{kind=link}

Euro rises broadly today as Italy finally got its 2019 budget plan approved by the European Commission. Disciplinary actions are now avoided. Italian 10-yield yields tumbles sharply and is pressing September’s low. For now, Yen follows as the second strongest. Canadian Dollar is recovering today as oil prices turned sideway after this week’s sharp fall. The Loonie also pays little attention to slowing CPI reading. Sterling is the weakest one, followed by Australian Dollar.

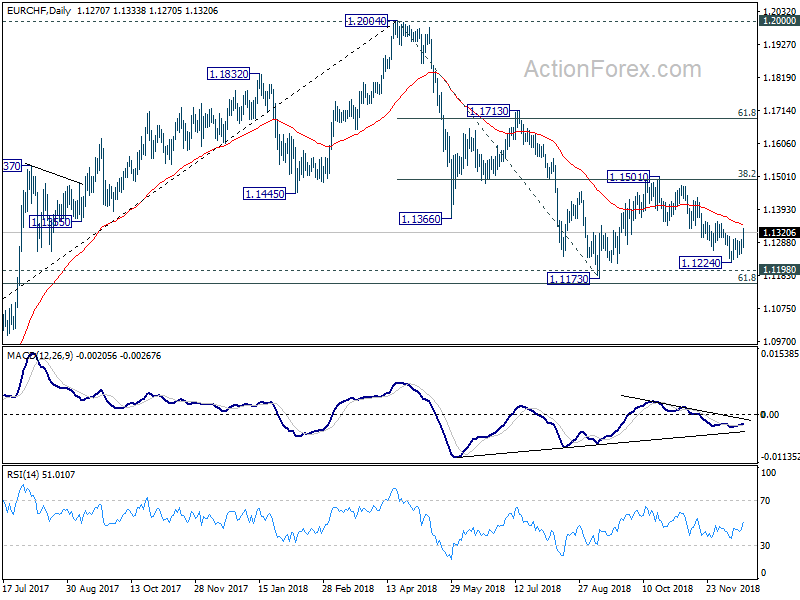

Technically, EUR/CHF’s strong rise today re-affirmed the case of near term bullish reversal. Focus will be on 1.1356 resistance next and break will pave the way back to 1.1501 resistance. EUR/AUD also strengthens notably and is eyeing 1.5887 resistance. Break will resume rebound from 1.5346 to 1.6 handle next. Otherwise, EUR/USD, GBP/USD USD/CHF and USD/JPY are staying in familiar range.

In other markets, FTSE is up 0.98% at the time of writing, DAX is up 0.57%% and CAC is up 0.61%. German 10 year yield is down -0.008 at 0.238. Italian 10 year yield is down -0.166 at 2.781. German-Italian spread is below 260. Earlier in Asia, Nikkei dropped -0.6%, Hong Kong HSI rose 0.20%, China Shanghai SSE dropped -1.05%, Singapore Strait Times rose 0.43%, mixed.

Released in early US session, Canadian CPI slowed to 1.7% yoy in November, down from 2.4% yoy and missed expectation of 1.8% yoy. CPI core common was unchanged at 1.9% yoy. CPI core median dropped from 2.0% to 1.9%. CPI core trimmed slowed from 2.1% yoy to 1.9% yoy.

Dollar mixed as FOMC rate decisions awaited

US Dollar is mixed as markets await FOMC rate decision. In short, Fed is widely expected to raise federal funds rate by 25bps to 2.25-2.50% today. The question is on the rate path in 2019 after all the political pressures Fed policymakers faced. The new economic projections will provide the key guidance to market expectations. More on the projections here.

Also, here are some suggested readings on FOMC:

- Fed Likely Hikes Rate in December, Future Path More Dovish

- S&P 500: Dovish Fed Hike Enough to Support US Stocks?

- Four Fed Scenarios And One Market

- Trade The Fed Decision

- USD/JPY: Will The Fed Deliver A Present Or A Lump Of Coal For Buck Bulls?

- Will the Fed be Less Dovish than Markets Expect?

- FOMC Preview: What Do We Expect?

- What To Expect From The Last Fed Meeting In 2018?

EU Dombrovskis confirmed budget agreement with Italy to avoid EDP

European Commission Vice-President Valdis Dombrovskis confirmed that an agreement is made with Italy regarding 2019 budget. He tweeted that “A lot of hard work and negotiation went into finding solution on the Italian budget. Let’s face it: the solution on the table is not ideal. But it allows us to avoid an Excessive Deficit Procedure at this stage, provided that the agreed measures are fully implemented.”

He added that “I hope this solution would also be the basis for balanced budgetary & economic policies in Italy. Italy urgently needs to restore confidence in its economy to ease financial conditions and support investment. Ultimately, this is what will support purchasing power of all Italians.”

UK CPI dropped to 2.3%, core down to 1.8%

UK CPI slowed to 2.3% yoy in November, down from 2.4% and matched expectations. But core CPI also slowed to 1.8% yoy, down from 1.9% yoy and missed expectation of 1.9% yoy. RPI also slowed to 3.2% yoy, down from 3.3% yoy and missed expectation of 3.3% yoy.

PPI input slowed to 5.6% yoy, down from 10.3% yoy, below expectation of 9.6% yoy. PPI output slowed to 3.1%yoy, down from 3.3% yoy, matched expectations. PPI output core slowed to 2.4% yoy, down from 2.5% yoy, above expectation of 2.3% yoy.

House price index slowed to 2.7% yoy in October, missed expectation of 3.3% yoy.

Low level US and China officials clashed at WTO

Reuters reported that two rather low level US and China officials clashed at the WTO today in closed-door talks. US Ambassador to WTO Dennis Shea accused China of doing “outright steal” technology of the US and said “this is not acceptable”.

China’s envoy said US administration’s “reckless actions” were the root cause of the crisis in global multilateral trade system. And he hoped that both countries can “move in the same direction with mutual respect to contribute to the stability of world economic and trade environment”.

Asian business sentiment stays low on trade war concerns

The Thomson Reuters/INSEAD Asian Business Sentiment Index rose to 63 in Q4, up from 58 in Q3 which was a near three year low. While readings above 50 still indicates a positive outlook, the result is still one of the lowest readings in years.

Antonio Fatas from INSEAD noted in the release that “this confirms the reading of the previous quarter: there is more uncertainty, there are increasing concerns about growth,” And, “this doesn’t mean there is going to be a crisis over the next quarters, but if there is one, this is an indication that it wouldn’t be a large surprise to some.”

Global trade war is, by some distance, the biggest perceived risks to business outlook. China slowdown and higher interest rates followed and then Brexit. The report also noted that, “the dispute between the world’s two biggest economies, threatens businesses throughout the region due to global value chains.”

Released in Asian session, Japan trade deficit widened to JPY -0.49% in November. Australia Westpac leading index dropped -0.1% mom in November.

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.1260; (P) 1.1279; (R1) 1.1301; More…

EUR/CHF rises to as high as 1.1333 so far today as rebound from 1.1224 accelerates. Intraday bias remains on the upside for 1.1356 resistance first. Decisive break there should confirm near term reversal. In that case, further rally should be seen back to 1.1501 resistance. On the downside, below 1.1288 will turn bias neutral first. But retreat should be combined well above 1.1224 low to bring another rally.

In the bigger picture, price actions from 1.2004 medium term top is seen as a correction only. Downside should be contained by support zone of 1.1198 (2016 high) and 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to complete it and bring rebound. A break of 1.2 key resistance is still expected in the medium term long term. However, sustained break of the mentioned support zone will mark reversal of the long term trend. In that case, 1.0629 key support will be back into focus.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Nov | -0.10% | 0.10% | ||

| 23:50 | JPY | Trade Balance (JPY) Nov | -0.49T | -0.31T | -0.30T | -0.29T |

| 07:00 | EUR | German PPI M/M Nov | 0.10% | -0.10% | 0.30% | |

| 07:00 | EUR | German PPI Y/Y Nov | 3.30% | 3.20% | 3.30% | |

| 09:30 | GBP | CPI M/M Nov | 0.20% | 0.20% | 0.10% | |

| 09:30 | GBP | CPI Y/Y Nov | 2.30% | 2.30% | 2.40% | |

| 09:30 | GBP | Core CPI Y/Y Nov | 1.80% | 1.90% | 1.90% | |

| 09:30 | GBP | RPI M/M Nov | 0.00% | 0.10% | 0.10% | |

| 09:30 | GBP | RPI Y/Y Nov | 3.20% | 3.30% | 3.30% | |

| 09:30 | GBP | PPI Input M/M Nov | -2.30% | 0.60% | 0.80% | |

| 09:30 | GBP | PPI Input Y/Y Nov | 5.60% | 9.60% | 10.00% | 10.30% |

| 09:30 | GBP | PPI Output M/M Nov | 0.20% | -0.10% | 0.30% | |

| 09:30 | GBP | PPI Output Y/Y Nov | 3.10% | 3.10% | 3.30% | |

| 09:30 | GBP | PPI Output Core M/M Nov | 0.10% | 0.20% | 0.30% | 0.40% |

| 09:30 | GBP | PPI Output Core Y/Y Nov | 2.40% | 2.30% | 2.40% | 2.50% |

| 09:30 | GBP | House Price Index Y/Y Oct | 2.70% | 3.30% | 3.50% | |

| 13:30 | USD | Current Account Balance (CAD) Q3 | -125B | -125B | -101B | |

| 13:30 | CAD | CPI M/M Nov | -0.40% | -0.40% | 0.30% | |

| 13:30 | CAD | CPI Y/Y Nov | 1.70% | 1.80% | 2.40% | |

| 13:30 | CAD | CPI Core – Common Y/Y Nov | 1.90% | 1.90% | 1.90% | |

| 13:30 | CAD | CPI Core – Median Y/Y Nov | 1.90% | 2.00% | 2.00% | |

| 13:30 | CAD | CPI Core – Trim Y/Y Nov | 1.90% | 2.10% | 2.10% | |

| 15:00 | USD | Existing Home Sales Nov | 5.20M | 5.22M | ||

| 15:30 | USD | Crude Oil Inventories | -1.2M | |||

| 19:00 | USD | FOMC Rate Decision (Lower Bound) | 2.25% | 2.25% | ||

| 19:00 | USD | FOMC Rate Decision (Upper Bound) | 2.50% | 2.50% | ||

| 19:30 | USD | FOMC Press Conference |