{kind=link}

It was only six months ago that the consensus was building that 2019 would be the year of the Euro. Although the reality as we enter the early stages of the new trading year is that instead of 2019 becoming the year where the Euro bounces back, is that the currency of Europe faces high risks of becoming an unfortunate casualty of global market turmoil.

The Euro, British Pound and Australian Dollar stand as the prime contenders to suffer the most out of the G-10 currencies from a prolonged risk-off environment in financial markets, where investors are unwilling to add risk into their portfolios due to ongoing concerns over slowing global growth.

What still hasn’t been priced into the Euro with the focus in Europe for a number of months directed on the Italian budget deficit is how exposed the Eurozone economy is to headwinds from the expected global economic slowdown. The prolonged trade tensions between the United States and China is also a major risk to the European economy. Europe relies heavily on demand from both nations for its goods, therefore if each of the economies in question slowdown this year this will have a resulting consequence on European data.

Thelikelihood of weakening economic momentum in the EU will also wipe away optimism that the ECB will aim to raise interest rates before the end of 2019.This would represent more bad news to Euro investors, and I see the probability of market expectations for a potential rate hike from the ECB to be pushed back sooner rather than later.

This means that when looking for opportunities for the Euro to extend higher in 2019, we are limited to bounces higher on USD weakness. This is where investors should spot another potential concern for the Euro because market participants are entering 2019 guilty of becoming too bearish on the Greenback. Yes, the United States economy is expected to slow down this year and this would be negative for the USD.However, an economic slowdown in the United States will not change the fact that the U.S. economy is still outperforming many of its developed peers and even emerging markets. If the expected global economic downturn does arise early in 2019, I would expect this to be positive for the USD because US assets are still favored byinvestors due to their yield on offer.

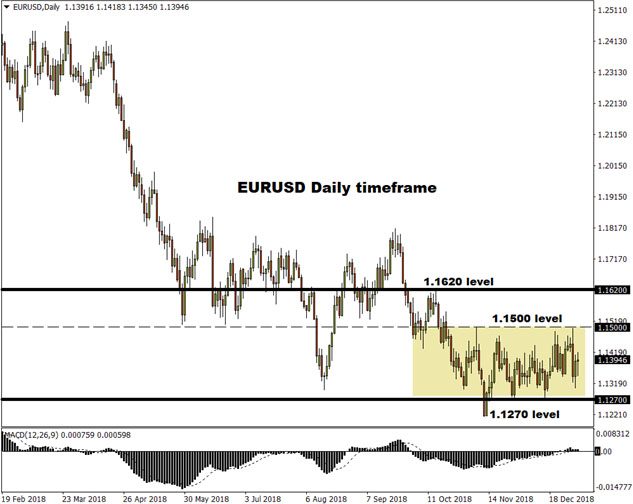

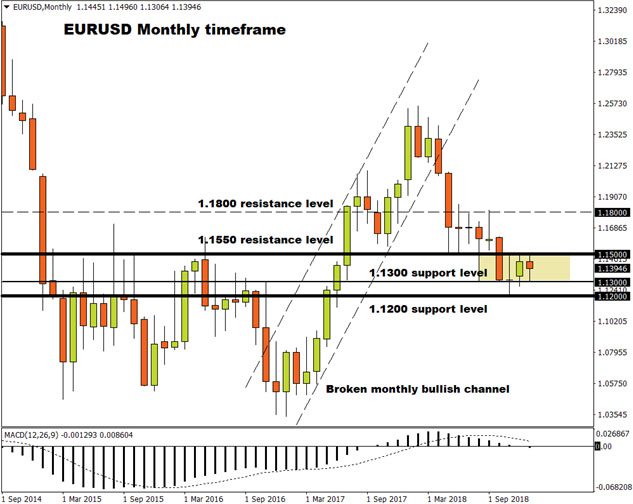

In regards to the technical outlook, we can see that the EURUSD has found stubborn short-term support close to 1.13, but travelled withina very narrow range between 1.145 and 1.12 for most of the final quarter of 2018. Even if the Euro manages to rally higher, the EURUSD faces tough resistance at 1.15 which will probably be used by investors as an opportunity to attack the Euro on rallies.

On the flip side, a breakdown on the monthly chart below 1.12 will be seen as inspiration for investors to send the EURUSD to levels that can potentially extend below 1.10.