{kind=link}

Here are the latest developments in global markets:

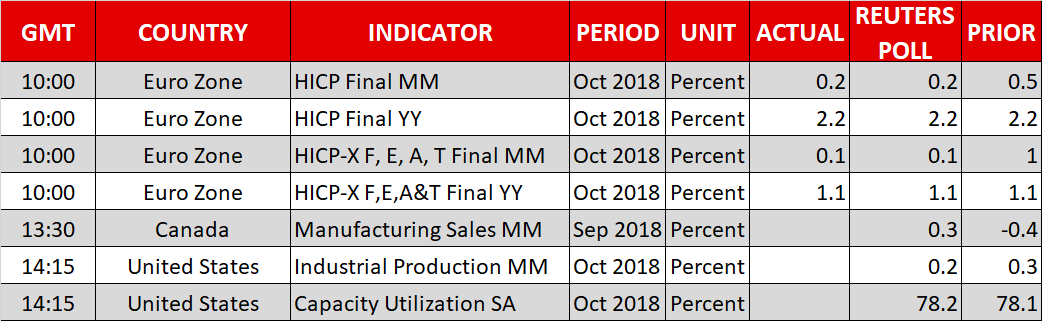

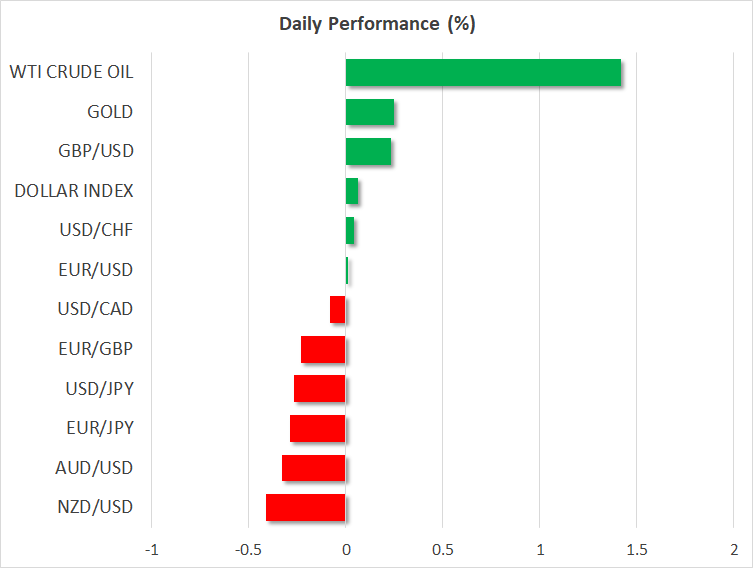

- FOREX: The dollar was slightly up versus a basket of currencies, with the closely watched British currency being broadly higher. Still, the pound mostly consolidated Thursday’s sharp losses on the back of the Brexit drama that unfolded, and still appears to have room to run. One exception was the yen, which came on the receiving end of safe-haven flows and thus the pound was unable to advance against it – pound/yen was flat –, while dollar/yen was down by 0.3%. Elsewhere, euro/dollar was unchanged on the day, giving back earlier gains that saw it rise to a one-week high of 1.1368. Somewhat dovish comments by ECB chief Draghi were seen as the catalyst behind the retracing of advances. Meanwhile, final eurozone inflation figures for October were in line with their preliminary estimates.

- STOCKS: Sentiment turned sour as UK media reports suggested that lawmakers are pushing forward with efforts to trigger a no-confidence vote in PM Theresa May, leading major European benchmarks to either completely wipe out previous gains or give up on a significant portion of advances from earlier in the day. The pan-European Stoxx 600 was little changed and the blue-chip Euro Stoxx 50 was down by 0.1% at 1211 GMT. Meanwhile, the UK’s FTSE 100 was down by 0.3%, the German DAX up by 0.1%, and the French CAC 40 lower by 0.1%. Futures on the Dow, S&P 500 and Nasdaq 100 were projecting a lower open on Wall Street, with contracts on the latter being deeper in losses, specifically trading lower by 1.2%.

- COMMODITIES: WTI traded higher by a sizeable 1.5%, at $57.30 per barrel. It was being helped by rising speculation that supply cuts will be agreed at OPEC’s meeting in early December. Still, the gains look insignificant relative to the selloff that took place from early October onwards, which even threw the precious liquid in negative territory for the year. Brent crude was also notably up, trading higher by 1.55%, at $67.65/barrel. In precious metals, gold was higher by 0.25% and not far below the one-week high of $1,218.33 an ounce hit earlier on Friday. Should May’s government collapse, then gold could come on the receiving end of safe-haven flows. The likely stronger dollar from such an outcome though, would probably place a lid on any resulting gains for the yellow metal.

Day ahead: Brexit and updates on Sino-US trade overshadow economic releases

The remainder of the day is light in terms of data, with developments on other fronts such as Brexit either way stealing the thunder from any releases.

Sterling is expected to remain volatile to Brexit news, as the situation appears fluid at the moment, to say the least. The prospect of further cabinet departures is well on the table, as well as that of a leadership challenge that could topple PM May from her position.

Meanwhile, attention is also falling on Sino-US trade relations. China is proceeding with concessions to the US that may on the one hand fall short of the Trump administration’s demands, but on the other they could pave the way for a meaningful de-escalation of tensions. Such an outcome will likely bolster risk-on currencies such as the Aussie, as well as equities.

Elsewhere, any news on the EU-Italy budget standoff have the potential to move the euro. Signals that Italian PM Conte is looking to work with the EU over his government’s 2019 budget are definitely euro-positive, given they deviate from the previous confrontational rhetoric. It remains to be seen though whether the positive momentum will be maintained, or whether the differences between the two sides would sooner or later lead to a clash.

On the data front, Canadian manufacturing sales for September are due at 1330 GMT, with US industrial and manufacturing output data following at 1415 GMT. Monthly growth in industrial production is projected to ease to 0.2% from September’s pace of 0.3%, though this would still mark the print’s fifth straight month of increases. Figures on October’s US capacity utilization are also due at 1415 GMT.

Bundesbank President and ECB policymaker Weidmann will be speaking at Frankfurt’s banking conference at 1300 GMT, while non-voting FOMC member in 2018 Evans will be participating in a Q&A session at 1430 GMT.

In energy markets, Baker Hughes data on active oil rigs in the US are slated for release at 1800 GMT.