{kind=link}

Japan and the United Kingdom will be next to publish economic growth numbers for the final quarter of 2018, while the Eurozone will release its second GDP estimate for the period. Inflation data out of the US and the UK will also be watched. The Reserve Bank of New Zealand will be among the last of the major central banks to hold its first monetary policy meeting of 2019. The Bank is unlikely to buck the trend and will probably follow its peers in shifting to a more dovish stance.

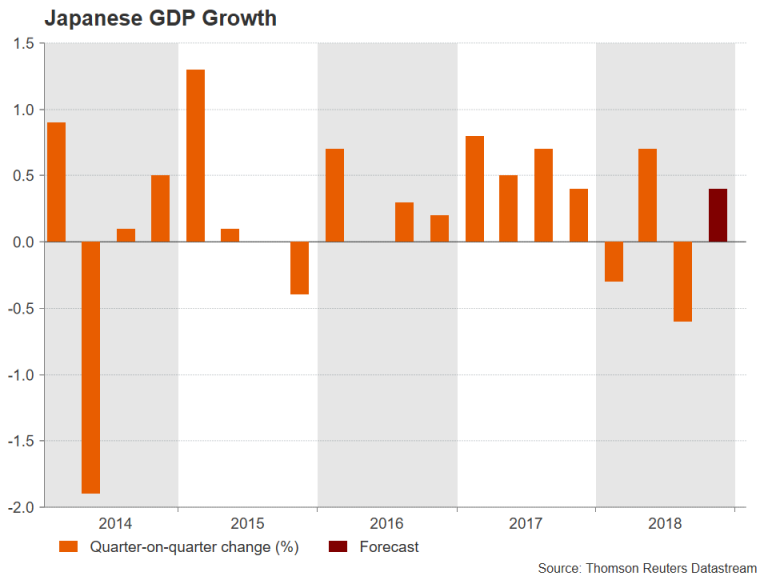

Growth in Japan to rebound in Q4

Japan’s economy is expected to have returned to growth in the final three months of 2018. Data on Thursday is anticipated to show GDP expanded by 0.4% quarter-on-quarter after contracting by 0.6% in the third quarter. While a stronger-than-forecast figure could give the yen a little bit of a bump up, it’s unlikely to allay concerns that more negative quarters could be on the way in 2019 as trade tensions and slowing growth globally weigh on Japanese exporters.

Prior to the GDP report, corporate goods prices – a measure of wholesale prices in Japan – will be looked at on Wednesday.

RBNZ meets; could signal increased rate hike chances

In some ways, the Reserve Bank of New Zealand was ahead of the game when it opened the door to the possibility of a rate cut back in August 2018, while other central banks held on to overoptimistic growth forecasts. Since the start of the year, all major central banks have either turned more dovish or taken a more cautious tone. The RBNZ could go one step further at its meeting on Wednesday and provide a more explicit signal of looser policy even as it holds the cash rate steady for now.

The New Zealand dollar has already faced a sell-off this past week from surprisingly weak employment numbers for the fourth quarter. The RBNZ could spark sharper losses in the kiwi if it bolsters its dovish language and lowers its economic projections in its latest Monetary Policy Statement, due to be published the same day.

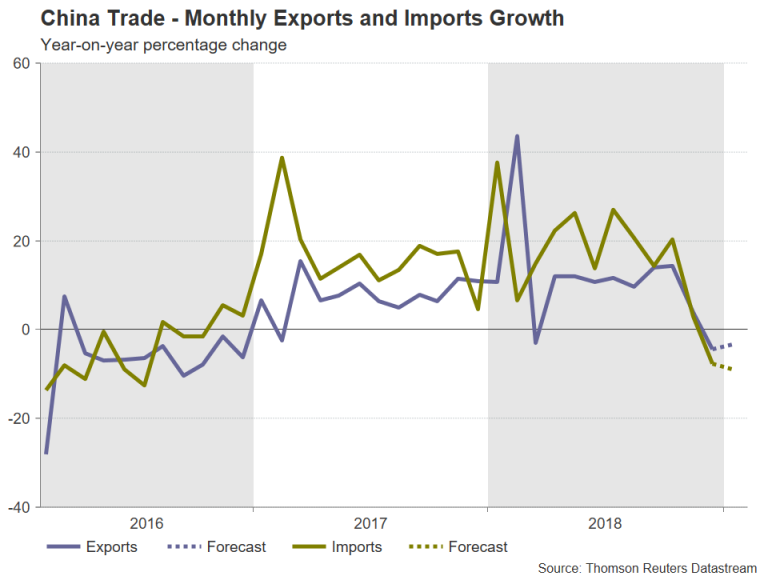

Further drop expected in Chinese exports

China will likely post another worrying set of trade figures on Thursday as trade tensions with the US continue to dampen demand for Chinese goods. Exports fell by 4.4% year-on-year in December – the fastest decrease in two years. The annual rate of decline is expected to have eased to 3.3% in January, which could perhaps provide some relief if confirmed.

However, a bigger focus will probably be the next round of trade discussions between US and Chinese officials next week. As the March 1 deadline approaches, investors will be looking for more concrete evidence of substantial progress. Otherwise, any sign that US tariffs on Chinese imports will go up again after the deadline if a deal isn’t reached by then could upset the fragile recovery in risk appetite that’s been in progress since the start of the year.

In other data from China, the January numbers for the producer and consumer price indices will be published on Friday.

The Australian dollar, which plunged by more than 2% versus the US dollar this week following the RBA’s shock dovish tilt, could come under further pressure if Chinese exports fall by more than expected and/or the Sino-US trade talks end without any significant agreement being reached.

Domestic data could also move the aussie as the NAB business confidence gauge for January is released on Tuesday along with December housing finance figures.

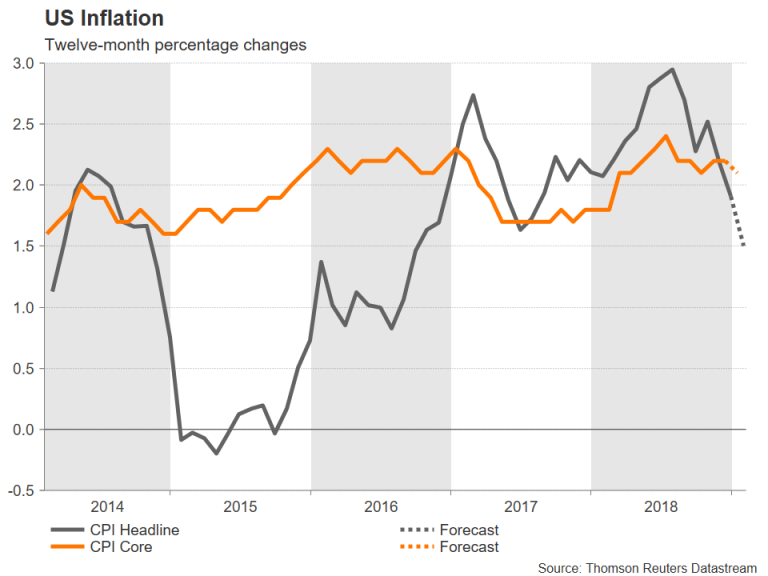

US inflation eyed

It’s going to be relatively quiet in the US as some key data such as Q4 GDP have yet to be rescheduled following the disruption from the government shutdown. The spotlight will therefore fall on inflation indicators. The CPI report is out on Wednesday with the headline rate forecast to have moderated from 1.9% to 1.5% y/y in January. Producer prices, also for January, will follow on Thursday, with import and export prices coming up on Friday.

The other major releases will consist of the Empire State manufacturing index for February, industrial output numbers for January and the University of Michigan’s preliminary consumer sentiment index for February, all of which are due on Friday.

A strong set of data could lift the dollar index above the 2-week top scaled this week. However, political developments will likely be bigger drivers for the dollar in the next seven days as US-China trade talks resume and Republicans and Democrats try to hammer out a deal on government funding. US lawmakers have until February 15 to agree on a new funding bill if they are to avert another shutdown. If there are signs that the US is headed for a prolonged period of government shutdown, this could weigh on the greenback as it would begin to have a more notable impact on GDP growth.

Eurozone growth worries to persist; Riksbank to hold rates

The past week saw another run of poor growth indicators out of the world’s second largest economic area and that trend will probably continue over the next few days. Eurozone industrial output numbers are due on Wednesday and are forecast to have declined by 0.3% month-on-month in December. On Thursday, Eurostat will publish its second estimate of Q4 GDP growth, while Germany will post its flash estimate. Eurozone growth is expected to be left unrevised at 0.2% but the German economy is predicted to have eked out growth of 0.1% after shrinking by 0.2% in the third quarter. Euro area employment figures for the fourth quarter might attract some attention too on Thursday.

If there’s any more negative surprises in next week’s releases, the euro is at risk of further down moves, with the $1.13 handle already looking shaky. However, with most of the bad news priced in by now and a shock print from Germany being very unlikely given that full year estimates released earlier more or less confirmed a 0.1% number for Q4, the bears may struggle to push the euro much lower in the near term.

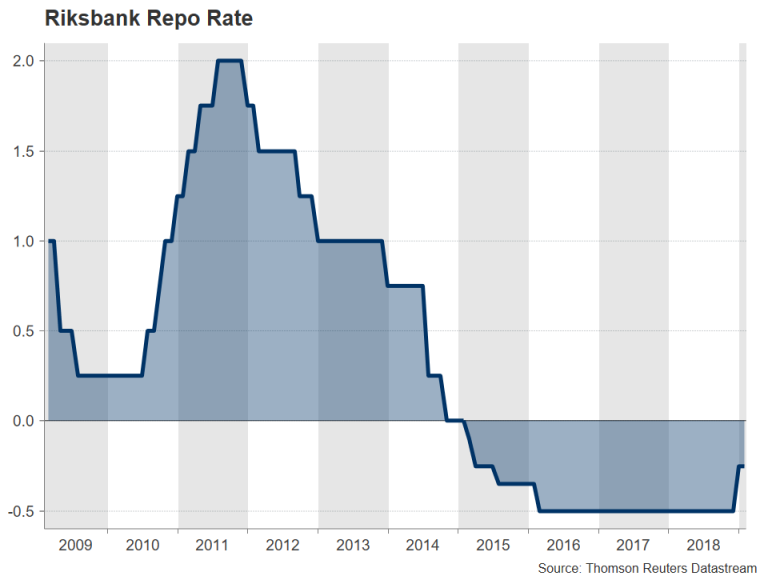

Also on the European horizon next week is the policy meeting by the Riksbank. Sweden’s central bank surprised some when it raised interest rates from -0.50% to -0.25% at its last meeting in December. However, it was a dovish hike as the bank simultaneously cut its economic forecasts and lowered its projected rate hike path. No change is anticipated therefore at Wednesday’s meeting and the Swedish krona could face some downside pressure if the Riksbank turns even more cautious about the outlook.

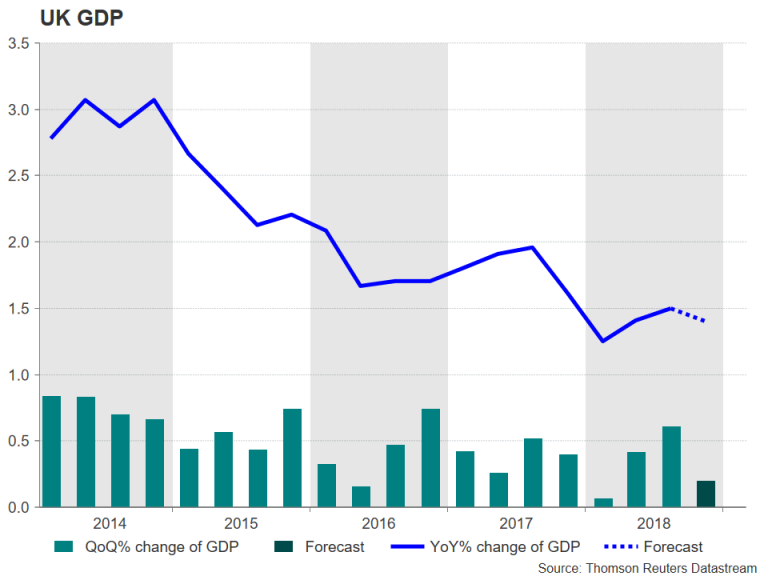

UK GDP growth to slow in Q4; inflation to hit target

The latest PMIs pointed to UK growth stagnating at the start of the year, but in the last three months of 2018, the British economy probably managed a modest expansion of 0.2% q/q. The GDP report on Monday will be accompanied by a slew of other data, including industrial production and trade. Industrial and manufacturing output are both forecast to have returned to positive growth, rising by 0.2% m/m each in December.

On Wednesday, all eyes will turn to January inflation figures. The headline rate of CPI is expected to have eased from 2.1% to 2.0% y/y in January, bang on the Bank of England’s target. The core rate is forecast to hold steady at 1.9% y/y. Lastly, retail sales numbers will be watched on Friday with only a tepid recovery being anticipated following December’s 0.9% m/m drop.

The pound could be in line for some small gains if the data surprises mostly to the upside, especially after the BoE signalled this week that rate hikes would still be on the cards if there is a smooth Brexit, despite the weaker global backdrop. However, traders are unlikely to place any large bets in sterling until there’s more clarity on whether Theresa May will be able to win significant concessions from the European Union on the Irish backstop issue.

It’s hard to see such a breakthrough happening in the next week or two, but in the event that the EU do offer Prime Minister May some compromise over the coming days, a vote on an amended Brexit deal could potentially be held on February 14.