{kind=link}

- US stock indices extend losses, Nasdaq enters bear market as concerns around future growth feed risk aversion

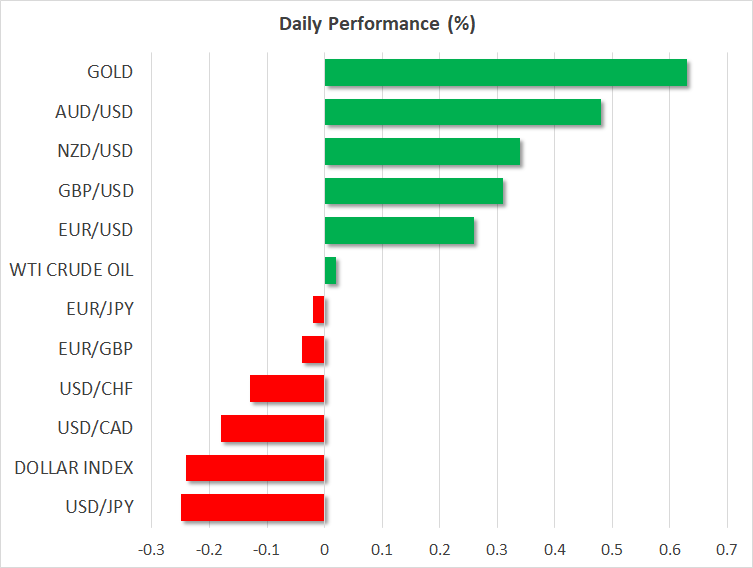

- Dollar and yen outperform on safe-haven demand, but are giving back some gains on Monday amid encouraging trade headlines

Equities drop to fresh lows as uncertainty reigns

US stock indices closed with sharp losses once again on Friday, in an environment characterized by thin liquidity, as investors attempted to protect their profitability heading into the New Year via liquidating more of their prior long positions. Technology stocks bore the brunt of the pain, with heavyweights such as Apple (-3.89%), Amazon (-5.71%), and Facebook (-6.33%) leading the way lower. Consequently, the tech-heavy Nasdaq Composite (-2.99%) officially entered a bear market, characterized as a 20% drop from its highs, while the benchmark S&P 500 (-2.06%) was not far away from entering its own bearish waters.

While the catalyst behind the latest leg lower was not clear, the main culprits seem to have been the partial US government shutdown that started on Friday coupled with the ongoing worries that the Fed is making a policy error by hiking rates further. Most striking was the fact that equities struggled even after New York Fed President Williams shifted to a more dovish tone, highlighting that rate hikes could slow further should growth disappoint.

Taking a step back, investors seem increasingly concerned 2019 may indeed be a year during which growth slows severely, not least due to fiscal stimulus fading, and hence are positioning accordingly. Yet, US economic data outside of the housing market remain solid, so it remains to be seen whether the economy will ultimately evolve as markets seem to expect. For now, though, the adage of “don’t try to catch a falling knife” is likely the most prudent approach, as the sell-off may still have legs to run before valuations reach levels attractive enough to lure investors back in.

Dollar and yen shine as investors seek safety

The dollar was the second-best performer on Friday, behind the Japanese yen, with both of these defensive currencies benefiting from the latest bout of risk aversion in markets. Sentiment seems to have turned around on Monday, albeit only slightly, likely helped by some encouraging news on the trade front that China and the US had a “deep exchange of views” on intellectual property protection. Separately, China also announced it will lower import taxes on roughly 700 products starting from January 1, as part of the ongoing effort to open up its economy.

On a different front, the dollar reacted very little to reports over the weekend that President Trump is considering whether to fire Fed Chair Powell, which was later denied both by Treasury Secretary Mnuchin and acting White House chief of staff Mulvaney.

As for the dollar and yen, given how light the economic calendar is over the coming days, their near-term direction may hinge primarily on how risk sentiment develops. Should the mood remain in risk-off territory, these two defensive assets could finish the year on a high note in the midst of safe-haven demand. On the contrary, risk-sensitive currencies such as the aussie, kiwi, and loonie, may remain broadly on the back foot in such conditions.