{kind=link}

- British lawmakers will vote on the Brexit deal today; outcome crucial for sterling

- In the broader market, risk aversion is abating as China outlined plans for fresh stimulus

- Some remarks by ECB President Draghi may also attract attention

Sterling turns its sights to the long-awaited parliamentary vote

The spotlight will fall on the UK today, where Parliament will vote on the government’s Brexit deal during the evening, between 1900-2100 GMT. The consensus overwhelmingly suggests a rejection and hence, the real question – which could also determine how the pound reacts – may instead be how heavy the defeat is, that is to say by what margin the accord is voted down.

A devastating rejection of say more than 100 lawmakers could hurt the pound, as any hopes that a revised version of this deal may pass later vanish, and the odds for early elections rise. However, if the motion is voted down only by a slim margin, the currency may gain on speculation that a revised version of the deal could pass in subsequent attempts. Of course, an approval would be an upset, and could see sterling skyrocket.

From a longer-term perspective, the risks surrounding the UK currency increasingly seem skewed to the upside. Although there are still some short-term threats including the uncertainty that early elections could bring, the biggest tail risk – a no-deal exit – seems to have abated somewhat lately as Parliament has seized control of the process. So long as a disorderly exit is avoided, practically every other scenario is likely positive for the pound in the bigger picture.

China’s stimulus hints turn market sentiment around

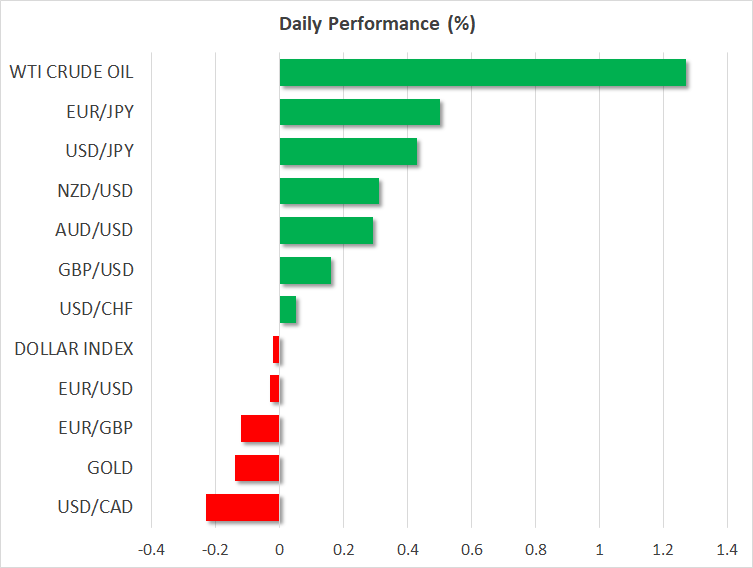

Risk appetite remained in ‘risk-off’ territory on Monday, following the disappointing trade data out of China, which reignited concerns that the world’s second-largest economy is slowing down amid a damaging trade dispute with the US. Accordingly, the Japanese yen that is viewed as a safe-haven asset outperformed, while US stock indices closed lower.

However, sentiment seems to have turned around today, following a chorus of market-supportive comments out of China overnight. Officials from both the People’s Bank of China (PBoC) and the government hinted that even more stimulus may be on the way to cushion the economy. As such, the defensive yen is lower today, while Asian equity markets were a sea of green, and futures tracking the major US benchmarks like the S&P 500 are pointing to a higher open.

Coming up: US PPI data and remarks from ECB’s Draghi

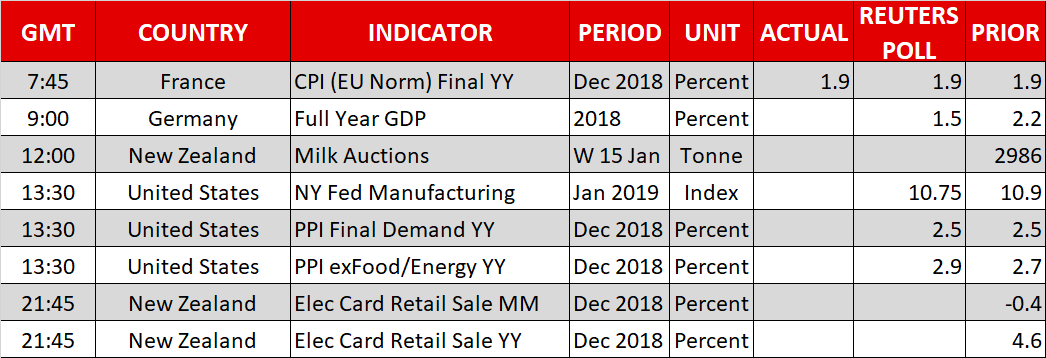

Outside of the UK, the economic calendar will be relatively light today. In the US, the producer prices for December are due out alongside the Empire State manufacturing PMI for January – the first regional survey for the new year. Although neither typically has much of a market impact, they are worth keeping an eye on in light of fears a recession may be drawing closer.

Staying in the US, regional Fed Presidents Kashkari (1630 GMT), Kaplan (1800 GMT), and George (1815 GMT) will all delivers remarks.

Meanwhile in Europe, ECB President Draghi will address the European Parliament at 1500 GMT. Keep in mind there’s been a slight shift in tone from some ECB members lately towards a more cautious direction amid slowing growth; it will be interesting to see if Draghi echoes such concerns.

Finally, in equity markets, the earnings season has kicked off. Notable names releasing their quarterly results today include JPMorgan Chase and Wells Fargo.