{kind=link}

Sterling is the star performer today as campaign to block no-deal Brexit in the UK gathers momentum. Some upside acceleration is seen after the Pound takes out near term resistance against Dollar, Euro and Yen. New Zealand Dollar is following as the second strongest as boosted by stronger than expected CPI. Though, it handed the top spot to the Pound in early US session. On other hand, as risk sentiments stabilized, Yen is trading as the weakest one, followed by Swiss Franc. Canadian Dollar turns softer after weaker than expected retail sales. But loss in the Loonie is so far limited.

Technically, GBP/USD and GBP/JPY reaches recent rally today. GBP/USD is heading to 1.3174 key resistance. GBP/JPY is targeting 143.93 first and could march towards 150 handle later. EUR/GBP is now targeting 0.8620/55 support zone. USD/JPY also breaks 109.89 resistance to resume recent rebound. Now, it’s EUR/JPY’s turn to take on 125.09 resistance. One more level to watch is 0.7116 in AUD/USD. Break should confirm near term bearish reversal.

In other markets, FTSE is currently down -0.33%. DAX is up 0.32%, CAC is up 0.46%. German 10-year yield is up 0.010 at 0.248. Earlier in Asia, Nikkei closed down -0.14%. Hong Kong HSI rose 0.01%. China Shanghai SSE rose 0.05%. Singapore Strait Times dropped -0.68%. Japan 10-year JGB yield rose 0.0034 to 0.004, turned positive. US futures point to higher open. There was some jitters on renewed concern over US-China trade negotiations yesterday. But traders were quickly calmed by White House economic advisor Larry Kudlow’s comment that “the story was unchanged, We are moving towards negotiations.”

Released from Canada, headline retail sales dropped -0.9% mom in November versus expectation of -0.5% mom. Ex-auto sales dropped -0.6% mom versus expectation of -0.4% mom. From US, house price index rose 0.4% mom in November versus expectation of 0.2% mom.

UK Labour highly likely to back amendment to block no-deal Brexit

The campaign to block a no-deal Brexit in the parliament is gaining momentum today. Labour lawmaker Yvette Cooper put an cross-party supported amendment proposal earlier, to try to impose a deadline of February 26 for Prime Minister Theresa May to get the Brexit deal approved by the parliament. Otherwise, there would be a parliamentary vote on delaying Brexit. The second most influential Labour member John McDonnell said today the party is “highly likely” to back Cooper’s amendment. He added “Yvette Cooper has put an amendment down which I think is sensible”.

However, UK Prime Minister Theresa May criticized that “What we have seen is amendments seeking to engineer a situation where Article 50 is extended – that does not solve the issue, there will always be a point of decision. The decision remains the same: no deal, a deal or no Brexit”.

Regarding no-deal Brexit, Moody’s senior vice president Sarah Carlson warned that “from a sovereign credit perspective, if you end up with a ‘no deal’ Brexit that is a sign that something institutionally has really quite profoundly failed.” And, that would weigh negatively on UK’s creditworthiness.

EU Moscovici: Brexit has to be dealt with in London first

European Commissioner for Economic and Financial Affairs Pierre Moscovici reiterated the EU’s stance that regarding Brexit, the ball is in UK’s court now. He said “Certainly the EU is there, the EU is waiting, the EU is ready but first we need to know clearly what are the British intentions and we need some clarifications from London”.

He added that “Of course the door is always open for discussion but it’s not up to us to tell now the British side where it wants to go. The ball clearly is in the British side again. It’s not a problem that can be solved by Brussels, maybe in Brussels later, but it has to be first dealt with in London.”

Also on the possibility of hard Brexit, Moscovici said “Nobody wants a no-deal (Brexit), that is clear. The British parliament doesn’t want a no-deal, the British government doesn’t want a no-deal, and the EU is not willing a no-deal, so we need to explore all options which are not a no-deal.”

BoJ stands pat, sharp downward revision in fiscal 2019 inflation forecast

BoJ left monetary policies unchanged today as widely expected. New economic projections are also released with upgrade in fiscal 2019 and 2020 GDP forecasts. But inflation forecasts was lowered rather sharply for fiscal 2019.

The short term interest rate is held unchanged at -0.1%. And under the yield curve control frame work, BoJ will continue to kept 10-year JGB yield at around 0%, with some upward and downward movements allowed. The annual amount of JGB purchase will be kept at JPY 80T.

Member G. Katakoa dissented as usual, pushing to strengthen monetary easing. Y Harada also dissented again, criticizing that allowing the long-term yields to move upward and downward to some extent was too ambiguous

On economy, BoJ maintained that “Japan’s economy is likely to continue on an expanding trend through fiscal 2020.” Also, “overseas economies are expected to continue growing firmly on the whole, although various developments of late warrant attention such as the trade friction between the United States and China.”

In the new GDP projections, comparing with October forecasts:

- Fiscal 2018 is revised to 0.9% to 1.0% (median 0.9%), down from 1.3% to 1.5% (median 1.4%).

- Fiscal 2019 is revised to 0.7% to 1.0% (median 0.9%), up from 0.8% to 0.9% (median 0.8%).

- Fiscal 2020 is revised to 0.7% to 1.0% (median 1.0%), up from 0.6% to 0.9% (median 0.8%).

The revisions showed that while BoJ is optimistic for 2019, it also sees larger uncertainties.

In new core CPI projections, comparing with October forecasts, and exclude effect of sales tax hike:

- Fiscal 2018 is revised to 0.8% to 0.9% (median 0.8%), down from 0.9% to 1.0% (median 0.9%).

- Fiscal 2019 is revised to 0.8% to 1.1% (median 0.9%), down sharply from 1.3 to 1.5% (median 1.4%).

- Fiscal 2020 is revised to 1.2% to 1.4% (median 1.4%) down from 1.4% to 1.6% (median 1.5%).

The downside revision in fiscal 2019 core CPI is rather steep.

Also from Japan, trade deficit narrowed to JPY -0.18T in December versus expectation of -0.49T. All industry activity index dropped -0.3% mom in November versus expectation of -0.4% mom.

NZD jumps on solid CPI, bets on RBNZ cut recede

New Zealand Dollar is lifted notable today but better than expected consumer inflation data. CPI rose 0.1% qoq in Q4 versus expectation of 0.0% qoq. On annual basis, CPI was unchanged at 1.9% yoy, above expectation of 1.8% yoy. The data eased worries that inflation outlook is worsening and chance for a rate cut by RBNZ is reduced. Majority of economists are still expecting the next move to be a hike. But for now, there is no time frame for that move yet.

Meanwhile, the outlook is still clouded by fading momentum in the economy, as show in recent forward-looking indicators. There is question on whether domestic inflation could sustain. And should data ahead disappoint, there bets on rate cut will re-emerge.

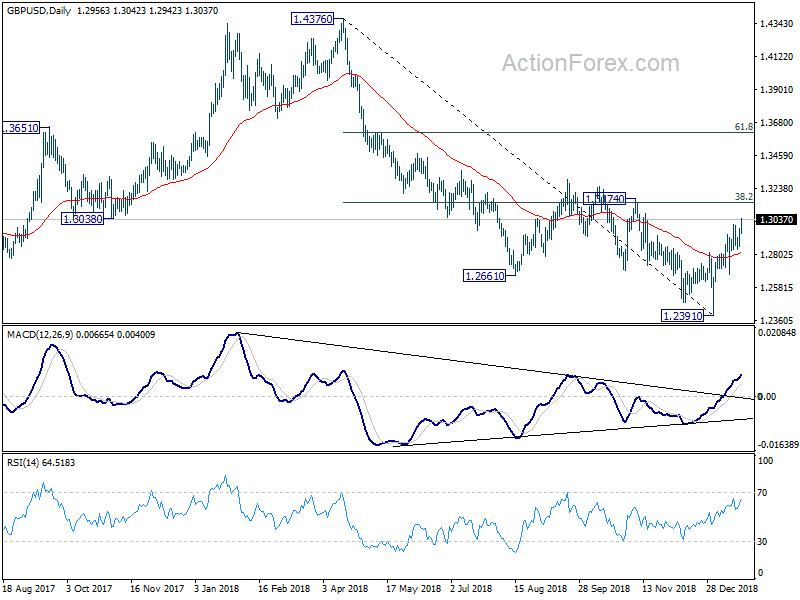

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2883; (P) 1.2929; (R1) 1.3004; More….

GBP/USD’s rebound from 1.2391 resumes today by taking out 1.3001 and reaches as high as 1.3042 so far. Intraday bias is back on the upside for 1.3174 resistance, which is close to 38.2% retracement of 1.4376 to 1.2391 at 1.3149. We’d expect strong resistance from there to limit upside, at least on first attempt. On the downside, break of 1.2830 support is needed to be the first sign of near term reversal. Otherwise, outlook will stays cautiously bullish in case of retreat.

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA. The structure and momentum of the fall from 1.4376 argues that it’s resuming long term down trend from 2.1161 (2007 high). And this will remain the preferred case as long as 1.3174 structural resistance holds. GBP/USD should target a test on 1.1946 first. Decisive break there will confirm our bearish view. However, sustained break of 1.3174 will invalidate this case and turn outlook bullish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | CPI Q/Q Q4 | 0.10% | 0.00% | 0.90% | |

| 21:45 | NZD | CPI Y/Y Q4 | 1.90% | 1.80% | 1.90% | |

| 23:30 | AUD | Westpac Leading Index M/M Dec | -0.21% | -0.09% | ||

| 23:50 | JPY | Trade Balance (JPY) Dec | -0.18T | -0.29T | -0.49T | -0.49T |

| 02:00 | JPY | BoJ Rate Decision | -0.10% | -0.10% | -0.10% | |

| 04:30 | JPY | All Industry Activity Index M/M Nov | -0.30% | -0.40% | 1.90% | |

| 11:00 | GBP | CBI Trends Total Orders Jan | -1 | 4 | 8 | |

| 13:30 | CAD | Retail Sales M/M Nov | -0.90% | -0.70% | 0.30% | 0.20% |

| 13:30 | CAD | Retail Sales Ex Auto M/M Nov | -0.60% | -0.40% | 0.00% | -0.20% |

| 14:00 | USD | House Price Index M/M Nov | 0.40% | 0.20% | 0.30% | |

| 15:00 | EUR | Eurozone Consumer Confidence Jan A | -6.5 | -6.2 |