{kind=link}

The Bank of England and the Reserve Bank of Australia will be next in the central bank world to set monetary policy amid rising risks and uncertainty about the outlook. It will be relatively quiet on the data front as Chinese markets will be shut for the whole week for the Lunar New Year celebrations, while the US economic calendar will be void of top tier releases.

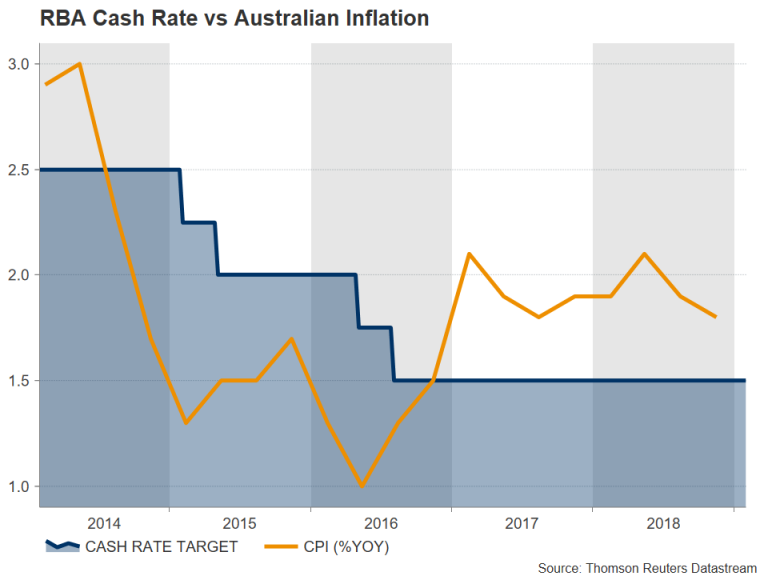

RBA to hold rates; may lower growth forecasts

The Australian dollar will take centre stage next week as a slew of data releases and an RBA policy meeting will be watched for possible clues about the direction of interest rates. The RBA has so far mostly stuck to its rosy growth outlook for 2019 but the markets don’t agree and are pricing in a small chance of a rate cut by year end. Investors think the soft inflation picture in Australia and the deepening slowdown in China will force the RBA to either delay a hike in the cash rate or to cut it.

If the central bank tones down its optimism at Tuesday’s meeting and follows this up with downward revisions to its growth and inflation forecasts in its quarterly Monetary Policy Statement on Friday, odds that the next move in rates will be down could jump.

If the central bank tones down its optimism at Tuesday’s meeting and follows this up with downward revisions to its growth and inflation forecasts in its quarterly Monetary Policy Statement on Friday, odds that the next move in rates will be down could jump.

A dovish tilt could severely pressure the aussie, which has been rallying this week on the back of better-than-expected inflation in Q4 and a sell-off in the US dollar. The latest numbers on building approvals on Monday, and retail sales and international trade on Tuesday (all for December) could also create some volatility for the aussie.

Loonie looks to jobs figures to extend gains

Another currency benefiting from the greenback’s pullback is the Canadian dollar. Rising oil prices have also been lifting the loonie but next week’s data could prove significant in determining whether the rally has further room to run as GDP numbers this week showed the economy contracted slightly in November, pointing to sluggish growth in the final three months of 2018. The Bank of Canada has said further rate hikes will still be needed over the coming period but if growth remains weak, the BoC may follow the Fed and pause its tightening cycle.

The first data point to watch out of Canada next week are Tuesday’s trade figures for December, followed by the January Ivey PMI on Wednesday. The more important one though for investors will be Friday’s jobs report. Employment growth picked up substantially towards the end of 2018, but a lot of the growth was in part-time employment, which may explain why wage growth actually moderated during the year. A disappointing report could cast doubt on whether the BoC would be in a position to raise rates anytime soon, leading the loonie to pare back some of its recent gains.

Kiwi eyes labour market indicators

New Zealand will also publish its latest stats on the labour market next week. Fourth quarter numbers on the unemployment rate, jobs growth and wages are all due on Thursday. Like its aussie and loonie counterparts, the New Zealand dollar surged against the US currency during the past week, while recent domestic data has not been as gloomy as feared. If employment continued to expand in Q4 and wage increases did not slow, the kiwi should be able to hold on to its impressive gains.

Dollar unlikely to find much reprieve from US data

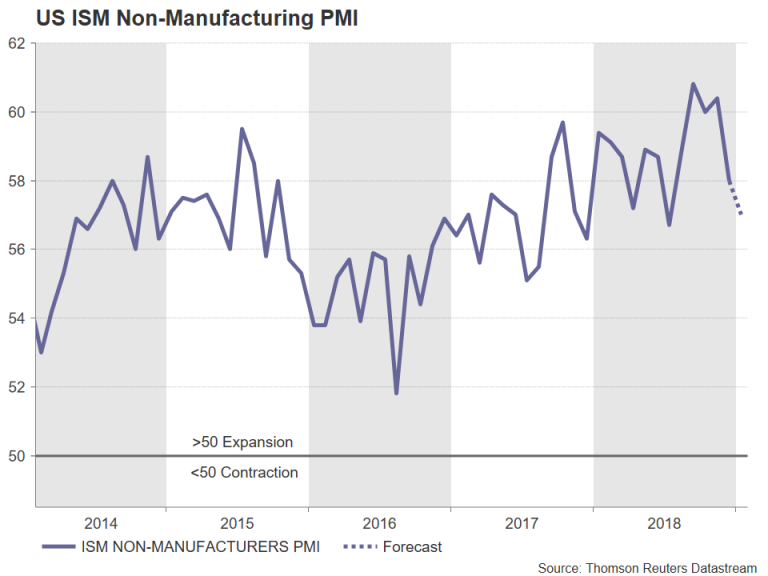

After the highly anticipated Fed meeting and all-important NFP report, US events will take a back seat next week, which means the sliding dollar could struggle to find much support in the markets. Nevertheless, any positive surprises could give the greenback a bit of a bump up, starting with Monday’s factory orders. They are forecast to have risen by 0.4% month-on-month in November after slumping by 2.1% in the prior month. The ISM non-manufacturing PMI will follow on Tuesday, with the closely-monitored activity gauge projected to ease to 57.0 in January from an upwardly revised 58.0 in December. Finally, on Wednesday, November trade figures and fourth quarter productivity numbers will be watched.

Bank of England meets amid Brexit chaos

With less than two months to go before the UK formally leaves the EU, the Bank of England will have the difficult task of setting monetary policy with no idea yet on whether or not there will be an orderly exit. Policymakers had already taken a more cautious stance at the last meeting in December as the Brexit uncertainty dragged on and given the heightened anxiety about the global growth outlook since then, the Bank could go one step further and signal fewer rate hikes than currently being projected for the next three years.

Bearing in mind that the BoE will also have updated quarterly forecasts at its disposal and there is a post-meeting press conference scheduled, some shift in policy is possible on Thursday.

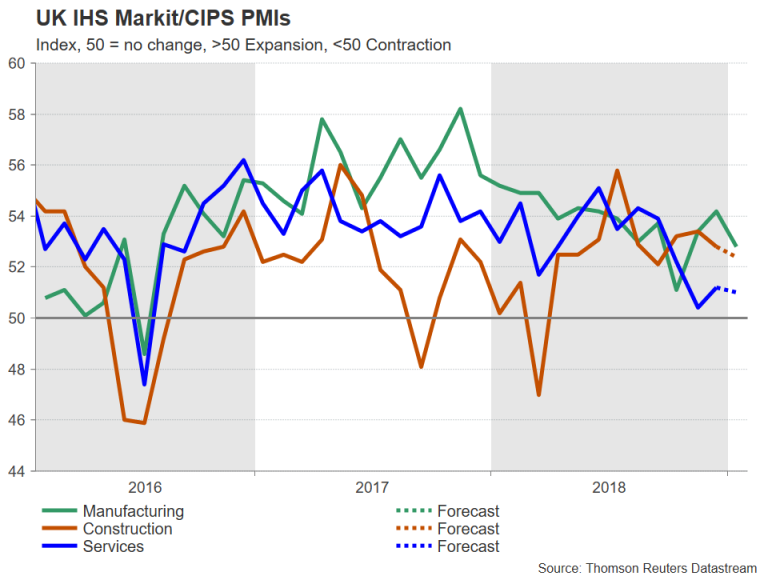

Ahead of the BoE meeting though, investors will be keeping an eye on Monday’s Markit/CIPS construction PMI, as well as the services PMI on Tuesday. The UK’s dominant services sector is expected to have slowed slightly in January, with the PMI falling to 51.0 from 51.2.

Any weakness in the data as well as a more dovish BoE would likely weigh on sterling, which has been on the retreat after Parliament failed to approve handing power to MPs to block a no-deal Brexit. A negative turn could make the $1.30 level an easy target for the pound next week.

Lacklustre week for the euro

With both the dollar and the pound getting onto a negative footing over the past week, the euro hasn’t been able to capitalize on their weakness particularly well as economic data from the Eurozone continues to disappoint. The single currency might find some upside from next week’s numbers, however, as some of the releases are forecast to show an improvement.

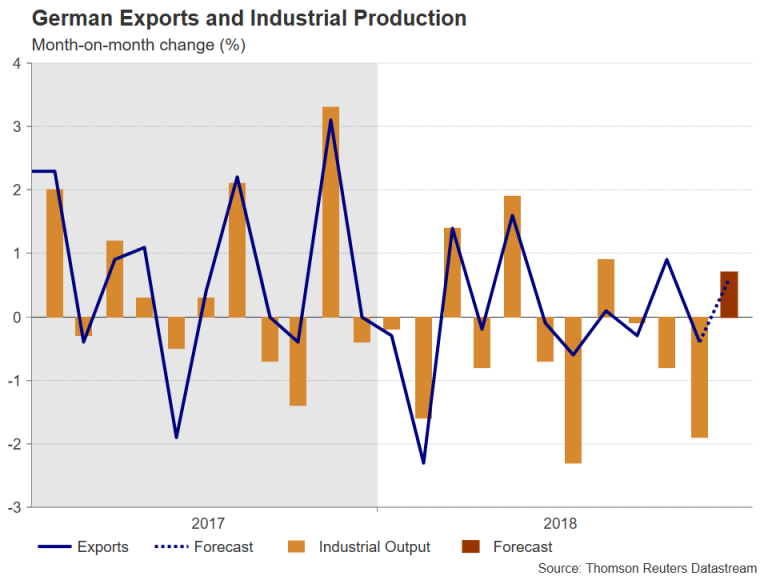

First up is the Eurozone sentix index on Monday, with the economic sentiment gauge expected to rise to -0.6 in February from -1.5 previously. Producer prices are also due on Monday, while on Tuesday, the final January prints of the IHS Markit services and composite PMIs are released along with retail sales for December. Retail sales are forecast to have declined by 1.6% m/m in December. German indicators in the following days should be more positive though. German industrial orders, out on Wednesday, are forecast to have risen by 0.3% m/m in December, while Thursday’s industrial output data is expected to show an increase of 0.7% m/m for the same period. Trade figures due on Friday could produce a hat trick as exports are anticipated to have increased by 0.6% m/m in December.

A set of positive readings from Germany could ease concerns of a sharper slowdown in the euro area’s largest economy. But more poor numbers could keep the euro stuck below the $1.15 handle for a while longer.