1% m/m; core 0.2% m/m

Consensus: 0.1% m/m; core 0.2% m/m

We expect headline CPI to retreat to 1.5% thanks to lower gasoline prices. Outside of fuels, however, we see strength across food and core services. The latter should underpin a 0.2% m/m print on core CPI, translating to a 2.1% y/y increase vs 2.2% previously. All eyes are on OER and rents, which we expect to rebound by 0.3%. The main risks to this report are medical care services and hotels (10% of the core index), both of which could correct. Strength in the former especially looks unsustainable, while the latter is volatile. Looking ahead, we look for headline CPI is likely to remain in a narrow 1.4-1.6% range with a break toward 2% unlikely until Q4.

U.S. Retail Sales – December

Release Date: February 14, 2019

Previous: 0.2%, ex auto: 0.2%, control group: 0.9%

TD Forecast: 0.1%, ex auto: 0.1%, control group: 0.2%

Consensus: 0.1%, ex auto: 0.0%, control group: 0.4%

We forecast retail sales to rise 0.1% m/m in December, down from 0.2% in November and a more robust 1.1% increase in October. The shutdown-affected release should continue to reflect a negative impact from lower gasoline prices and a more measured expansion in core sales. We pencil in the latter at 0.2% m/m, down from a year-high 0.9% jump in November. That said, we see risks to the upside given the resiliency of the US consumer on the back of a strong labor market and steady wage growth.

Canada: Upcoming Key Economic Releases

Canadian Manufacturing Sales – December

Release Date: February 14, 2019

Previous: -1.4%

TD Forecast: 0.6%

Consensus: N/A

Manufacturing sales are forecast to rebound by 0.6% in December after a 1.4% drop last month. This release will be subject to greater uncertainty as a result of disruptions to international trade data, although looking at broader set of indicators points to a partial recovery. Lower gasoline prices will continue to weigh on refinery output, although a return to normal operations after maintenance shutdowns should support stronger volumes. Outside of energy a broad increase in factory prices, a spike in hours-worked and strong manufacturing conditions south of the border provide further evidence in support of a pickup. Real manufacturing sales should come in above the headline print owing to lower industrial prices, driven by petroleum products, providing a source of strength for industry-level GDP.

{kind=link}